Bringing Trust Back to Barclays: When a Strong Social Purpose Pays Off

Not all brands create purpose-led products. Winning in the purpose era sometimes means using branded signature social programs.

There is a general acceptance that an organization’s effective social effort should also boost business, but many suggest that the route to winning in the purpose era is by directly helping society through efforts like manufacturing wind turbines, distributing healthy food or saving costs from reduced energy use. The problem is that few companies make wind turbines or offer organic food, and energy use goals over time become less and less dramatic in part because incremental progress gets harder.

An alternative is to use branded signature social programs, whether internal or through a partnership with an external nonprofit, to advance the brand driving the business by providing energy and visibility, an image lift, and engagement opportunities for employees and other stakeholders.

A reasonable question that comes to mind—can a signature program truly help a business that may not be closely related to the program? There is research in psychology and elsewhere that supports the belief that elements of an admired social program can affect the perception and liking for the sponsoring brand. However, more definitive and rare evidence comes from brands that have demonstrated the impact of a signature social program on a brand in the field. An example is Barclays, that conducted what is termed a “before-after: experiment,” where relevant measures such as perceived trust are taken before the “treatment,” in this case the communication of stories around new social programs and compared to those same measures after.

Barclays is a role model for how to use branded signature social programs to regain trust, a key brand dimension in the financial services industry. The Barclays brand was damaged by the 2008 financial crisis with accusations that Barclays had manipulated key interest rates. In 2012, the trust level for Barclays in the United Kingdom was well below that of its competitors despite several years of PR and advertising arguing that the “new” Barclays should be trusted. It is not a stretch to conclude that Barclays was one of the least trusted brands in a heavily mistrusted sector in the U.K., Needing a restart, Barclays created a new brand purpose: “Helping people achieve their ambitions—in the right way.”

The 140,000-employee base was encouraged to create programs responsive to the new purpose. Dozens of programs emerged. The Digital Eagles was created by a 17-person employee group (a decade later the team had grown to 17,000 employees) with a mission to teach the public, especially the older cohort, about surviving and even thriving in the digital world. Stories about how the Digital Eagles and other programs affected real people helped shine a light on the social purpose initiatives at Barclays.

One story featured Steve Rich, a sports development officer, who had lost his ability to play football (soccer to Americans) because of a car accident. However, he could participate in “walking football”—usually played with a six-person team on a small field with no running—and again experience the joy of the sport. Wanting to help others do the same, he decided to raise awareness of walking football and turn it into a nationwide game in Britain. With the help of the Digital Eagles, Rich created a website that linked over 400 teams across the country and connected individuals with teams. It was partly responsible for the growing interest the sport has generated, the emergence of a national tournament, and the ability of people to connect with former football mates. His accomplishments and personal regeneration are inspiring indeed.

Employees were inspired and energized by the programs driven by Barclay’s new higher purpose. And customers and prospective customers changed their perceptions of the brand (as reported by the Edelman Financial Trust Barometer for 2014 summarized in the WARC Study noted above). Two years after the emergence of the signature stories, such as those involving the Digital Eagles, trust in Barclays was up 33%, consideration was up 130%, the emotional connection was up 35% (versus 5% for the category average) and “reassurance that your finances are secure” was up 46%. The new campaign drove six times as much change in trust and five times as much change in consideration as the descriptive “this is the new Barclays” campaign that preceded it. In addition, Barclays received 5,000 positive mentions in the press.

Barclays vividly demonstrates that a signature social program such as the Digital Eagles can lift a brand and is uniquely capable of doing so. There is little doubt that a sharp increase in trust and consideration means an increase in loyalty and even the size of the customer base. Barclays explicitly observes in the 2021 Barclays PLC Strategic Report that offering a complete menu of services to customers is dependent on the earned trust attached to the Barclays brand. The further implication is the Digital Eagles will be supported over decades because its impact on the Barclays brand makes the program a business asset.

In the purpose era, trust is an even more valued attribute and, when lost, it is hard to earn back. Barclays demonstrates that communicating different intentions and programs does not move the trust needle. But the right social purpose and program such as the Digital Eagles told with emotional stories can climb the hill.

Future Back Planning: Maximizing Future Growth Opportunities

Future back planning is key to unlocking uncommon growth during times of economic uncertainty.

Future back planning is key to unlocking uncommon growth during times of economic uncertainty.

In our latest global research report, Building Business Resilience Through Innovation, we found that a leading barrier to increasing innovation efforts is that the organization lacks a long-term planning process. Unfortunately for many companies, this has only worsened in the last few years as reactive thinking characterized by the pandemic era.

As innovation leaders emerge from this reactive phase and begin to chart out the next few years of growth during a time of great economic uncertainty, it is essential to create a growth strategy that spans these three-time horizons.

Across these horizons, there is an inverse relationship between the investment in resources and the investment in strategic decisions. Running the business of today is resource intensive and requires operating with excellence with much less space for strategic exploration. In contrast, exploring the business’ target destination over the next five to ten years within a wide open divergence environment is time intensive. Due to the scarcity of resources, it often requires time-bound investment to collect data on the most relevant drivers of change, model potential scenarios that could unfold over time, and based on that, determine what new opportunities are worth further validation and investment.

In Horizon 1, the existing value chain is used to optimize and scale the business, but in Horizon 3, the needed value chain will most likely be adjacent to today’s value chain. The inversion point of building the new value chain is challenging to manage because resources are ramping up as the ability to make strategic decisions is fading. At this point, the skills required to be successful change. It is operationally complex to get something to move through the inversion curve.

If a business neglects Horizon 3 activities today, it sets itself up to be leapfrogged by the competition because it will not have invested in the assets and capabilities needed to act on emerging opportunities.

Future Back Helps Companies Maximize Growth Opportunities in Horizon 3

While it is impossible to predict the future, market leaders and makers proactively anticipate preferred and disruptive future scenarios. The first step is understanding the most impactful drivers of change that will shape the future market landscape. Drivers of change come from a range of sources: the classic Porter’s Five Forces of suppliers, buyers, new entrants, substitutes and competitors that determine industry profitability, as well as macro-forces that are broader than industry boundaries, often categorized as social, technological, economic, environmental, and regulatory drivers (STEER).

From doing future back work across industries, we have found three non-mutually exclusive factors that help us see around corners. Across these factors, emerging technology is critical in reshaping societal norms, enabling new interaction modes, and determining future profitability and competitive advantage sources.

3 Non-MECE Factors that Shape the Future Market Landscape

1. The Overton Window describes the range of policies that are accepted by the mainstream at a given time and can be used to identify ideas on the threshold of gaining mainstream acceptance. For example, over the last 50 years, public acceptance of in-vitro fertilization (IVF) has rapidly increased as the availability of IVF technology has also grown. In 2021, fertility support startups raised $345M, up 35% from the previous year. Health systems and payors that anticipated this shift ten years ago were able to differentiate themselves within a rapidly growing market. However, with the overturning of Roe v. Wade, societal progress regarding IVF is now under threat. Industries heavily funded by the government, such as healthcare and clean energy, are also strongly shaped by changing societal norms.

2. Behavioral shifts often emerge due to technological advancements that make it easier to do more with less or create new modes of interaction between humans and machines. For example, Figma’s significant innovation was being browser-first, with the ability to edit files in real-time in the cloud, allowing teams of developers, designers, and product managers to collaborate in one place efficiently.

Adobe was late to the game of browser-first collaboration and, as a result, paid $20 billion to acquire Figma, which had roughly $400M in revenues at the time. The steep price was considered a solid investment given the future value of Figma’s product spaces. Thinking more broadly, technological advancements across the Internet of Things, artificial intelligence, artificial and virtual reality, and autonomous machines will enormously impact behavior and interaction modes, changing how we learn, work, collaborate and entertain ourselves.

3. Business model shifts are often required to capitalize on or meet emerging technology demands, regulation, the economic environment, and ESG agendas. For example, Fundrise was the first company to crowdfund real estate investment successfully, and the founders did it by seeking the expertise of regulators from the beginning. Working with a former regulator, Ben Miller figured out how to use Regulation A to raise money from non-accredited investors, which was the first time anyone had ever done. Eventually, the regulation changed to Regulation A+, which allowed the company to raise more equity from non-accredited investors while streamlining the filing process. Still, at that point, Fundrise was already the category leader in a new market.

Four Questions to Determine a Company’s Options within the Future Market Landscape

Once we understand the most impactful drivers of change, the next step is modeling the most viable opportunities for a specific company to pursue. We begin with four questions:

1. How is a company encumbered and advantaged?

This includes understanding a company’s options based on its funding and regulatory moats. Firms funded by unregulated capital have an entirely different set of options than firms funded by regulated capital. A venture capital-funded firm can take on much higher fixed costs to stand up a new capability without a near-term path to profitability. For example, the data cloud company Snowflake raised $2.1B over eleven rounds of funding since 2012 and isn’t expected to reach profitability until 2023.

On the other hand, an advantage of being a large, publicly traded company is that it is easier to find suppliers and partners to test and validate Horizon 3 growth hypotheses with and bring new offerings to market. Along with understanding the implications of funding sources, it’s essential to know where margins come from today – is it from hardware, software, or services? Who has the most power in the value chain to extract more margin over time? What parts of a company’s existing product line, assets, and capabilities might serve as a moat? Does it have access to a rare resource on the supply side or a lock-in effect on the consumer side? Finally, is there a regulatory moat that will make it difficult to unseat an incumbent?

2. Who has the preferred position in the market to launch and scale this idea?

The most critical mindset of future back work is humility. We always assume that another player is better set up to execute an idea. The big four (Alphabet/Google, Amazon, Apple, Meta/ Facebook) dominate their innovation ecosystems due to their scale, network effects, and ability to buy entire markets. Firms operating within these ecosystems are often unlikely to win share-of-wallet among end consumers and are much more likely to succeed by playing a critical infrastructure or support role. We look at the role of aggregators and integrators in the innovation ecosystem to understand how parts of the market are consolidating and where technology is being abstracted away from the end user.

3. Who is the player that can shut this idea down?

As Archimedes said, “The shortest distance between two points is a straight line.” In highly regulated industries such as financial services and healthcare, a significant source of Horizon 3 growth is creating new business models based on the changing regulatory landscape. Like the Fundrise example, the founder of Coinbase realized that abiding by U.S. law rather than moving offshore could act as a long-term defendable moat for the company. With the collapse of FTX, that bet has already paid off.

4. What has prevented this idea from being launched and adopted before?

Is the idea on the threshold of becoming mainstream? Is there a consumer experience problem or a price-to-value problem? Or does capital not think it’s worth an investment? The inevitable endpoint of markets is to solve consumer problems rather than business and technical problems. Enterprise capital is good at solving Horizon 1 business problems, such as increasing conversion in existing channels, creating efficiencies, and increasing margins.

On the other hand, venture capital is good at investing in long-plays that create new consumer markets because it has a risk appetite and is willing to be too early. Too early might mean taking on the cost of educating the market about a problem that they should have realized could be solved. For example, Netflix was loved for eliminating late fees (a consumer problem previously considered unavoidable in a physical rental market). Still, the company was perceived as shifting to a digital-first business model too quickly. Success in bridging the gap between its Horizon 3 digital-first business and its Horizon 1 DVD rental business required subsidizing the price of the new service for end consumers.

The Mindset We Bring to Future Back Work

The future back process combines design methodology (outside-in and hypothesis-led) with business rigor (commercial opportunity assessment with an asset-forward view of value-chain adjacencies and potential competitive moats).

The mindset we apply to this work draws from design and consulting. We’ve distilled it into three design principles:

Humble

We begin this work by assuming that another player has a better solution as well as a preferred position in the market.

Anti-fragile

We create a durable portfolio of growth moves in order to hedge our bets, with the understanding that it is impossible to know exactly how the market will reshape over time.

Effective collaboration

You need to keep running the business of today while exploring what your business might be in the future. At the same time, your hypotheses around how the market might shift and what options are most attractive for your company are the entry point into this work. We design future back engagements to extract maximum input in the most time-efficient way by starting with stakeholder hypotheses, bringing in external experts to identify new opportunities and threats quickly, and then designing workshops and executive communications that bring your team along the right way at the right time.

The Outcomes We Achieve Through Future Back Work

There are three main outcomes that we have consistently achieved through this work:

Board-level alignment and buy-in on a future vision. For example, supporting the approval of a board-level, multi-hundred-million-dollar M&A strategy in order to create an entirely new product category.

Driving capital allocation for new business building. For example, on a recent project, this work led to a $5 billion acquisition as the centerpiece of a new business unit.

Updating the product roadmap to transition from now and near-term investments to decisions that will drive the next horizon of the business.

We would love to do this work with you. If you already have hypotheses on the future of your business, we can dive into a Future Back project to explore, validate, design and quantify those opportunities. If you know that your company needs a Horizon 3 growth strategy, but your leadership team isn’t bought in, we have interim steps to drive alignment among stakeholders while collecting initial hypotheses on potential sources of long-term growth.

Interested in maximizing your future growth opportunities? Please get in touch.

The next M&A banking wave may be upon us. What can be learned from past integrations where brand was left in a suboptimal place?

While there is no crystal ball, slow economic growth and an inverted yield curve continue as headwinds for the banking industry. Both have already exposed vulnerabilities of large regional banks like Silicon Valley and Signature Bank, as well as G-SIBs such as UBS and Credit Suisse. While the speculated wave of consolidation may be overblown, there will no doubt be M&A activity during the foreseeable, uncertain future.

HBR continues to cite that between 70-90% of acquisitions fail. In addition, MIT Sloan studied 200+ M&As with values exceeding $250M during a 10+ year period starting in 1995 and learned that in nearly two-thirds of those deals, brand strategy was deemed to have a low to moderate influence in pre-merger discussions. This approach leads to the new identity or identities post-merger in a suboptimal place with limited clarity and often stems from a gap in brand expertise during the M&A process and following.

Specifically, we see five common mistakes related to brand that hinders speculated growth performance and increase costs during and post-acquisition:

The deal strategy undervalues customer upside and risks: To complete a fully informed financial forecast, due diligence must quantify current and future demand, change tolerance and emerging customer requirements.

There is limited understanding of purchased brand assets: For a truly shared optimized portfolio post M&A, companies must understand how all brand assets work to drive choice, revenue, and pricing power.

Integration teams have a narrow framing as primarily a “re-branding” effort: M&A presents a rare, point-in-time opportunity to articulate a new corporate narrative, upgrade customer perceptions and drive lasting cultural change within the organization.

Integration planning without a go-to-market plan to win: Integration priorities should pair synergy plans with growth moves: product, service and experience innovation to drive growth through the new asset base.

The new enterprise under-leverages culture and employee engagement: Successfully informing, engaging and enabling employees BEFORE launching externally is critical to retaining human capital and driving cultural engagement.

As inevitable market forces drive sustained or increased M&A in the banking industry, new and exciting opportunities emerge. Here are three practical things to consider that relate to your brand (and business) during M&A:

Consider customer context early and often: Ensure all functional discussions include conversations around customer impact and set a precedent that addressing the customer impact and experience is a priority. This is especially true at retail banks, often built around specialized customer focuses or geographic footprints with entrenched identities.

Evaluate the value and values of brand assets to guide the right transition plan: Typically, fewer stronger brands win out in banking. While long-term efficiencies exist for consolidating brands, careful work must be done to explore different end-states and migration scenarios. Perform the right evaluation ahead not just to understand the brand’s value, but also the inherent values the brand holds, and the customer perception to guide the right transition plan in context.

Discover or rediscover purpose and power it through culture from within: Banking consolidation done wrong can feel like a mismatched transformer coming together with messy operating model discussions and integration cadences that unfold over time. This can be especially distancing for distributed employees working in branches or regional offices closest to the customer. Investing early in the process to better understand and sharpen a combined new culture with a more meaningful purpose can serve as a North Star for smoother and more engaged integration.

Despite certain leading indicators, it will be hard to predict exactly what will happen with M&A in the banking sector. However, we can learn from the past in some capacity through the diligence and integration process to better predict the future, learning about the importance of brand as a critical consideration in the process.

For more information on capturing greater brand and marketing value through M&A, please contact us today.

Connecting the Dots Between Innovation and Resilience: 4 Learnings for Companies in China

Companies in China believe innovation and resilience are connected but they experience strong tension. Read more on how to overcome barriers.

Investing in both innovation and organizational resilience are two essential elements of success for companies to compete in today’s rapidly changing world. Through interviews with 14 senior executives and surveying 300+ innovation experts across the globe, Prophet’s latest research explores how successful organizations use innovation to drive business resilience.

Four Learnings for Companies in China to Build Innovative Organizations

Our findings reveal that innovative companies are more likely to be resilient. Particularly, 60% of respondents in China agree that innovation and resilience are connected, more so than their counterparts in Singapore (48%), the U.S. (47%) and the UK (47%). However, there exists a strong tension between the two characteristics – while Chinese companies on average deploy more innovation tactics compared to companies globally, they also face more pronounced barriers. In this article, we share our key findings and explore implications for Chinese businesses seeking to drive sustainable growth through innovation.

1. Prioritize Cross-Functional Alignment

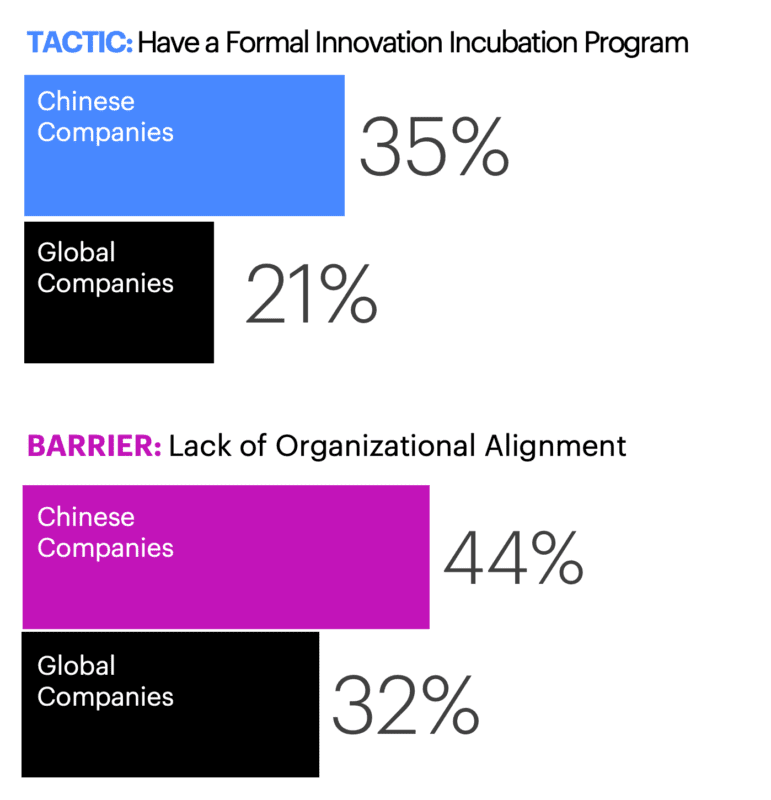

Incubation programs and pod-like team structures have long proven to be effective innovation tactics and are widely adopted by companies in China. According to our research, 35% of Chinese respondents report that their companies have a formal innovation incubation program compared to 21% of respondents globally. Additionally, 27% of Chinese respondents report their companies use pod-like team structures vs. just 18% of respondents globally. However, such team structures risk becoming siloed. A lack of cross-functional alignment remains a significant barrier to innovation and growth, with 44% of Chinese respondents citing it as a challenge compared to only 32% globally.

One example of how cross-functional alignment can impact innovation comes from the fast-growing beverage brand Chi Forest. As a startup, the company found tremendous success through operational agility, running pod-like teams with product managers in each team leading individual innovation initiatives. However, as Chi Forest grew, organizational inefficiencies emerged due to a lack of streamlined workflows and cross-functional collaboration, causing an overlap of roles and processes. Chi Forest has embarked on an organization-wide transformation agenda to reimagine its operation and business model.

Takeaway: It is important to implement innovation incubation programs and pod-like team structures, while also emphasizing cross-functional alignment.

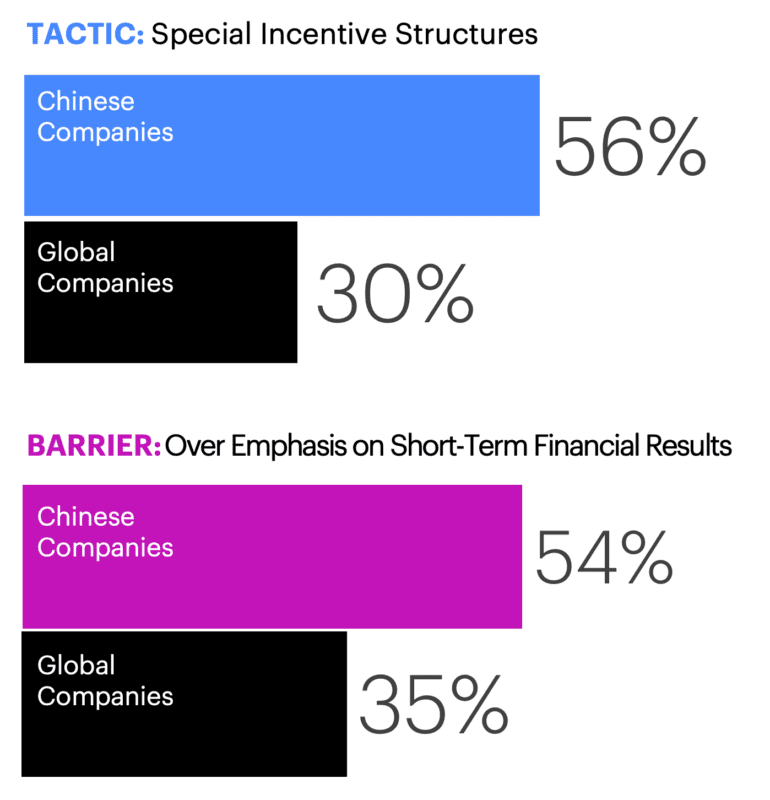

Incentives are a crucial part of driving innovation, but overly focusing on short-term financial outcomes can hinder success. Our findings show that 56% of Chinese respondents report their companies to have special incentive structures for new business opportunities compared to 30% globally. Yet this has also led to an innovation barrier, where 54% of Chinese respondents say their companies have too much emphasis on short-term financial results compared to 35% globally.

To empower long-term growth for the company, innovation success should be measured against various objectives beyond financial ROI. For example, Xiaomi has a series of incentive programs to encourage innovation, including an Annual Technology Award that rewards $1 million to an internal engineering project every year, evaluating technology and engineering excellence as well as business impact. The 2022 winner, Xiaomi’s CyberDog team, impressed CEO Lei Jun because the project successfully integrated many of the group’s R&D results and presented new technologies that could be soon applied to other core products. This is a good example of how incentives can be used effectively to drive impactful innovation.

On the other hand, companies like Pop Mart are facing growing pains. Although the company offers generous incentives, it measures innovation success solely on the creation of new product lines and their short-term sales volumes. As a result, the toy maker is left with a bloated portfolio and hasn’t been able to elevate its brand equity despite years of exponential growth.

Takeaway: To avoid pitfalls, organizations must develop incentive structures to recognize results, while avoiding overly focusing on short-term financial outcomes.

3. Guide Rapid Innovation Cycles with Long-Term Vision

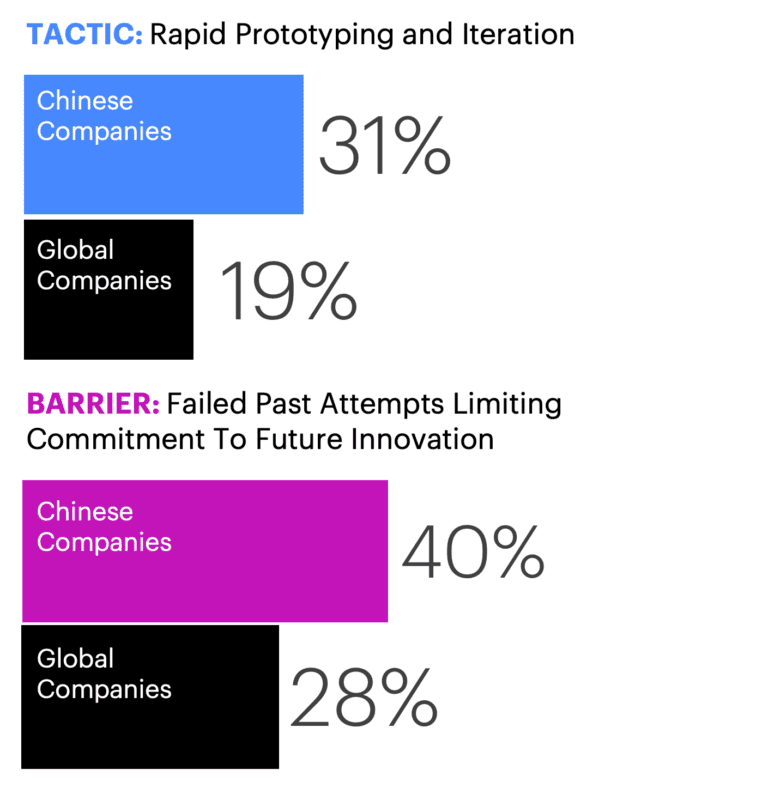

Rapid prototyping and iteration is a common innovation tactic, but past innovation failures and a lack of long-term planning processes can discourage innovation. Our findings show that 31% of respondents in China say their companies use rapid prototyping and iteration compared to just 19% of respondents globally. However, failed past attempts at innovation have limited commitment to future innovation for 40% of Chinese companies compared to 28% globally. Additionally, 40% of Chinese respondents say their companies lack a long-term planning process compared to 38% globally.

Shiseido’s approach to innovation is a great example of how companies can balance a strong brand vision and rapid innovation cycles. “Shiseido’s ability to have lasting success is in large part due to our dedication to creating the best quality products to meet consumer needs. This dedication to ‘craftsmanship’ is why we don’t blindly follow market trends but rather think critically about how we can further refine our products,” said Carol Zhou, SVP of China Business Innovations & Investments at Shiseido, in an interview with Prophet, “Although we may not always be at the forefront of trends, we have found the right pace to create a timeless brand.”

Takeaway: Organizations should lead innovations with a clear vision and long-term planning, while enabling rapid prototyping and iteration based on a clear strategic roadmap, to create products that meet both long-term and short-term goals.

4. Focus on Customer Insights as a Foundation of Innovation

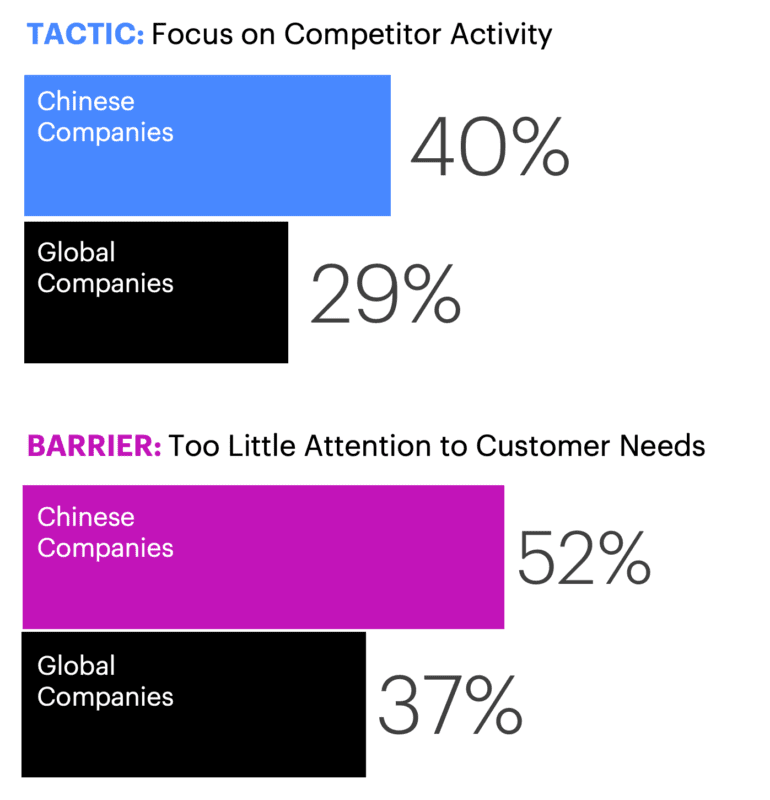

Creating differentiating innovations and finding emergent subcategories are effective ways to separate yourself from competitors, but paying too much attention to competitors and too little attention to customer needs is a surprisingly common mishap, according to our research. Chinese companies tend to focus heavily on competitor activity, with 40% doing so compared to 29% globally. This is often at the expense of paying attention to the needs of their customers, with 52% of Chinese respondents reporting that a major barrier to innovation for their companies is paying too little attention to customer needs, compared to 37% globally.

Companies must develop an organizational-wide mindset of diving into customer insights, data analysis, and user testing to identify what customers truly need and want. By doing so, they can create innovative products and services that truly differentiate them from their competitors, making them stand out in the market. Nike has been successful in this regard, with a strong focus on the athlete and understanding their needs driving their innovations. As Mark Parker, CEO of Nike, explains, “Our success has been based on our commitment to innovation and great design, which really in our case starts with our commitment to the athlete – and really understanding the athlete and the insights we get from that relationship. So, we translate those insights into real innovation.” In China, Nike actively deploys a localized digital ecosystem to engage with its customers and understand their needs. In turn, the rich data gathered from these digital platforms continuously fuels its innovation and growth.

Takeaway: Prioritize a human-centered approach that focuses on customer needs to create truly meaningful innovations.

Building Innovative Organizations

Indeed, innovation is not a department, but a collective achievement of an organization, as one innovation leader has told us. Companies should lead with a vision, encourage risk-taking, experimentation, and collaboration across all levels of the organization. This will help to create an environment where innovation can thrive and become ingrained in the company’s DNA.

What can your company do today to turbocharge innovation?

Emphasize the importance of always-on consumer insights and deploy the right team and structure as enablement.

Ensure a holistic view of the market demand landscape, covering both consumers and competition and strategize growth moves and innovation efforts.

Build a multi-year roadmap with different chapters and cross-functional teams and land the detailed action plan in a short-term/ one-year plan.

Clarify how innovation initiatives drive business purpose, develop employee value propositions and define incentives accordingly.

Transform how your innovation team works within your organization to instill agility and collaboration.

Innovation and organizational resilience go hand-in-hand. Combined with investing in diverse innovation tactics, driving C-suite buy-in, and creating an organizational-wide innovation culture, businesses are more likely to be innovative and resilient, and become more likely to have greater financial success.

Our research shows that Chinese companies excel in deploying innovation tactics compared to companies globally, however they also under-invest in building long-term resilience. It is crucial for them to close this gap in order to drive transformative growth that’s meaningful and sustainable.

Prophet’s verbal experts share their POV on four trends we anticipate for AI and its future role in content development.

AI takeovers have long been our dystopian fantasy. Except we imagined something more apocalyptic, with explosions, volcanic skies and scarce resources, and the whole thing would be directed by Michael Bay. To our imagination’s dismay, the integration of AI into daily life has been pretty drama-free, taking on tedious tasks like filling in payment details, scheduling, and drafting texts.

But when ChatGPT showed up, boasting its domination over the written word, writers had questions:

What will happen to our jobs? What about the sanctity of writing as a labor of love? Is writing really writing if it’s developed by AI?

While it’s fair to believe AI is overstepping, we also know this is just the beginning. With so much technology of the future already in motion, we can’t deny that a new era for writing, communicating, and knowledge sharing has arrived. Sure, it will take some getting used to, but we’re starting to come around to the possibilities AI presents for writers.

Kevin Kelly, founding executive editor of Wired magazine and author of The Inevitable: Understanding the 12 technological forces that will shape our future writes: “This is not a race against the machines. If we race against them, we lose. This is a race with machines. You’ll be paid in the future based on how well you work with robots … It is inevitable. Let the robots take our jobs and let them help us dream up new work that matters.”

Let’s not forget, we’ve been in this situation before: just like typewriters made way for laptops, and typing made way for audio recording, ML and AI will surely help professional writers become more prolific, discerning, and original over time. It might even help aspiring writers gain the confidence they need to get started.

We’re eager to see what these tools are capable of, and below are four trends we anticipate in the coming months and years:

From Content Creation to Content Curation

As AI continues to take on the bulk of content creation, more people will be inspired to distill, edit and provide commentary on existing content. Content creators will eventually be succeeded by content curators. Similarly, strategists, editors, and commentators will become the creative forces brands and media outlets seek as they strive to keep up with the demand for niche and personalized content.

Podcasting and video will also continue to reign since they provide authentic, undeniably human content built on connection and collaboration.

Still, employers will need people to operate and monitor AI writing tools, which will naturally position AI prompting, co-writing, and editing as core competencies for employees in communication fields. In the same way that SEO writing matured into a core competency, employers will expect their staff to upskill, and seek employees who can use AI writing tools effectively.

A Reinvigorated Emphasis on the Craft of Writing

It’s no secret that the line between writer, content creator, and a guy with a Twitter account has all but disappeared over the last 15 years. AI will exacerbate that issue by enabling people to publish under-developed work faster.

Fortunately, that will make fresh, high-quality content more valuable and easier to spot. We’ll see more recognition for human-derived work by way of badges next to author profiles—think the esteemed “verified” checkmark used on platforms like Spotify and Instagram. As these new hierarchies of quality become the norm, top-tier writers with the appropriate credentials will be celebrated simply by writing without the help of AI.

Though, as we continue to explore the power and potential of systems like ChatGPT, we should also remind ourselves of their limitations. For example, ChatGPT is branded as AI, but it’s actually a machine learning (ML) tool operating through algorithms that mimic human intelligence. While it’s mostly impressive, it’s not sentient—and it’s not going to replace human writers any time soon. However, writers should still be actively looking for ways to welcome its assistance in their work.

Marketers will Happily Delegate Information Gathering to Focus on Creativity and Strategy

With platforms claiming the ability to produce creative company names instantly, many marketers, brand builders and creatives understandably met the launch of ChatGPT with trepidation.

At first, it felt like a threat to the very nature of the creative process. If it were true that AI could produce original work in a fraction of the time, would naming specialists have any hope for a secure professional future? Fortunately, it only takes a few queries within ChatGPT for that fear to subside. The platform cannot yet replicate the art of persuasive copywriting or effective naming. Sure, it’s fast, but it’s not creative.

We, however, can take advantage of its superior productivity skills. As we well know, the brainstorming process begins with a clearing of the obvious or “bad” ideas. ChatGPT can help us surface and trash those ideas faster, freeing us to dig deeper, explore new avenues of inspiration and test unexpected executions. Essentially, we can build off what AI can deliver as a first step and springboard to something more distinctly human and original.

Apprehensive Publications will (Eventually) Come Around

Despite the current debate on whether to publish or recognize AI-assisted content in any capacity, eventually, we will award work partially written by AI.

Not convinced? Look at the self-publishing industry. Self-published books, articles, and essays were wholly regarded as less than for years. Self-published writers were pariahs because they didn’t jump through the same institutional hoops as the “real” writers before them. Once thousands of self-published writers found their audiences and made a living doing what they loved, criticism subsided. Public figures shared their work on sites like Medium. Global sensations like EL James (50 Shades of Grey) and Robert Kiyosaki (Rich Dad, Poor Dad) and even some of Margaret Atwood’s early works were self-published. Self-publishing became a welcome professional trajectory.

It’s of course ironic that with ChatGPT, self-publishing platforms are the ones playing gatekeepers. Medium, Amazon KDB, and Substack are among the publications that have shared formal statements regarding AI regulation, like this one from Data Science:

“We’re committed to publishing work by human authors only, and we don’t—and won’t—accept posts written in whole or in part by AI tools.”

Writers who respect the craft and want to see it upheld at their preferred publications will continue to push for better regulatory practices. Others will celebrate the new possibilities of AI-generated content, advocating for its necessity in today’s content-driven world. Medium is one such publication:

“We welcome the responsible use of AI-assistive technology on Medium. To promote transparency, and help set reader expectations, we require that any story created with AI assistance be clearly labeled as such.”

Over time, the passionate opposition to AI-assisted writing will fade, and we’ll find a place for it in the hierarchy of writing quality. Soon, AI-assisted writing will become as commonplace as publishing your debut novel on Amazon.

As AI writing tools like ChatGPT continue to mature, people will continue to explore its role in art, culture, content and communication. Though these tools currently present as many pitfalls as possibilities, in time we’ll find this technology will help us shift into a new era as writers, thinkers and collaborators.

Addressing the ESG Gap: Reconciling ESG Performance and Perceptions

Identify and address gaps in ESG performance and customer perceptions.

ESG is not just a feel-good initiative – it is a vital part of business and employee engagement strategies that drive growth in a world that increasingly needs businesses to address pressing global challenges.

Companies face pressure from multiple stakeholders to be more socially and environmentally responsible while being transparent about that progress. While there is a continued push by consumers and employees, regulators and investors are also pushing harder for ESG. The EU now requires companies to publish reports on the social and environmental risks they face (with the US not too far behind).

As a result, businesses have begun to invest more seriously in delivering against their ESG ambition and targets – aiming to create a tangible impact. But as the ESG focus strengthens, there is often a gap – between how companies perform on ESG, and what customers perceive of a company’s ESG strategy.

Evaluating the ESG Gap

The ESG performance vs. ESG perceptions gap is based on two questions: 1) How well is my company performing on ESG? and 2) How do customers perceive we’re doing on ESG?

The glaring discrepancy between these two questions has fueled the rise of “greenwashing” or “purpose washing” accusations against some companies, while the reconciliation of this gap has generated growth by leaning into customer preferences. As a result, it’s urgent that companies understand and evaluate their gap to maximize their ESG impact and tap into new opportunities.

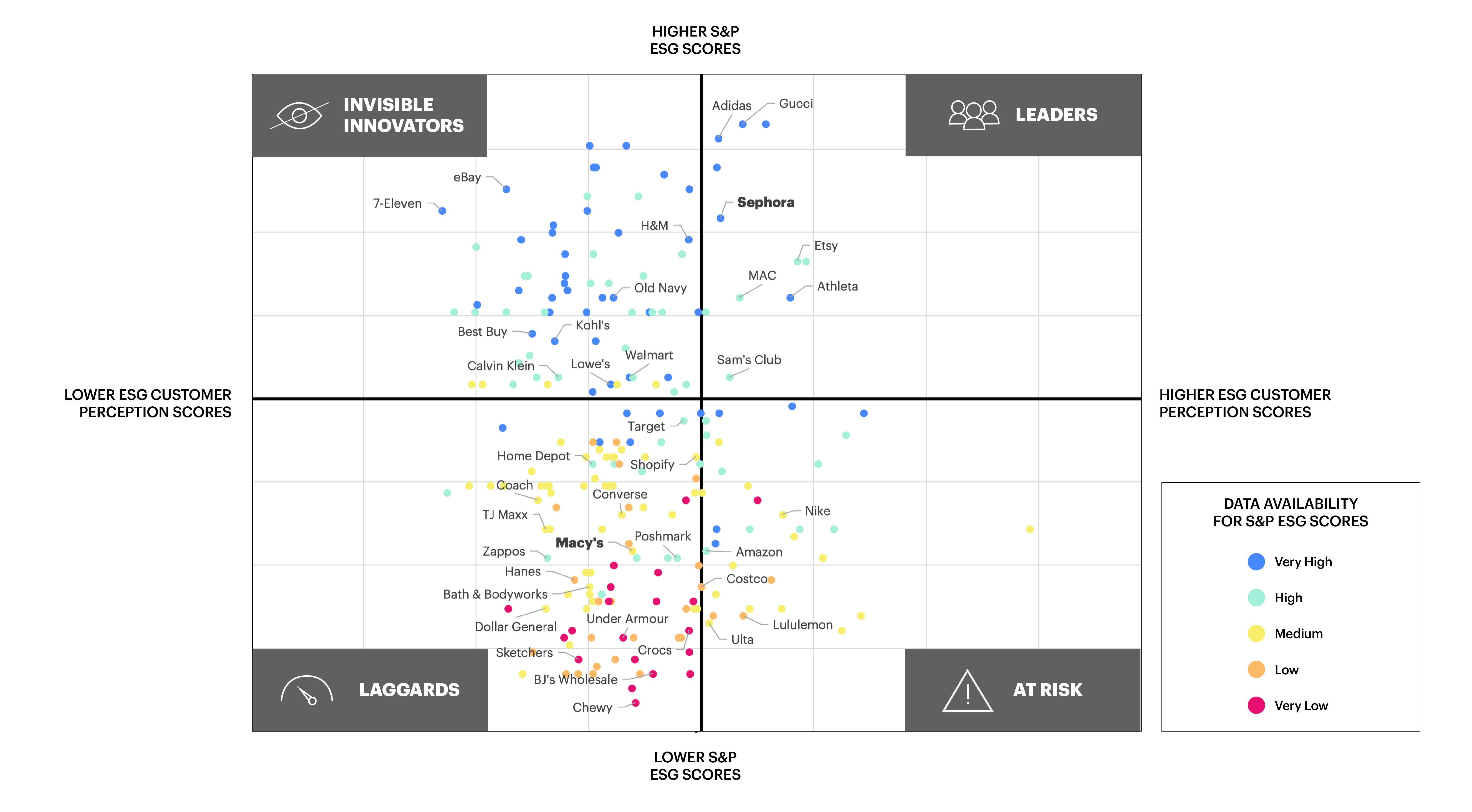

Note: Dots represent industries and companies included in the Prophet analysis.

Figure 1: ESG Performance vs. Perceptionsexample

ESG Performance

In addition to companies’ internal reporting, a wave of third-party ESG metrics and ratings (e.g., MSCI, S&P ESG Scores) have emerged. These scores measure how well a company addresses and manages risks in the areas of environmental, social, and governance. As a result, ESG scores should provide an unbiased, comparable view of a company’s ESG exposure to guide investors.

While these metrics aren’t perfect – they often leverage incomplete data and standard measurement processes have yet to be implemented – they provide much-needed visibility to external stakeholders and comparability across companies and industries.

ESG Perceptions

ESG performance scores measure what a company is doing across ESG initiatives – it’s another effort to be recognized and rewarded for that investment by consumers.

While many factors affect brand perception, companies are starting to integrate customers’ ESG perceptions into their analysis as ESG becomes a purchase influencer. For example, products making ESG-related claims averaged 28% cumulative growth over the past five-year period, versus 20% for products that made no such claims. Companies can look at data (like the Prophet Brand Relevance Index ®) to better understand what consumers think of their brands.

Using performance scores and customer perceptions of ESG, companies can start to understand if they are successfully communicating how their ESG agenda translates to additional value. Alternatively, these metrics can help companies determine if their words are ahead of their actions and if they are at risk of greenwashing or virtue signaling.

The Framework

By identifying the gap, companies can diagnose where they are in their ESG journey and the next steps for progress: Are they slow to adopt ESG and need to integrate it into all functions? Are they perceived by customers to be performing well on ESG but not living up to it? Do they have robust ESG programs but aren’t publicly recognized for them? Or are they ESG leaders?

To better illustrate the gap, we mapped customer perceptions and ESG performance scores, identifying four quadrants that companies may occupy. We will take a closer look at the automotive and retail industries, both of which have organizations that occupy all quadrants.

Overall, one theme emerges: Companies need to do better on ESG, both in establishing and executing ESG commitments and initiatives and sharing that progress openly with stakeholders.

Figure 2: ESG Performance vs Perceptions: Automotive Industry

Figure 3: ESG Performance vs Perceptions: Retail Industry

Leaders (HIGH Performance/HIGH Perceptions)

What this means: Companies here are both performing well on customer perceptions and ESG performance scores. Some of them have found strong alignment between elements of ESG and their businesses. Others have leveraged an element of their business (a product or a component) to build credibility with consumers around an area of ESG (e.g., using recycled or renewable materials in a new product). Overall, these companies are born out of purpose, intertwining their ESG strategies with business strategies.

Who we’re seeing in this space: This is an aspirational quadrant not characterized by any one industry. The few inhabitants often represent the best of their category, having typically established ESG precedents for their industries.

For retail (see figure 3), Adidas, Sephora, Etsy, and Athleta live here. Sephora is known for integrating DE&I thinking not only into its internal culture and employee operations but is also committed to ensuring that its products are sourced from diverse businesses. It was the first retailer to dedicate at least 15% of shelf space to Black-owned brands and commissioned the first-ever large-scale study on Racial Bias in Retail to improve the shopper experience.

What to do if you’re here: Continue to make sustainable and socially responsible products, services, and investments in ESG. By seeking industry collaboration, companies can bring others along on the journey and strengthen the category. But while it’s great to have established leadership, companies here will need to be vigilant and make their leadership positions defensible. Other companies will see the benefit of being known as strong ESG performers and will strive to replace the current leader.

At Risk (LOW Performance/HIGH Perceptions)

What this means: This quadrant is characterized by high customer perceptions of ESG in contrast to low performance on ESG. ESG may be well integrated into the brand story through messaging, but there hasn’t been strong progress in delivering on that narrative.

Someare purpose-native companies that made ESG a core part of their brands, benefitting from the halo effect from their origin story, despite being unable to enact a robust ESG strategy as they scale. Other companies include strong consumer brands with ESG-friendly elements, but company performance on ESG doesn’t match.

As a result, companies here are at risk of being labeled as “greenwashing” or “virtue signaling” if customers realize the company’s ESG initiatives amount to statements with little evidence to back them.

Who we’re seeing in this space: Some companies may be unable to scale their ESG performance to align with their words. For example, Tesla (see figure 2), nearly synonymous with EVs as the pioneer in the space, was born out of the purpose to accelerate the world’s transition to sustainable, clean energy. However, despite this clear mission, the company has struggled to make strides in other facets of ESG – Tesla was removed from the S&P 500 ESG Index because of issues of racial discrimination within its workplace. Its CEO is famously outspoken for his anti-ESG rhetoric.

What to do if you’re here: Assess where to improve or build strategies to deliver on ESG promises and customer expectations. Commit to bold moves against top risks to show progress and authenticity.

To avoid widening the gap, companies should evaluate the validity of any explicit ESG claims in their messaging to ensure that they are staying true to their statements. ESG performance should be prioritized over ESG perception building.

What this means: Companies here are performing well on ESG but aren’t recognized for their progress by consumers. This could stem from 1) not communicating ESG strategies to external stakeholders, 2) not coordinating ESG excellence with brand and marketing, or 3) believing that their customers might not prioritize ESG when they search for and purchase products. Some companies, like a QSR or CPG food company, might even be plagued by category stigma developed over years of a tarnished reputation.

We also see more consumer awareness of social and environmental efforts in lifestyle, fashion and entertainment categories – consumer-facing brands that play prevalent roles in culture and identity – rather than functional brands in the appliance and food categories. ESG expectations will also vary by the category of the issue. For example, some customers may think a transportation company should prioritize environmental issues over social issues.

In figure 1, we see a relationship between low ESG performance scores and low ESG data availability – illustrating that without robust data sets for third-party ratings, companies’ ESG scores will ultimately be hurt.

Who we’re seeing in this space: When we look at the rest of the automotive industry (see figure 2), there is an intriguing contrast with Tesla. There is a cluster of auto companies including Volkswagen, Mazda and BMW that have higher ESG performance scores but lower customer perceptions of ESG. This illustrates the necessity of not only delivering on ESG ambitions but communicating them well.

For example, BMW established clear goals such as reducing CO2 emissions by over 40% by 2030 and meeting climate neutrality no later than 2050. Additionally, the company aims to have 10 million fully electric vehicles on the roads by 2030, with all vehicles able to be fully recovered and reused for circularity. However, BMW’s lower customer perception of ESG illustrates that customers don’t know what BMW is doing to leave a positive impact on the environment, potentially leaving environmentally conscious consumers out of reach.

What to do if you’re here: Companies should build connectivity between their ESG and brand narratives for a cohesive story that touches all stakeholders. They should also start sharing their ESG data more openly to socialize their performance. If their brand is rooted in ESG, then they should follow up with the numbers to support it.

Companies should increase collaboration between the Chief Marketing Officer and the Chief Sustainability Officer. Shine a bright light on the elements of ESG that consumers care about. If companies don’t know if or what they care about, they need to find out.

Laggards (LOW Performance/LOW Perceptions)

What this means: Companies here are underperforming on ESG and are perceived poorly by customers with respect to ESG. This may mean that these companies still see ESG as a siloed function (like Corporate Social Responsibility) in the business. Companies here may also be in an industry where no player is focused on delivering against ESG. Or the company is lagging, relative to its more ESG-progressive peers.

As a result, there is ample opportunity to establish a strong foundation for growth in all areas of ESG.

Who we’re seeing in this space: Typically, larger, legacy companies – especially those whose businesses seem foundationally at odds with ESG – may run into these ESG challenges because they are slower to adapt. For example, the apparel and fashion industry (see figure 3) – which is responsible for 10% of human-caused greenhouse gas emissions and 20% of global wastewater – is now scrambling to reduce its environmental impact against the backdrop of the harsh effects of climate change.

Macy’s is one of the country’s most storied department stores, founded over 150 years ago. As the store looks to set itself up to rectify years of flagging sales, it has turned to ESG to fuel its future. In 2022, Macy’s announced that it will spend $5 billion by 2025 on three pillars of social purpose – people, communities, and the planet – to help shape a more equitable and sustainable future. Legacy companies like this are now realizing that success in the future is tied to meeting the needs of customers and employees, who want the organizations they purchase from and work for to be socially responsible.

What to do if you’re here: Look for quick wins to establish a foundation for ESG. Try to move performance first, but also evaluate the need to shift perceptions.Start sharing ESG data more openly to socialize ESG performance with stakeholders, emphasizing a commitment to accountability.

Set an ESG ambition and agenda to identify the next steps to start delivering on their goals. A transformation plan can help outline how a company must change for this new chapter of growth. Additionally, join industry or issue-based coalitions to build understanding, commitments, and relationships.

METHODOLOGY

ESG PERFORMANCE SCORES: In our analysis, we used 2022 S&P ESG scores to identify companies’ performance on ESG. Unlike ESG datasets that rely simply on publicly available information, S&P Global ESG Scores are informed by a combination of verified company disclosures, media and stakeholder analysis, and in-depth company engagement via the S&P Global Corporate Sustainability Assessment (CSA).

CUSTOMER PERCEPTIONS OF ESG: To determine customer perceptions of companies’ ESG performance, we leveraged our 2022 Prophet Brand Relevance Index ® (BRI) data. The BRI measures brand relevance – relevance encompasses all the elements required for a strong brand and healthy bottom line, including high demand, strong appeal and products and services that add value to a consumer’s life.

Prophet asked more than 13,500 consumers in the U.S. about the brands that matter most in their lives today. We measure their relationship to 293 brands in 27 categories, looking closely at 16 attributes.

Whether you believe ESG is strategic to your company’s growth or that your customers are prioritizing ESG in their purchases, it is vital to recognize and address any ESG performance and customer perceptions gap. Otherwise, your company may miss opportunities to connect with ESG-minded customers.

The first step to addressing your ESG performance vs. perceptions gap is understanding where your company is today. Once you’ve defined that, the steps we’ve outlined will help guide you toward ESG leadership.

This article is a part of our ESG Performance vs. ESG Perceptions series analyzing the gap between what a company does and what its customers think it does on ESG. Stay tuned for our next analysis featuring our new 2023 BRI data!

On-Demand Webinar: Innovating Your Way to Business Resilience

You cannot predict when or from what direction disruption will come, but you can use innovation to build a resilient business.

55 min

Given the turbulent global economy and widespread cutbacks, Prophet’s innovation team had some burning questions. What makes a business resilient–not just able to survive tough times but thrive?

We intuitively believed there was a connection between innovation and resilience. But we wanted to know if others thought that, too. So, we talked to 300 senior global business leaders across 30+ industries. We learned that innovation and resilience are connected, and organizations that are both innovative and resilient are 2X more likely to exceed their financial targets and 3X more likely to create more shareholder value than their competitors.

As we continue to unpack our findings, we’ve got plenty of new questions, which is why we recently invited a few innovation experts to join us for an on-demand webinar. Professor Jan-Erik Baars, who teaches industrial design at the Lucerne School of Business in Switzerland, and Chris Reinke, vice president of design and product development at Masonite, an industrial manufacturer.

Below are a few key highlights from that discussion.

Defining Innovation

Innovation is “about solving the problems people care about,” saysReinke, who formerly directed design at Bose. “Innovation needs to be uniquely relevant, hard to copy and something your customers want to pay for.”

But in hisexperience, many companies rely too much on their history and current knowledge. They’re reluctant to look far enough into the future to understand what might happen next. As a result, these companies tend to be slow to pivot and capture the next growth opportunity.

“The viewpoint of the organization has a huge influence on its ability to be innovative and resilient,” says Baars. He spent nearly two decades in design at Philips. During his time there, he noticed that future casting was specifically assigned to the inventors of the organization, while business managers were limited to a much shorter horizon.

“If you don’t allow an organization to open for larger and longer horizons, you will not have enough time and stamina to understand customer needs and respond accordingly to develop something truly meaningful,” Baars says. “You can’t sketch something out on a napkin and expect to have it ready next quarter.”

Our research confirms that the most innovative companies are explicitly organized to innovate on multiple time horizons, simultaneously. They work hard to advance organizational capabilities. “They’re like successful musicians,” Baar says. “They’re dedicated, disciplined and committed. They stick to the plan, grow, learn and improve. “Layla Keramet, partner and EMEA head of Prophet’s Experience and Innovation practice, believes there are three tiers to innovation opportunity:

We are not using the existing technology, product or solution in a way that can improve our human condition, and there is an opportunity to optimize and make it better.

People are making a significant shift to a new type of product and service, therefore driving the demand for innovation.

The technology, product or solution doesn’t have use cases for today, but we think it will in a plausible future.

Financially Thriving Companies Invest in a Diverse Range of Innovation Techniques

No matter which path companies are on, they can benefit from increasing the number of innovation tactics they use. Our research asked business leaders to identify which best-practice innovation techniques their organizations consistently rely on. Those that describe themselves as innovative and resilient use between five and six of these innovation techniques, on average. Companies that were neither innovative nor resilient used only 3.5.

That surprised us, especially since these tactics are widely known in the innovation community and general business world. Baars, on the other hand, wasn’t shocked at all.

“Most companies are dominated by management thinking,” he says. “They are very focused on output and time to market, even though that makes no difference to the consumer.” Yet that type of thinking tends to limit the variety and scope of innovation techniques.

Becoming more innovative requires “a change in the culture so that these techniques can be introduced, accepted and deployed.”

Innovation must be more than just a function. Building an innovation lab and detaching that group isn’t useful. “It’s like having a satellite with nothing to satellite around,” Baars says. “Innovation has to be a part of the core business.”

Companies that aren’t sure where to begin should start small and build from there, advises Reinke. Look at products that have proven successful and ask, “How can we make them better? What does the future look like?”

Masonite recently completed an activity with Prophet that looked to 2030. “We created a vision that enables us to walk back to the current day and understand where we are going with our product line,” says Reinke. “Now, we have a roadmap.”

The C-Suite Must Have Skin in the Game

Through our research, we discovered that only 11% of senior leaders set and are accountable for their organization’s innovation agenda. That didn’t surprise Baars, “Most companies are dominated by people with MBAs. They’re not trained in the company’s primary activity, which is creating impact for customers. Very few have degrees such as a Master of Business Design, which trains people to understand the inherent uncertainties of design thinking and set innovation agendas.”

“In many organizations, there is an over-representation of traditional business managers and an under-representation of designers and engineers,” Baars says. “So, they focus on driving operational excellence and efficiency, and not on creating an impact for customers.”

Final thoughts

Our recent research and conversations with innovation leaders demonstrate that an organization’sinnovative strengths correlate with its resilience, the kind of bounce-back flexibility all companies need to prosper in changing markets. As innovation leaders make their case for corporate support, they should enlist the involvement of the C-suite to spark new cultural thinking and organizational strategies.

In this year’s State of Digital Transformation report, we set out to identify the key differences between the businesses that are succeeding at digital transformation, and those that are still struggling. We surveyed over 600 executives from North America, Europe and Asia across a range of industries to highlight not only their current digital capabilities but the key investments and choices they made that got them to where they are today. By separating the responses of high performers and average performers, we identified key characteristics of companies that successfully met their transformation goals.

This report serves as a benchmark for what digital maturity looks like in 2023 and charts a path forward for businesses that are looking to drive growth and thrive in the next wave of digital transformation initiatives.

Key Takeaways:

The majority of companies (45%) chose business growth as their top goal for digital transformation, followed by innovation (45%) and efficiency (42%).

Top-performing companies tracked metrics like innovation (36%) and digital literacy (32%) to measure digital transformation success, while average performers tracked business performance (42%) and efficiency (40%).

Limited budgets (34%) and a resistant culture (27%) were the top obstacles to digital transformation success.

Despite challenging economic times, 42% of digitally mature companies were accelerating their digital transformation efforts this year.

Top-performing companies were more likely to have their digital transformation led by the CEO (33%), compared to average performers where the CIO or CTO (36%) were more likely to be in charge.

The top transformation priorities for companies were upgrading technology (50%), achieving operational efficiency (34%) and getting more value from data (32%)

How ASUS is Building Leadership in Sustainable Technology: A Conversation with TS Wu

ASUS’s Chief Sustainability Officer shares how the brand’s “Engineering Spirit” shapes its ESG strategy.

In the face of increasingly complex compliance requirements and growing economic turbulence, a robust ESG strategy has become indispensable for a company’s growth. While today’s corporations often operate in structured and specialized siloes, a successful ESG strategy requires heightened collaboration across all stakeholders in order to find solutions to complex challenges. In our work, we found that companies prioritizing ESG initiatives often excel at identifying innovative solutions to unlock growth opportunities.

Global technology brand ASUS has long been an industry leader in ESG strategies and sustainable growth. In 2021, ASUS furthered its efforts by launching the “2025 Sustainability Goals,” committing to 100% renewable energy usage by 2035. As part of this initiative, ASUS worked with Prophet to deepen its ESG strategy and narrative. In January 2023, ASUS released its new ESG slogan at CES – “Sustaining an Incredible Future.”

Cecilia Huang, a former partner at Prophet, sat down with TS Wu, chief sustainability officer of ASUS Group, to discuss how ASUS imbues a strong purpose and ESG strategy into its organizational culture to drive uncommon growth.

CH: In recent years, the technology industry emphasizes more sustainable growth while confronting various challenges, such as compliance requirements and market shifts. What measures has ASUS taken to overcome these challenges as well as elevate its ESG strategy?

TW: I have seen in the past few years that societal topics such as environmental protection have become increasingly mainstream, and ESG strategies and organizational resilience are more valued. However, there are still many challenges that businesses need to identify and solve urgently. Externally, meeting compliance standards and consumer demands to remain competitive requires rapid iteration; internally, organizations face issues such as talent retention, innovation, brand building, and profitability.

In order to meet these challenges and effectively integrate ESG, ASUS has implemented three major initiatives:

First, from “maximizing the interests of stockholders” to “maximizing the value for stakeholders”: In the past, ASUS focused on maximizing stockholder value. But now, we recognize that for a business to achieve long-term success, it must meet the expectations of all stakeholders.

Second, from “emphasizing technology” to “emphasizing purpose”: The guidance of organizational culture is crucial. Chairman Jonney Shih has always insisted on promoting ASUS’ “authentic and pragmatic” culture internally. He once shared the book, The Heart of Business by Hubert Joly, former CEO at Best Buy, which advocates for leadership and business that starts from the heart. Such a culture allows ASUS employees to focus less on external awards and recognition and more on the original intent and vision of the company. We have been following this philosophy to garner enthusiasm towards ESG, building our strategy from the inside out.

Third, from “passively avoiding risks” to “actively achieving sustainable growth”: In the past, our focus for ESG has been on risk reduction and legal compliance. Now we are going a step further, with an eye on brand growth and adapting to the future. We’re working to proactively create shared value through the development of ESG strategies that promote sustainable growth.

CH:When did ASUS’s commitment to ESG begin? What experiences can you share from what ASUS has learned over the years?

TW: ASUS has undergone six stages towards developing our ESG strategy. Starting in 2002 the seeds of ESG were planted at ASUS. Customers began paying more attention to product sustainability. We set up Green ASUS under the Quality Assurance Center to meet the demands of the market and our customers. Subsequently, in 2008, ASUS established the ASUS Foundation to invest more actively in social impact programs in order to improve our corporate image and reputation.

The turning point was in 2010 when ASUS transitioned from passive involvement into active efforts. We proposed standards for ourselves that were higher than industry regulations and sought to bring more environmentally friendly products to customers, with the aim of gaining a greater competitive advantage and penetrating a broader international market. In 2016, we went a step further and embedded sustainability as a parameter in product design, process transformation, organizational design, supply chain management and other processes, formally incorporating ESG into our strategy.

Now, based on the existing foundation and achievements, we are exploring how ESG can become an important pillar of our company’s future strategic growth.

After undergoing the six stages of ESG transformation, we understand how to deal with various challenges and recognize the importance of making ESG a core strategy on its own. By setting up a dedicated department and adding the role of chief sustainability officer, we’ve created a culture that allows different departments across the company to understand the importance of ESG, enables experts to help advise on and implement initiatives, and deeply roots ESG within ASUS.

CH:You mentioned that ASUS’s leadership places great importance on the original intent of the company. What role do they play in driving ESG across the organization?

TW: I believe the role of leaders in the early stages of ESG development is far greater than in the later stages. Leaders can guide the organization early on and ensure its implementation is not just a superficial branding project.

At ASUS, our chairman and CEO both lead by example, personally participating in the ESG committee to discuss ASUS’s sustainable business strategy and philosophy. Employees understand that the leadership greatly values ESG Therefore, each department incorporates ESG accordingly and soon sees the benefits of ESG in building the business, thus forming a positive feedback loop.

Different departments will invite the sustainability team to participate in their strategic planning with the hope that the success of new products will not only come from new functionalities but also from the sustainable features in product design. To us, this signifies real change.

CH:ASUS’s “Engineering Spirit” is unique. How does it relate to ESG initiatives? How do the two influence each other?

TW: “Engineering Spirit” is the DNA of ASUS’s organizational culture, and our ESG strategy is connected to it in two ways.

The first is data-based measurement and technology-centric management. This means that the benefits of sustainability-related actions can be evaluated and managed through quantifiable indicators. Taking environmental profit and loss assessment as an example, ASUS quantifies the air pollution, water pollution, greenhouse gas, and waste pollution generated throughout the process of laptop computer production. This allows us to understand the environmental impact of suppliers in each segment of the value chain and helps us optimize resource allocation. In addition, this initiative allows us to clearly convey to stakeholders ASUS’s emphasis on sustainable growth and the value it brings to society through real and visible figures.

The second is design thinking. In this realm, we pursue the concept of “beautiful, practical, and environmentally friendly,” and incorporate products’ design, weight, thinness, and ESG dimensions into product parameters. We resolve conflicts through technology and design thinking to find the optimal solution.

As a result, the focus on sustainability has permeated ASUS’s product design, process design, organizational design, and supply chain management. Its importance is highly valued at each stage of the process.

CH:Lastly, in terms of organizational management, how should companies build a better future through improved organizational processes, values, and talent development?

TW: I believe a shift in strategic and operational thinking is key. While competition is inevitable, a change in mentality is essential. Organizations in the past emphasized the division of labor and efficiency, but ESG-led organizations emphasize collaboration and connection. Therefore, ASUS’s ESG department plays the role of a facilitator and guide across the organization, rather than a commander. We never require other departments to replicate successful cases. Instead, we use them as experience sharing and a knowledge base, so that each team can reasonably choose resources and invest pragmatically based on real business conditions, ultimately promoting sustainable growth across the company. Externally, ASUS also cooperates with other technology companies to launch a Climate Partnership, with the goal of working jointly on issues that cannot be solved by a single company.

Furthermore, talent is indispensable to ESG. We do two things to cultivate our talent development. First, we encourage independent innovation. In our organizational design, ASUS gives individuals greater autonomy to foster innovation. Second, we cultivate interdisciplinary talent. We believe that it is very important to develop employees that can coordinate and integrate different domains, especially for ESG-oriented organizations. As an organization, we are committed to shaping our employees from specialists into generalists, connecting fragmented knowledge and creating higher value.

Finally, establishing values is very important. To quote our chairman: “Long-term profitability is the standard by which the market measures the success of a company. What truly outstanding companies have in common is that they have a clear business philosophy and consistent values, and they know how to communicate with key stakeholders. When an organization can think deeply, redefine the role of sustainability, and use its unique core capabilities to meet the needs of the environment and society, the performance of the company will be even more outstanding.”

As shown in our conversation with TS Wu, the key to driving a successful ESG strategy to realize transformational growth lies not only in technological innovation and brand story but also in holistic planning across multiple strategic dimensions, including brand purpose, organizational management and collaboration.

For business leaders, the starting point is to ensure the right mindset that focuses on creating value for all shareholders, building a purposeful business and actively driving sustainable growth. It is important to take a long-term view to transform the organization and culture with a strong purpose. If done right, an ESG-led strategy can align the company and become the central force for unleashing uncommon, sustainable growth.

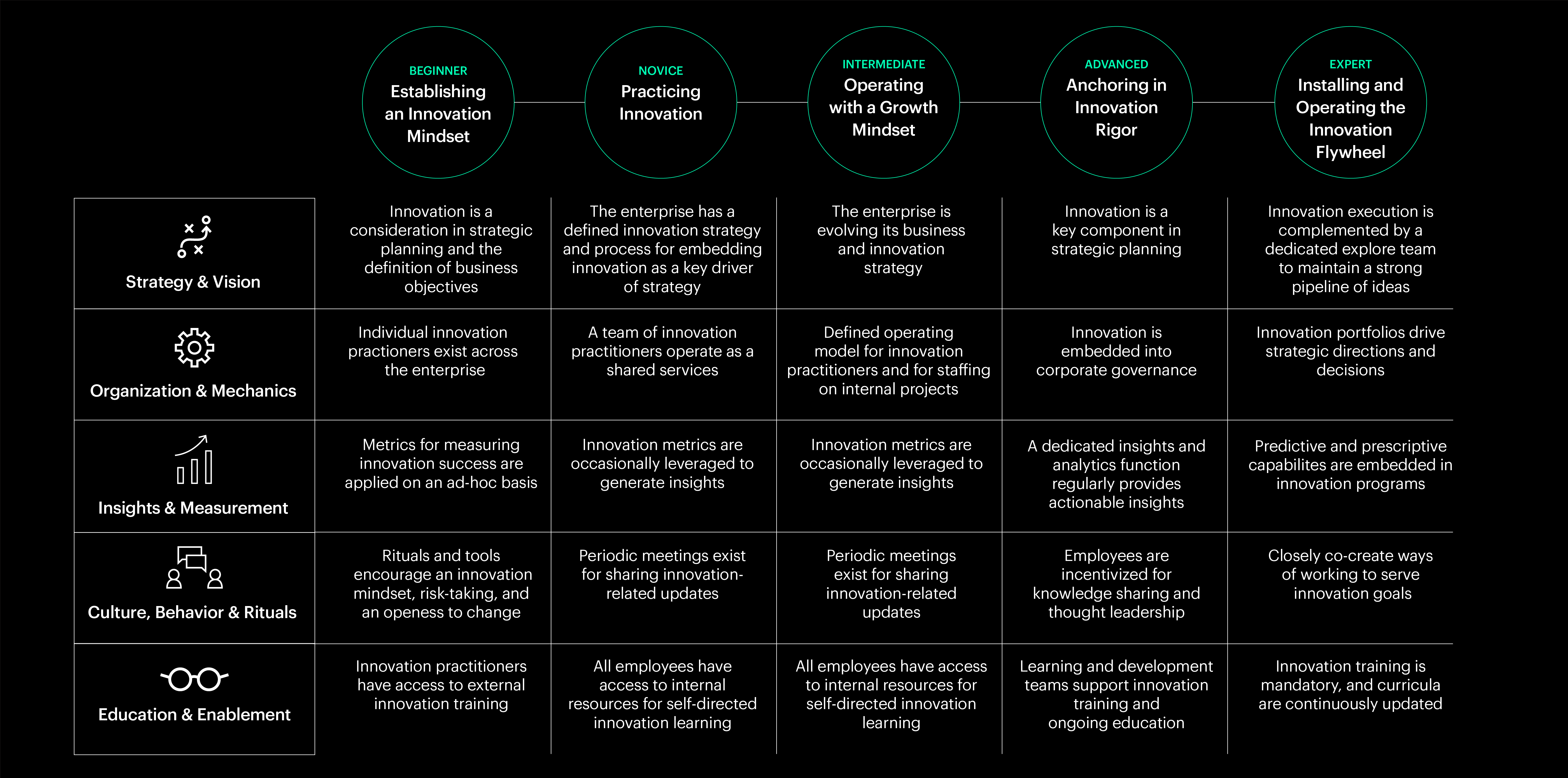

Introducing the Innovation Maturity Model for Financial Services

Prophet’s Innovation Maturity Model helps organizations establish and operate high-powered innovation engines.

Innovation – more and more – is what every financial services company seeks as the primary means of driving growth. That’s true because innovation is increasingly what separates market leaders from also-rans.

But for all the investments in innovation, most organizations struggle to generate the returns they’re looking for or produce the growth that innovation is supposed to unleash. For more on the barriers to innovation and – more importantly – how to get over them, read our recent research report, Winning the Innovation Game in Banking.)

In the intensely competitive financial services sector, it is not enough to innovate every now and then. Rather the goal is to establish a rigorous practice of innovation and to make it a standard part of ongoing operations. The vision is to establish a high-performing innovation engine that continually identifies innovation opportunities, explores those ideas via prototyping and gated investments and efficiently moves meaningful innovations to market. Such a disciplined process is necessary to avoid the common pitfalls that make repeatable innovation an elusive target for many companies.

Introducing… the Innovation Maturity Model

To help banks, insurers, and investment managers industrialize their approach to innovation, Prophet created the innovation maturity model. This model helps organizations:

Assess their own innovation capabilities and opportunities

Identify the barriers – technological, process, human, cultural – inhibiting innovation

Establish tangible innovation goals and actionable plans to overcome those barriers

Define a roadmap to establishing repeatable innovation capabilities

The innovation maturity model inspects five dimensions of the business that are critical to enabling innovation:

Strategy and Vision

Organization and Mechanics

Insights and Measurement

Culture, Behaviors and Rituals

Education and Enablement

Within each of these areas, the model defines varying levels of maturity – beginner, novice, intermediate, advanced, expert – so organizations can understand where they are today and what to aim for tomorrow. For instance, an organization with expert-level capabilities in organization and mechanics would involve the entire enterprise in using innovation portfolios to drive strategic directions and decisions, with all employees aligned to the innovation strategy and with specific responsibilities to drive that strategy forward.

In terms of education and enablement, beginner firms will be those that provide access to and funding for external training for dedicated innovation practitioners. Intermediate firms will have innovation teams in place to help drive behavioral change across the organization and support wider education efforts. At the expert level, innovation training and education will be a mandatory part of onboarding and learning and development programs, with continuously updated curricula and regular use of outside resources for insight and inspiration.

The innovation maturity model reflects our market experience in terms of what works in driving breakthrough innovations. Further, it’s designed to establish cultures that prize risk-taking and experimentation and instill operational discipline relative to innovation. Such organizations are capable of both acting like a startup and investing like venture capital firms. As we highlight in our report, “Winning the Innovation Game in Banking”, it’s a matter of building a portfolio of innovation ideas based on deep customer insight and then rapidly testing and refining those ideas through pilots and MVP launches into the market.

The Many Forms of Innovation

Because innovation can take many forms, our innovation maturity model provides the core insights that can point the organization in the right long-term direction. To put the model into context, consider how the organizations below are evaluating the different ways to set up their innovation engines and flywheels.

Allianz: An ‘Always On’ Dedicated Innovation Center: Allianz has launched dedicated innovation centers to engage a range of partners, including FinTechs, start-ups and firms in other sectors, to develop entirely new insurance solutions for specific industries, including travel and automotive. This looks like a winning strategy considering the pressure on insurers to innovate in the face of intensifying risks from climate change, relentless cyber threats and the growing protection and retirement savings gaps.

JP Morgan Chase: A Condensed Annual Innovation Event:

JP Morgan Chase fills its innovation pipeline in creative ways, too. It holds an annual Innovation Week, bringing together employees in more than 400 events focused on generating new applications for artificial intelligence, machine learning and other enabling technologies, while highlighting specific business issues, opportunities, and current technology trends. It also held a digital innovation competition to generate transformative ideas to enhance the client and advisor experience. Such broad-based approaches reinforce that innovation is part of everyone’s job.