Webinar Replay: B2B Leaders Series feat. Randstad & Boston Medical Center

B2B leaders discuss the challenges of building the right culture and systems for digital transformation.

59 min

Watch the webinar replay in which you’ll learn about the challenges that B2B organizations face in undertaking transformation on a large scale and how they address them. The discussion features Rene Steenvoorden, Chief Digital Officer, Randstad, Heather Thiltgen, President, Boston Medical Center/WellSence Health Plan, and Fred Geyer, Senior Partner at Prophet, who were interviewed by Joerg Niessing, Senior Affiliate Marketing Professor at INSEAD.

Two of the participants, Fred Geyer and Joerg Niessing, co-authored ‘The Definitive Guide to B2B Digital Transformation’. Get your copy of the book here.

If you have any questions or would like to learn how our Marketing & Sales practice helps clients identify a clearer path to a digital transformation that powers growth with real and measurable results, contact us today.

To Transform Digital Selling, Must Sales & Marketing Converge?

Despite historical differences, sales and marketing teams now see that more collaboration equals more revenue.

In our 2020 State of Digital Selling global research report, we found a consistent theme: the more in sync sales and marketing was, the better the outcome for sales, in terms of revenue, customer satisfaction and other metrics. That, and the tremendous growth of executives managing both functions—LinkedIn has identified the Chief Revenue Officer as the fastest-growing C-Suite role—has led to an emphasis on studying this convergence as part of my research on the digital transformation of sales. In this post, I’ll look at the impact of this convergence, which was discussed in my recent webinar with our research director, Omar Akhtar.

Convergence or Collaboration?

Convergence of sales and marketing today is embodied by the rise of new C-suite leaders, often with the Chief Revenue Officer (CRO) title, who manage both sales and marketing—often with a new combined Revenue Operations team supporting both. What is the line between convergence and collaboration? It’s undoubtedly possible for these teams to align and collaborate so well that they could appear converged and achieve the same benefits. A question my research will answer this year is: what points of convergence or collaboration are required to digitally transform sales?

Clearly, the trend is in favor of convergence as shown by research indicating the CRO title is the fastest growing in the C-suite. What benefits are CEOs seeking with convergence?

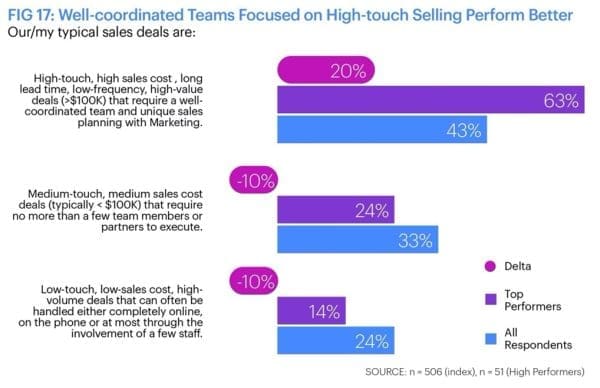

An important benefit was a clear finding in my recent report which found the high performance of Account-Based Marketing (ABM) and Account-Based Selling (ABS). One factor we evaluated was the type of digital sales model employed, in terms of scale as measured by the size of the deal, lead time and level of collaboration employed. Our research found that high-touch, high-value, long lead-time sales that rely on a well-coordinated team and unique sales planning with marketing paid off well. Top performers (represented in the purple bars in the chart below) follow this model, and it was even the most frequent model among average performers as well (shown by the index in blue).

The benefits of collaboration are high. Consider the enormous investment marketing teams have made in technology, data, and skills development. Much of that investment can be leveraged by sales to digitize selling. By sharing the same data, enablement tools and customer experience platforms, costs can be reduced, and effectiveness increased, as near-real-time decisions can be used to nurture leads and provide the intelligence needed to up-sell, cross-sell and re-sell.

Barriers Are Deep-Rooted

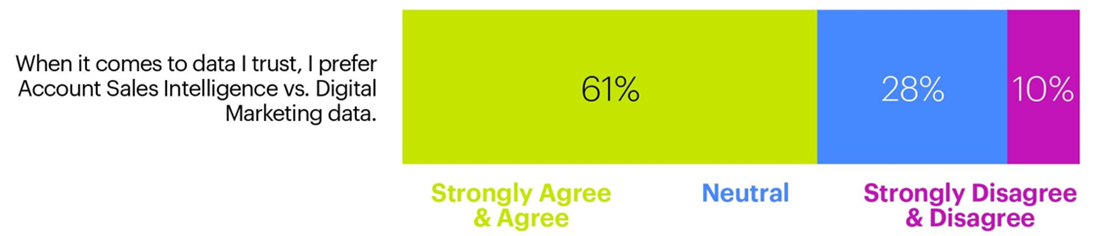

Too many times, sellers and marketers don’t see eye-to-eye. In a recent conversation with a marketing leader, we discussed whether this is a left-brain/right-brain issue: marketers being more analytical and sales being more relationship and instinct-driven. Yes, these are broad generalizations, but they hold in my experience too. This impacts trust. Sales’ digital transformation will rely on new levels of trust among sales teams for the data and tools they use to navigate digital selling. This trust is lacking among the average digital seller, but high among top performers. For example, when we asked sellers if they trusted marketing’s data, 61% reported that they don’t—they want their own.

Perhaps the most fundamental challenge is misaligned priorities. In our recent 2020 State of Digital Marketing report, we found that marketing deprioritized sales-focused efforts, such as creating more sales qualified leads to buyers, supporting sales team productivity and growing e-commerce.

“An equal partnership in the form of an executive steering committee—or through CRO convergence—can address these barriers.”

Building trust is essential to sales’ transformation: if, as I believe, sales needs marketing’s help to digitally transform, we must tackle cultural mindsets and increase alignment focus. It may not be easy for sales leaders to accept marketing’s help given the risk of marketing dominating sales’ digital transformation, at the expense of what makes sales different from marketing. An equal partnership in the form of an executive steering committee—or through CRO convergence—can address these barriers.

What It Means & What You Can Do

The place to start is to look at the key touchpoints between sales and marketing that represent hand-offs, which tend to be problematic. The table below shows what I believe to be those key areas and the relative digital maturity of marketing and sales. As you can see, marketing and sales are complementary:

Planning. Much of planning integration is solved when sales and marketing collaborate through ABM/ABS. I’ve spoken with one large manufacturing business that plans GTM strategy holistically: team members from marketing, sales and service create a strategy through carefully structured workshops, spanning up to 5 days together working as a team. This not only ensures alignment, but time together can bridge cultural barriers.

Content. The content touchpoint includes selling assets, like playbooks, scripts and content that nurture leads to conversion. This area is most often led by marketing, but I continue to hear sales complain about the content they’re asked to share: it may not be easily personalized for the buyer, or the seller may not know how to position it for the prospect’s unique needs. Often training is the heart of the issue, but part of the root cause is a misalignment in strategy and insights. Sales need to be much more involved in content strategy and learn the tools necessary to use and measure content effectiveness.

Lead Management. Best next moves during lead nurturing are important in digital selling, because of the near real-time response that must be coordinated between sales and marketing. For example, after a lead downloads a white paper provided by marketing, what shared customer intelligence signals the best next step for sales? I’m also questioning whether lead management belongs in a digitally transformed sales organization that can do its own prospecting. As sales become increasingly comfortable with automation and data, the definition of a “marketing qualified lead” and “sales qualified lead” will surely evolve.

Data. My digital sales research has shown that top performers align performance metrics between sales and marketing, such as customer satisfaction, revenue goals, etc. In fact, there was a 34% spread in digital selling maturity between the index and top performers when KPIs, incentives and compensation were aligned between teams. But I also found that sales don’t necessarily trust marketing’s data—which brings us back to the cultural issues that must be addressed. The solution is also found in last year’s 2020 State of Digital Selling report: top performers collaborate with marketing on both a data architecture and technology stack roadmap to keep aligned—much more so than the index of average performers.

Technology. Technology touchpoints are dual: internally, represented by sales and marketing enablement (e.g., CRM, SFA, etc.), and externally, customer-facing digital experiences, such as websites, apps and social media. Marketing is leading CX work today, but as sales become more digital, they need to be part of a highly collaborative process with marketing and service teams to create a seamless customer experience that crosses their functions.

Ongoing Teamwork. Customer experience worries for the sales team don’t stop after the sale. Some of the most integrated sales and marketing teams work within a growing part of the economy: Software as a Service or SaaS. For example, a salesperson who has sold a SaaS HR system needs to understand whether their customer is utilizing the system to its full potential. If the customer is underutilizing the system, they may have bought the wrong product; if they’re overutilizing the system, there’s an upsell opportunity. Even if your product isn’t SaaS-oriented, it helps a lot to think of it that way by demanding marketing and service customer insights that may guide your sales strategy for an account.

The insurance game is changing. The past year has seen life completely upended for insurance agents, whose success once hinged on a certain skillset, often with physical touchpoints. While many insurance providers have raced to increase digital selling efforts in reaction to COVID-19, the results have been mixed. It’s going to keep changing too, so it’s time to adapt to fuel a post-pandemic recovery and lead the way to future growth.

Embracing Digital Selling from our dedicated Financial Services practice outlines a roadmap for digital selling with the steps to take now in order to create a strategy that supports new digital tools, efficient models and the development of the necessary capabilities.

In this report you will learn:

The four primary challenges insurers need to overcome to compete in the digital world

How insurers can maximize digital selling efforts for both short and long term growth

A roadmap to guide how to install a structure that helps agents navigate a fast-changing, digital selling environment

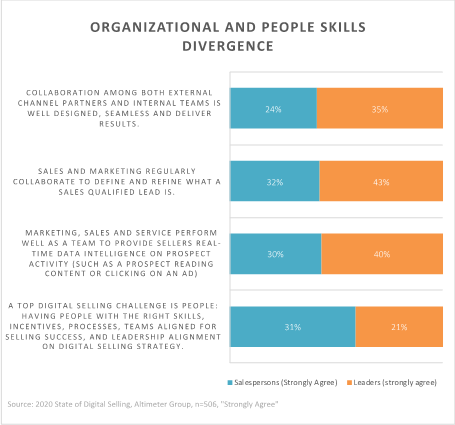

Why Are Leaders More Optimistic Than Sales Teams About Digital Sales Transformation?

Our research reveals a scary disconnect: Leaders are more positive about transformation than their sales staff.

In our 2020 State of Digital Selling global research report, we found disconnects between the views of front-line sales staff and their leaders. Leaders view their progress in digital sales transformation more positively than sales staff in three areas: technology, customer experience, and organization/people-readiness. This post delves into those disconnects to help leaders and staff better understand their respective sales transformation realities and ends with recommendations on how to close the gap.

Technology & Data

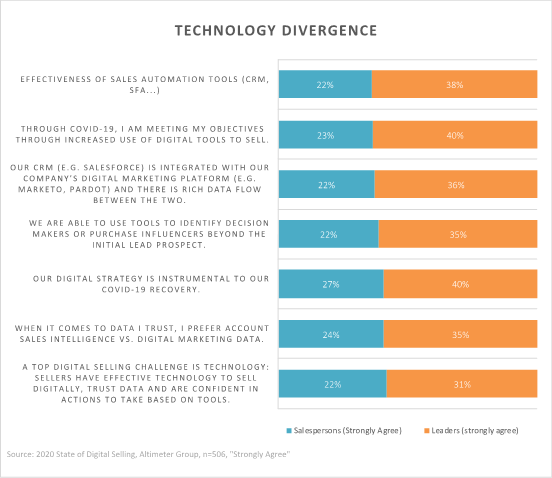

For front-line sales teams, technology is far less effective than what their leaders believe. The largest gap was the effectiveness of foundational CRM and sales automation tools, which only 22% of front-line team members rate “highly effective” vs 38% of leaders. Only 23% of staff strongly believe that increased use of digital tools has helped them meet their objectives through the COVID-19 pandemic, vs 40% of sales leaders.

“The root cause of the tech gap is skills and training.”

One clue that points to the root cause of the tech gap is skills and training: 31% of sales staff say that it is the biggest digital selling transformation challenge, vs. just 21% of leaders—who instead name technology as the greatest transformational challenge.

Customer Experience

Front-line sales staff view customer experience much differently than sales leaders. The front-line would like to expand buyer digital tools to match buyer preference and self-service (41% front line vs. 29% leaders). Front-line sales teams understand CX from direct engagement with customers and prospects, while sales leaders are a step removed and often rely on IT or CX experts to recommend digital tools. To tackle this disconnect, leaders should engage the front-line more in CX development.

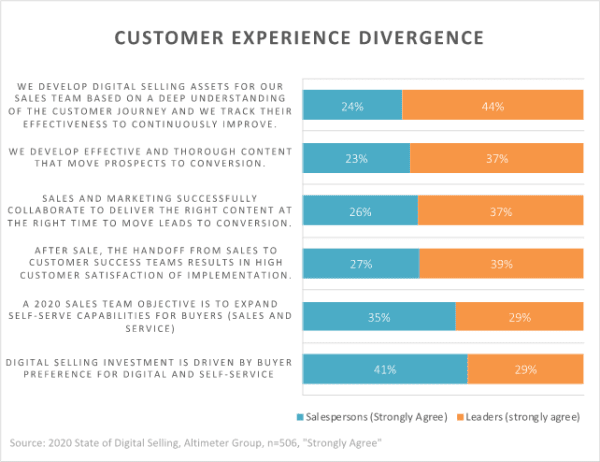

The biggest disconnect was the value of content and selling assets: only 24% of front-line staff strongly agree they have the right to sell assets based on the customer journey vs. 44% among managers. Reinforcing this disconnect, only 26% of sales staff strongly agree that sales and marketing successfully collaborate to deliver the right content at the right time to move leads to conversion (vs. 37% of sales leaders). At the end of the sales funnel, only 27% of front-line staff strongly believe the handoff from sales to customer success teams results in high customer satisfaction (vs. 39% of leaders).

In addition, when it comes to content, I hear a consistent story from front-line sales: they don’t know how to select, customize and share (within the customer’s context) content. All too often, content is shared without adequate context from the seller, and this leaves the customer with less reason to read it. This is a training issue. Part of the problem could be the complexity of tools sales teams are asked to use, but training on the “why” and “how” of content is also a challenge.

People & Organization

Front-line sales staff perceive sales and marketing collaboration as much less effective than leaders do. Only 24% of sales staff view collaboration as effective (vs. 35% of leaders). This attitude shows up in two areas: the ability of sales and marketing to collaborate and refine what a sales-qualified lead is (32% staff vs. 43% leaders) and the provision of timely customer intelligence to understand prospects (30% vs. 40%).

No doubt, part of this may be a visibility problem: leaders are more likely to work cross-functionally (including with marketing) than front-line sales. The more problematic issue is the front-line’s view that sales-qualified leads aren’t well-defined, and the fact they’re not getting adequate customer intelligence to understand leads. This should trouble leadership, as both of these issues have a direct impact on the front line’s results. Leaders likely have metrics that indicate access to customer intelligence, but it won’t tell them how effective it was in closing a deal. Of course, an upward trend in usage data indicates growing reliance on it and so is a good indication of ultimate usefulness. If leaders don’t see an upward trend, there’s likely a problem that can be uncovered through direct conversations (or field polling) of the front line—something metrics won’t tell managers.

What It Means & What You Can Do

It’s not unusual to see differences in attitudes by role in our research, but this consistent gap between front-line sales staff and sales leaders drew attention because it was persistent (across all questions we asked). These gaps could hamper the progress of those organizations seeking to digitally transform their sales teams and so are worth paying attention to. Keep the following in mind to successfully transform sales:

Regularly poll front-line staff to understand their perspective and compare to related metrics like content effectiveness and sales tool enablement adoption. Sales managers and leaders should question those metrics that indicate front-line use of data, content and tools without proof that the front line is truly getting the value A salesperson downloading a white paper to share with a prospect is a vanity metric. It doesn’t indicate whether that content was effectively shared and made a difference in converting the prospect.

No one likes to take a great salesperson off the front line, but you need to in order to best match transformation tactics to real-world experience. If you have a digital selling transformation council or team, include some of your best sales staff to ensure your whiteboard ambitions address real-world needs. In addition to basic capabilities, tools, etc., involve the front-line in the selection and prioritization of metrics leaders see when it comes to sales enablement.

Regularly analyze buyer and customer surveys to understand key disconnects, e.g., front-line sales staff see the need for additional customer-facing digital tools that leaders are clearing missing. You’ll discover those gaps—and others—by better understanding digitally-savvy buyers.

Customer Relevance: 5 Ways That B2B Brands Differ From B2C Brands

B2B brands may make it easy for customers to buy, but they disappoint on consistency and emotional connection.

To be the relevant choice, the go-to brand for customers has been shown to drive profitable growth and to help insulate businesses from unexpected shocks such as COVID-19. The sixth annual Prophet Brand Relevance Index®, which studied 228 brands among 13,000 consumers, reveals how brands that rely heavily on serving B2B customers build relevance differently than brands that focus only on B2C customers.

As part of the study, we compared 57 brands with significant B2B businesses such as Amazon, General Electric, FedEx and IBM with 171 pure B2C brands such as Lego, Peloton, Netflix and Etsy. Both cohorts of brands with significant B2B business and the pure B2C brands increased relevance to their customers over the course of 2020. The B2C group had a greater range of high and poor performers with brands such as Peloton, Kitchen Aid and Lego in the top five and Popeye’s, Burger King and Facebook in the bottom three. Technology brands were the best performing in both the B2C and B2B cohorts. Apple led the pack followed closely by Amazon ranked tenth overall.

“The sixth annual Prophet Brand Relevance Index®, which studied 228 brands among 13,000 consumers, reveals how brands that rely heavily on serving B2B customers build relevance differently.”

When we analyzed the drivers of customer centricity and pragmatism, key differences appeared.

When compared to B2C focused brands, B2B reliant brands…

1. Meet Important Needs

On average B2B reliant brands outperform B2C-focused brands on meeting their customers’ important needs by a remarkable 28 percent. 3M for example, is rated 64 percent higher than the average B2B brand on meeting important needs and being a brand the customer cannot live without. That said, it is one of the worst-performing brands in the survey on making the customer happy by connecting with emotion.

2. Make It Easy

B2B reliant brands are 25 percent more likely to make it easier for their customers than B2C-focused brands. Microsoft, for example, performs a bit above the average of B2C brands on consistent performance and being dependable, but excels at making the consumers’ lives easier.

3. Don’t Deliver Consistently

B2B reliant companies are 17 percent less likely to perform as well as B2C companies on “consistent delivery.” GE is a typical example. It ranks in the top one hundred brands with very high customer scores on most dimensions of pragmatism, such as makes it easier and is dependable but ranks only average on consistent delivery.

4.&5. Fail to Connect Emotionally and Don’t Make the Customer Happy

This doesn’t appear to be a surprise as emotion is important for B2C brands but not to the same extent as B2B brands. What is surprising is the size of the difference; a 47 percent difference for happiness between B2B reliant and B2C focused brands. Adobe demonstrates the challenge. It outperforms other technology-oriented B2B companies such as HP and IBM on being a brand customers can’t live without but is rated 75 percent lower on makes the customer happy and connects with emotion.

The key takeaway for B2B reliant brands is to break out of the trap of trading off performance with emotion. Great brands, such as Apple deliver to both B2C and B2B customers, don’t make this tradeoff; so why should Adobe settle for it? The other key takeaway is to focus on technology. The most technologically advanced B2B brands we examined by industry outperformed their peers on meeting important customer needs and making it easy for the customer.

Learn more about brands in your industry

This post provides just a snapshot of the 228 brands evaluated in the 2021 Prophet Brand Relevance Index®. For more insights on this year’s top-performing brands, visit this website.

Our research shows companies are moving toward digital selling techniques faster than they’d planned.

Sales teams have had a tough year. The forced push into selling virtually through tools like social media and video conferencing have disrupted both sellers’ sales funnels and their customers’ journey. We’ve developed a tool to help you quickly assess your organization’s digital selling readiness for the key capabilities used by top performing sales organizations discovered in our 2020 State of Digital Selling research report. You don’t have to be in sales to find this useful: marketers will play a key supporting role in the digital transformation of the sales organizations they support.

Sales have watched for years (largely on the sidelines) as the influence of B2C e-commerce changed the expectations of B2B buyers, who now increasingly favor seamless digital experiences that make their lives easier. Many sales teams polished their LinkedIn profiles to engage prospects in the digital landscape only to realize that without great content and integration with backend CRM and SFA systems, those profiles are hollow attempts at transformation. Post-COVID, don’t expect selling practices to go back to “normal,” because there’s no undoing the changes in buyer and seller behavior the global pandemic has caused.

“Post-COVID, don’t expect selling practices to go back to “normal,” because there’s no undoing the changes in buyer and seller behavior the global pandemic has caused.”

Our 2020 State of Digital Selling global research report found that 73% of surveyed sales organizations will transition to digital selling techniques faster than planned. And McKinsey’s research found “Looking forward, B2B companies see digital interactions as two to three times more important to their customers than traditional sales interactions.” The question our research sought to answer is which capabilities are needed (and most important) to digitally transform sales.

What is Digital Selling?

Like any technology disruption, defining it in the early phases of adoption can be tricky. It’s sure to evolve as seller and buyer behavior continues to change. Here’s a starting point:

Digital Selling is the use of technology-focused commerce practices to meet the needs of digitally savvy buyers and by sellers to seamlessly integrate the sales funnel across marketing, sales and service.

Just as marketing has transformed into a technology and analytics-lead discipline, the digital transformation of sales is underway to position sales as an equal digital partner.

Don’t think of digital selling as entirely end-to-end virtual or digital experiences, but rather a practice that finds the right balance of the complementary offline and online forces. Our research found that top-performing sales organizations combine the human touch needed to influence and sell with digital enablement tools and analytics that give them a significant edge in key sales metrics, including win rates, quota achievement and customer satisfaction. In fact, the best sales team practices were based on the digitization of the Key Accounts sales model, in which a cross-function team of marketers, sellers and service pros focus on key account wins (see chart below).

In our research, we chose to study the digital transformation of sales from the perspective of the capabilities a sales organization needs to succeed.

The report breaks down each of these capabilities further into sub-capabilities that again show the gap between top performers against the industry average.

Building Relevance Through Relationship-Driven Marketing

Right-now thinking, content marketing and nimble messaging nurture customer bonds.

The 2021 Prophet Brand Relevance Index® (BRI), recently launched and as we sift through the top performers, it’s clear to us that relationship-driven marketing strategies are powering the strongest companies.

Now in its sixth iteration, the BRI is based on four core principles of relentless relevance, measuring whether a brand is customer-obsessed, ruthlessly pragmatic, pervasively innovative and distinctively inspired. But a year of pandemic, social unrest, political upheaval and economic uncertainty is causing some brands to soar and pushing others entirely out of the conversation.

To understand how consumers measure the most relevant brands, we closely study the specific relevance dimensions in the top-ranked brands. We see three clear consumer marketing trends executives can tap into, regardless of industry and category.

The “right now” consumer need: Lean into how you can help, then execute relationship-driven marketing

Organizations that are confident enough to jump into a pressing need, solve it fast, and communicate effectively are among the year’s biggest gainers. Top brands demonstrated an embracement of the relationship-driven marketing mindset.

Johns Hopkins Medicine, No. 8, vaults into the Index for the first time, primarily due to the creation of its widely-used COVID-19 dashboard. Launched in late January last year, when many people felt they weren’t getting the answers they needed from the government or media sources, it quickly became not just a trusted data provider, but also a source of daily contact.

As Black Lives Matter protests swept the world, many companies did little more than slapping a black box into their Instagram accounts. But Xbox, No. 19 and one of the Index’s biggest gainers, responded differently. It tightened rules around hate speech, sparking meaningful conversations among gamers worldwide.

And to pass the time during the pandemic, millions of consumers turn to KitchenAid, No. 3. It increases adoration by leveraging its Yummly food platform, with 26 million users and more than 2 million recipes, it elevates fans from mere cooks to domestic divas.

“Right now” thinking also includes launching new products and services that speak directly to the moment. These new offers go well beyond features and functionality. They address important emotive needs–and consumers reward that thoughtfulness. Chick-fil-A, No.39, is the only restaurant in the top 50. That’s a credit to compassionate introductions like family meal kits, well outside its quick-serve wheelhouse.

Content marketing: Keep your audiences engaged with core products & services

The most relevant brands are content juggernauts, using new agile processes, techniques and channels to create sprawling ecosystems. And these ever-growing hubs reach well beyond their central customer base, finding unexpected avenues to acquire new and potential customers. In doing so, they don’t just remain top of mind: They become constant companions.

“The best marketing and sales organizations have been focusing on speed skills for years now, reengineering both organization and culture to add more flexibility.”

Peloton, No. 2, isn’t only relevant because of its bikes, treadmills and the fact that – as gyms and fitness studios closed – people needed digital sweat sessions more than ever before. Its incredible rise started long before the pandemic and is directly linked to a smart, relationship-driven and agile content strategy, providing a constant stream of workouts, a “virtuous cycle,” built into a system that allows them to constantly retouch the content. With its commitment to supporting content throughout its lifecycle, its classes by now welcome millions of at-home meditators, yogis and weightlifters over and over again.

Coming in at No. 5 LEGO recognized the pandemic’s effect on adult’s normal social and leisure activities, the creative outlet brand for kids introduced several grown-up art projects, including Andy Warhol style murals and the Botanical Collection… LEGO also leads by creating an entire digital content ecosystem around its products, from movies to minimovie series and microsites designed around LEGO storylines, innovative tools and processes to drive customer-generated content.

Message molding: Shape the conversation

The best marketing and sales organizations have been focusing on speed skills for years now, reengineering both organization and culture to add more flexibility.

These brands entered 2020 more agile than their competitors. But as events unfolded, it became clear just how essential this is. Our BRI is filled with examples of brands as nimble as ninjas, continually updating their messages and flexing their agile muscles.

Take Sephora. It rises 36 places to land at No. 33, an astonishing gain in a year where industrywide, makeup sales plunged 19 percent. Few nights out give consumers little reason to buy cosmetics, however, Sephora keeps gaining relevance, with messages focusing on beauty as a key part of self-care.

Amazon, No. 10, offers a different example. Its sales are skyrocketing, reflecting the surge in e-commerce. Yet it recognizes that many consumers question its lack of transparency around employee health. So, it’s running an extensive ad campaign explaining the many ways it is working to protect its front-line workers.

Even amid intense upheaval in consumer behavior, marketing and selling strategies can help brands increase relevance–and revenues. To achieve uncommon growth, organizations must look for ways to deepen their relationship-driven marketing capabilities. This will help each respond to new needs and opportunities as quickly as they arise, invest in content that expands the brand’s universe and find ways to update messaging to meet the moment.

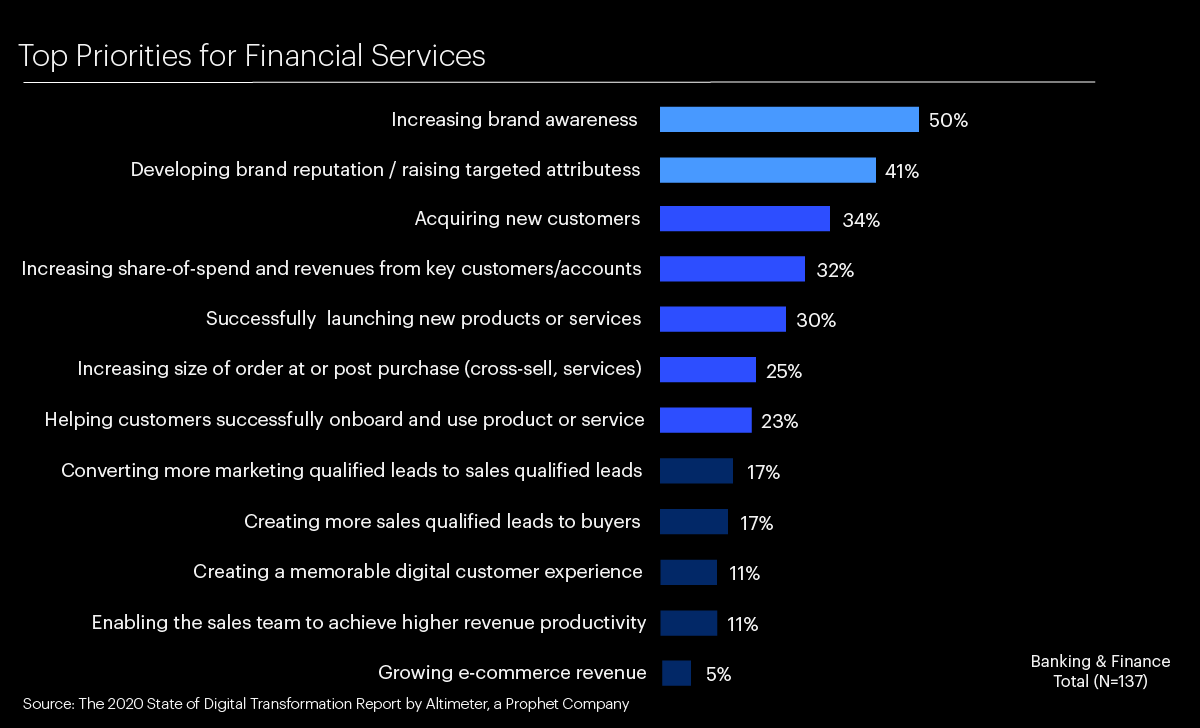

Top Digital Transformation Challenges in Financial Services

Collaboration and personalization can help legacy firms outpace fintech upstarts.

When it comes to digital engagement, some of the biggest names in financial services still can’t seem to move fast enough.

While upstart brands like Cash App, Alipay, Monzo and Robinhood rack up millions of new customers, many legacy financial services companies are plodding along. There is progress, but many digital transformation initiatives are underperforming.

“Many digital transformation initiatives are underperforming.”

There’s no question that companies like Capital One and USAA are breaking new ground. But despite increased spending, many others are lagging behind – both in how they think about digital transformation strategy and how they execute it.

At Prophet, we wanted a better sense of what’s holding these companies back and how financial services compared to other industries. Our digital transformation research dug into the details of transformation, surveying 476 digital executives worldwide, including 150 who work in financial services.

One major finding? If efforts are uneven, it’s not necessarily because they’re underfunded. Digital marketing budgets in financial services now comprise between 50 and 70 percent of marketing resources. That’s up from a range of 20 to 40 percent in 2018. And while COVID-19 is causing some firms to cut spending as part of overall cost reductions, most execs recognize the need for more digital marketing in an increasingly virtual world.

Financial services firms still focus on traditional marketing objectives, like increasing brand awareness or developing brand reputation. Those goals matter. But it often means that they pay less attention to higher-impact digital targets, such as adding customers (which ranks as the first priority across all industries) and increasing revenues from key customers and accounts (ranks as the second priority). And they lag even further behind financial disruptors, which use marketing to generate leads.

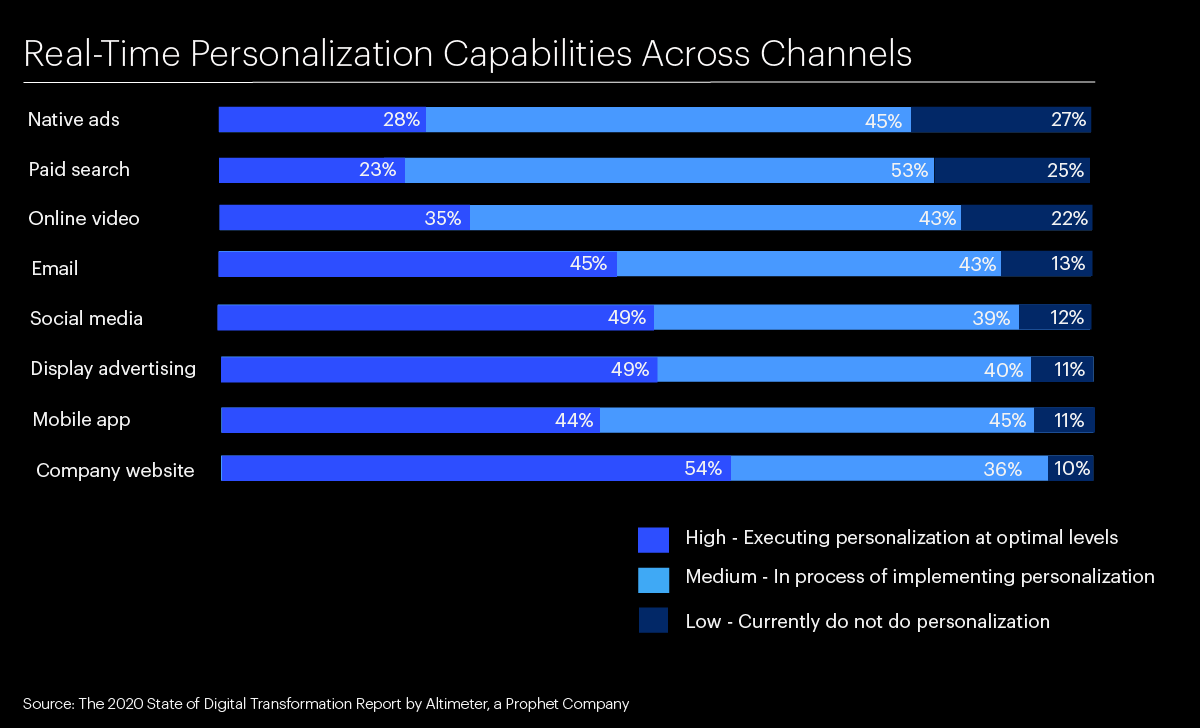

2. Gaps in Personalization

While almost half of the financial services respondents rank personalization as a top priority, the industry is lagging in delivering those experiences, something that is considered table stakes in other industries. While dynamic personalization is a key characteristic of digitally mature enterprises, less than half of financial services believe they can personalize at optimal levels. And 16 percent of firms don’t personalize at all across channels. There’s also a worrisome level of false confidence. Almost half do not use marketing technology (martech) platforms to scale personalization efforts, despite the general consensus that martech is needed to deliver optimal levels of personalization.

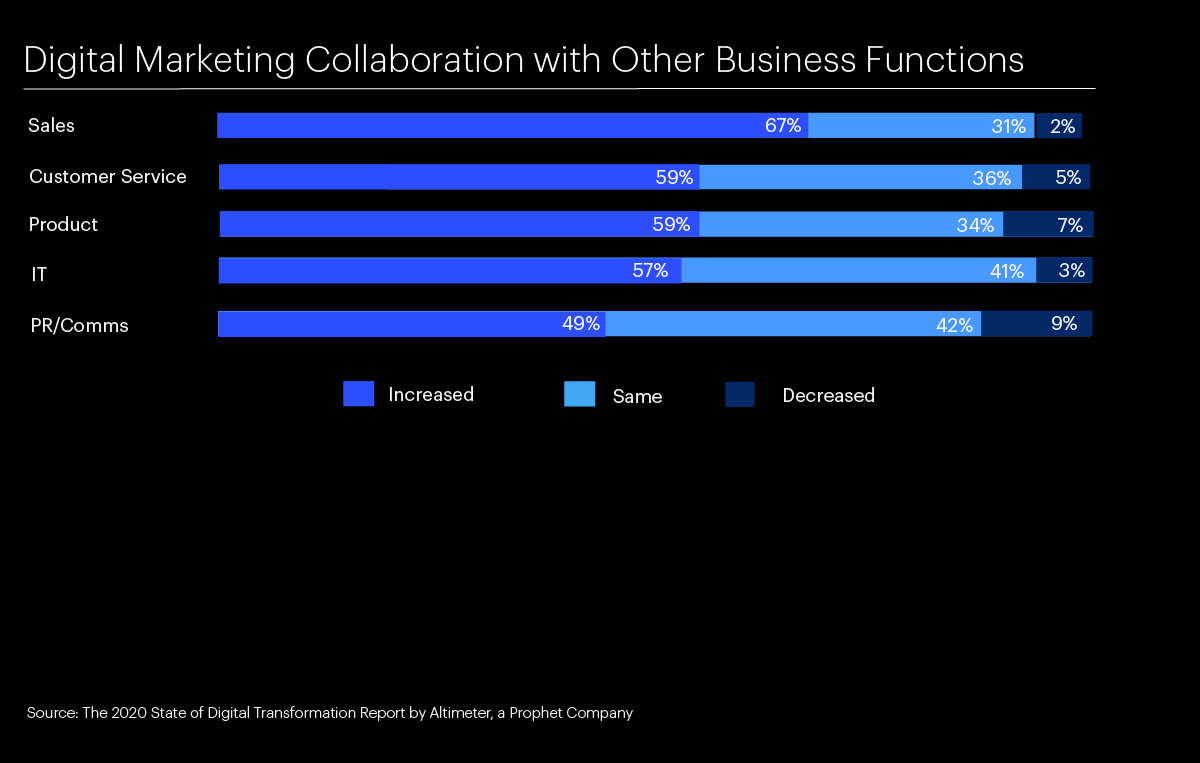

3. Lagging in Collaboration

Certainly, marketing teams at financial services companies understand that it’s essential to work closely with other business functions, especially sales. They know they need to continue to prioritize this cross-functional collaboration. In the context of demand generation and B2B2C marketing, this increased collaboration is crucial to ensuring a lead doesn’t get dropped and is ultimately converted. About three-quarters of financial services respondents plan to invest in cross-functional efforts going forward, indicating that plans are taking this collaboration need into account. While the mindset and plans for the future are good news, it’s still worth noting these efforts lag in practice. About two-thirds of respondents increased collaboration with sales over the last two years, compared with 75 percent of respondents in all industries. Almost a third of respondents actually cut back on collaboration.

The Underlying Challenges: Integration Struggles and Skill Shortages

There are two underlying areas to address that are critical to solving the above problems. First, financial services still struggle to integrate the technology they already have. Almost half of all financial services firms say they lack the budget and integration mechanisms for their technology, specifically the martech stack.

And second, finding and hiring the right talent is still difficult. More technical skills are central to digital marketing talent needs, especially data analysis, marketing automation and software expertise.

As financial services firms look to improve and accelerate their transformation efforts, here are five ways to increase the pace of change:

Use digital marketing to drive growth through generating leads and acquiring more customers, rather than simply building brand awareness. Integrate a marketing technology stack that enables personalization. Prioritize cross-functional collaboration between marketing and other departments, especially sales, for the greatest business impact. Focus on integrating martech into the existing technology stack by ensuring adequate budget and resourcing is in place. Develop recruiting strategies and revamped employee value propositions to fill talent gaps, especially in the ability to make existing martech solutions work better.

Is your business equipped to compete? Our expert Financial Services practice can help to devise a clear strategy to move your business forward in 2021 and beyond, get in touch today.

Busting the Myth That B2B Companies Are Digital Laggards

We examined 26 criteria, and find B2B companies are holding their own.

New research shows B2B companies are on par with their B2C counterparts and should look to B2B digital leaders for best practices.

The online world is full of warnings that B2B companies have fallen behind B2C companies when it comes to digital transformation. However, our new report, The 2020 State of Digital Transformation in B2B, clearly shows that B2B companies are on par with their B2C counterparts across five stages of digital maturity. This work is based on a comparison of 170 B2B companies with 238 B2C organizations and 160 B2B2C firms based on a survey conducted by the industry analysts at Altimeter, a Prophet company.

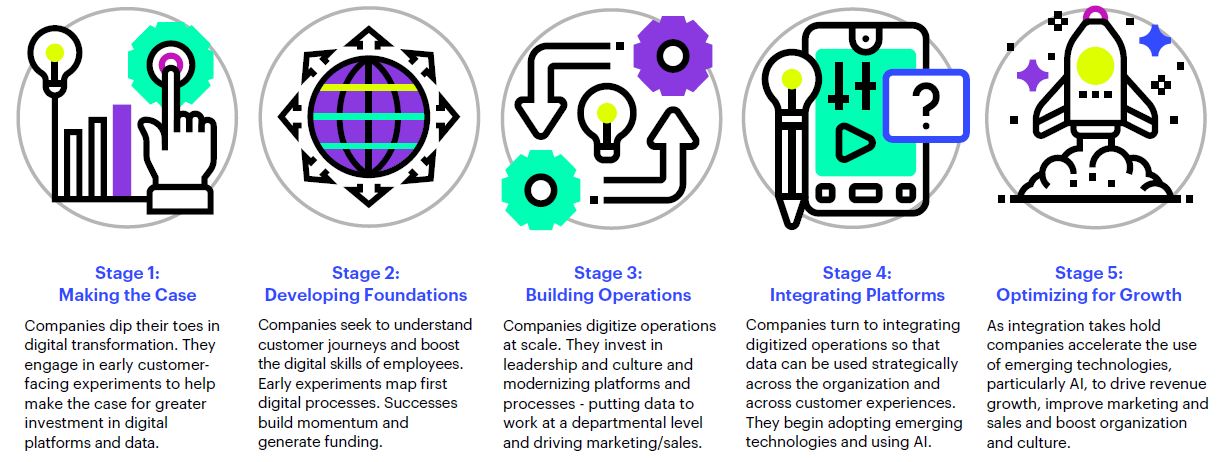

Five Stages of Digital Maturity

Digital maturity was determined by evaluating the relative adoption of digital practices across twenty-six criteria grouped into five areas: Leadership and culture, customer experience, marketing and sales, technology and innovation, and data and artificial intelligence. To understand the impact of digital transformation maturity, we grouped all of the respondents into one of five transformation stages based on their maturity scores (see Figure 1). Click here to see a deeper exploration of digital maturity in the full report.

Figure 1: The 5 Stages of Digital Maturity

Sixty-nine percent of all companies (B2B, B2C and B2B2C) have moved past the initial stages of digital transformation maturity and are investing in digital technology and data to accelerate growth and improve productivity. Two-thirds of these more mature companies are in stage three where they are focused on operationalizing the use of platforms and data at scale and putting them to work to drive growth. The most mature companies, 25 percent of total respondents in stages four and five, are characterized by efforts in integrating operations to deliver more personalized experiences and using emerging technologies such as AI to redesign customer experiences and offer digital services to accelerate growth. Time is running out for the laggards in steps one and two while those companies in stage three must turn their efforts into impact so they can justify their investment and continue to accelerate progress.

Digital Maturity is a Better Predictor of Capabilities and Plans Than Customer Type

Our study revealed that stages of digital maturity are better predictors of digital capability building, investment in technologies or utilization of advanced digital platforms and data. Differences between B2B and B2C companies on a broad range of digital transformation plans and practices become small once responses are controlled for the level of digital maturity.

“The most mature is taking a more opportunistic approach compared to those who are still struggling to put in place basic digital capabilities.”

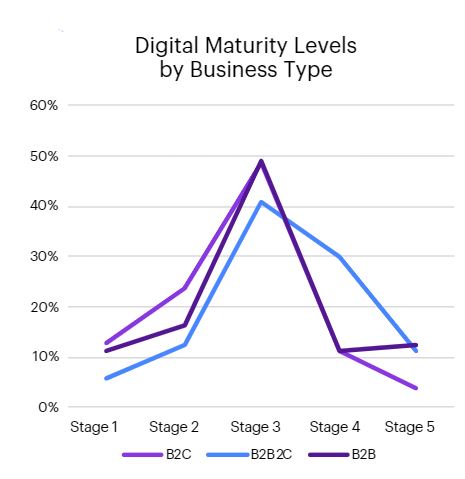

B2B2C companies are more likely to be more digitally mature (41% in stages 4 and 5) than either B2B or B2C companies; probably because they must build capabilities to address both business and consumer audiences.

Figure 2: Digital Maturity Levels by Business Type

Digital Maturity Matters

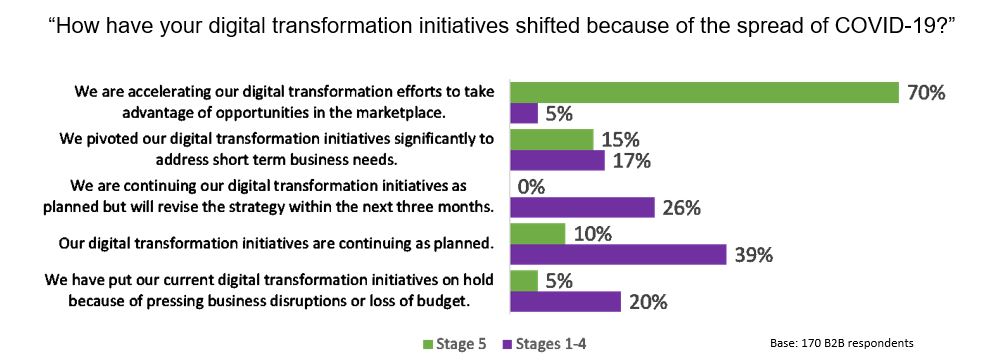

Organizations that are furthest down the path of digital transformation are best able to turn uncertainty into a competitive advantage. Their response to the pandemic is illustrative. The most mature are taking a more opportunistic approach compared to those who are still struggling to put in place basic digital capabilities. While eighty-two percent of stage one through four organizations are continuing or pivoting their transformation efforts, seventy percent of the most digitally mature companies are accelerating their digital transformation efforts (see Figure 3). They recognize that disruption is a time to step forward not back and have the confidence in their digital capabilities to capitalize on the situation.

Figure 3: Transformation Initiative Shifts Due to COVID-19

B2B companies should shift their search for best practices from B2C companies to more digitally mature B2B companies. It is easier and more effective to replicate best practices from one B2B company to another and maturity is a better predictor of outcomes than customer type. B2B companies who are digital laggards (stages 1 and 2) should look to the examples of companies that are operationalizing and scaling their digital efforts (stage 3). B2B companies can look to their more mature counterparts for insights into how to integrate, personalize and used advanced technologies to drive impact and become more digitally mature.

Brands Are Sitting Out the Super Bowl: Is This an Inflection Point for Marketers?

How companies are recalculating the complex math of advertising during the Big Game. It’s riskier than ever.

The Super Bowl LV is right around the corner. The Kansas City Chiefs will face the Tampa Bay Buccaneers and this year’s match-up is all about legacy vs. new. The duel of Tom Brady vs. Patrick Mahomes. Will Tom Brady be able to win another Super Bowl and retain his GOAT status? Or will the 25-year-old star outperform him on a national stage? It will be a fascinating game to watch.

Off the field, we also see the duel of legacy vs. new as we look at the much-ballyhooed ad spots surrounding the Super Bowl. Several legacy brands that traditionally bought ad spots are sitting out this year: Budweiser, Pepsi, Coke. While other brands like Chipotle, DoorDash and Indeed are willing to get in the game and spend $5M+ for 30 seconds of airtime. Even amidst the criticism against the NFL for their lackluster response to Black Lives Matter, the controversy of physical audiences during the pandemic and viewership ratings once again on the decline, the Super Bowl is still considered the quintessential placement for U.S. advertisers.

“The Super Bowl is still considered the quintessential placement for U.S. advertisers.”

In addition to navigating these ongoing challenges, this year’s Super Bowl also brings the duel of advertising on legacy television vs. digital video to a head. Brands are increasingly aware that coveted eyeballs are turning off the television while the reach and engagement on YouTube, Twitch and other digital platforms are becoming the new prestige play. CMOs today are seeing digital video advertising deliver results and brand awareness is also functioning as a direct response.

We believe this interesting match-up of legacy vs. new highlights 3 shifts in how CMOs decide where and how they invest their marketing dollars:

1. From Static to Dynamic

CMOs are increasingly under pressure to move the needle and do it fast. Their mandate has expanded from the top of the funnel down to acquiring customers. As a result, they are continuously experimenting with ways and channels to optimize the return of their marketing investment – often challenging practices that have been considered “tried and true.” For the first time in decades, Anheuser-Busch announced that the iconic Budweiser brand is sitting this Super Bowl out. We can still expect to see ads from BudLight and the first-ever corporate spot. Regardless, this still came as a big surprise to many.

2. From Reach to Relevance

The pandemic has shifted consumer behavior. Consumers have become more open to trying new brands – even new players – forcing brands to defend their positions. As a result, CMOs are changing their approach from maximizing reach to proactively finding ways to embed their brands in consumers’ lives. This year, for some consumers, the Super Bowl will not be as important as in prior years, given social distancing. Budweiser understands this and is reportedly reallocating its Super Bowl budget to a topic that is more relevant to its audience: COVID relief in the form of coronavirus vaccination awareness efforts.

3. From Opportunistic to Authentic

Shifting marketing strategy and execution depending on context or market conditions is not new. The best marketers have done it to raise the bar and set the standard on how to engage consumers (remember the “dunk in the dark” tweet from Oreo in 2013?). Today this is increasingly difficult as consumers expect and demand brands to be authentic. Consumers are quick to call out anything that looks and feels different or “off-brand.” With the ease and speed of social media, brands have to answer to their customers. It will be interesting to track how Budweiser executes on the COVID-19 efforts now and into the future from an authenticity perspective, at the risk of exposing the brand and hindering the return of their investments.

Investing in a Super Bowl ad is a big decision for any marketer. Sometimes the decision is clear and compelling: by showing up to where consumers are, on the right platforms, in the right context and with authentic engagement, marketers have a better shot at maximizing the return of their investments.

But the case is not always clear and yet organizations continue to invest. Why? The culture within organizations is slow to change. Successful marketers go beyond the data to focus on aligning the mindsets and behaviors of their organizations to ensure they make the right decisions, not the decisions that have “worked” in the past. It’s a tall order.