Meet Jamie, the insurance customer of 2030. What will it take to win her business?

The Insurance Customer of the Future report is the latest research from Prophet’s Financial Services practice. It explains how insurers can drive growth by putting their customers at the center of their transformation strategies. The first step? Understanding their customers on a deeper level. Not only understanding who they are, what they value and what they need in the present, but also several years down the line.

Prophet’s experts centered their research around Jamie, an insurance customer living in 2030. By understanding and anticipating the generational trends and technological possibilities that will shape Jamie’s environment, insurers can make the right transformation moves now to win Jamie’s – and her peers – business in the future.

Read this report to gain deeper insights on:

The digital transformation trajectory of the insurance industry and its implications for business leaders

The broad demographic, social, economic and technology trends that will define the decade ahead for insurers and their customers

The evolving consumer demands that will shape the future of insurance

The ways insurers need to transform their businesses to win in the “new world”

The insurance game is changing. The past year has seen life completely upended for insurance agents, whose success once hinged on a certain skillset, often with physical touchpoints. While many insurance providers have raced to increase digital selling efforts in reaction to COVID-19, the results have been mixed. It’s going to keep changing too, so it’s time to adapt to fuel a post-pandemic recovery and lead the way to future growth.

Embracing Digital Selling from our dedicated Financial Services practice outlines a roadmap for digital selling with the steps to take now in order to create a strategy that supports new digital tools, efficient models and the development of the necessary capabilities.

In this report you will learn:

The four primary challenges insurers need to overcome to compete in the digital world

How insurers can maximize digital selling efforts for both short and long term growth

A roadmap to guide how to install a structure that helps agents navigate a fast-changing, digital selling environment

Top Digital Transformation Challenges in Financial Services

Collaboration and personalization can help legacy firms outpace fintech upstarts.

When it comes to digital engagement, some of the biggest names in financial services still can’t seem to move fast enough.

While upstart brands like Cash App, Alipay, Monzo and Robinhood rack up millions of new customers, many legacy financial services companies are plodding along. There is progress, but many digital transformation initiatives are underperforming.

“Many digital transformation initiatives are underperforming.”

There’s no question that companies like Capital One and USAA are breaking new ground. But despite increased spending, many others are lagging behind – both in how they think about digital transformation strategy and how they execute it.

At Prophet, we wanted a better sense of what’s holding these companies back and how financial services compared to other industries. Our digital transformation research dug into the details of transformation, surveying 476 digital executives worldwide, including 150 who work in financial services.

One major finding? If efforts are uneven, it’s not necessarily because they’re underfunded. Digital marketing budgets in financial services now comprise between 50 and 70 percent of marketing resources. That’s up from a range of 20 to 40 percent in 2018. And while COVID-19 is causing some firms to cut spending as part of overall cost reductions, most execs recognize the need for more digital marketing in an increasingly virtual world.

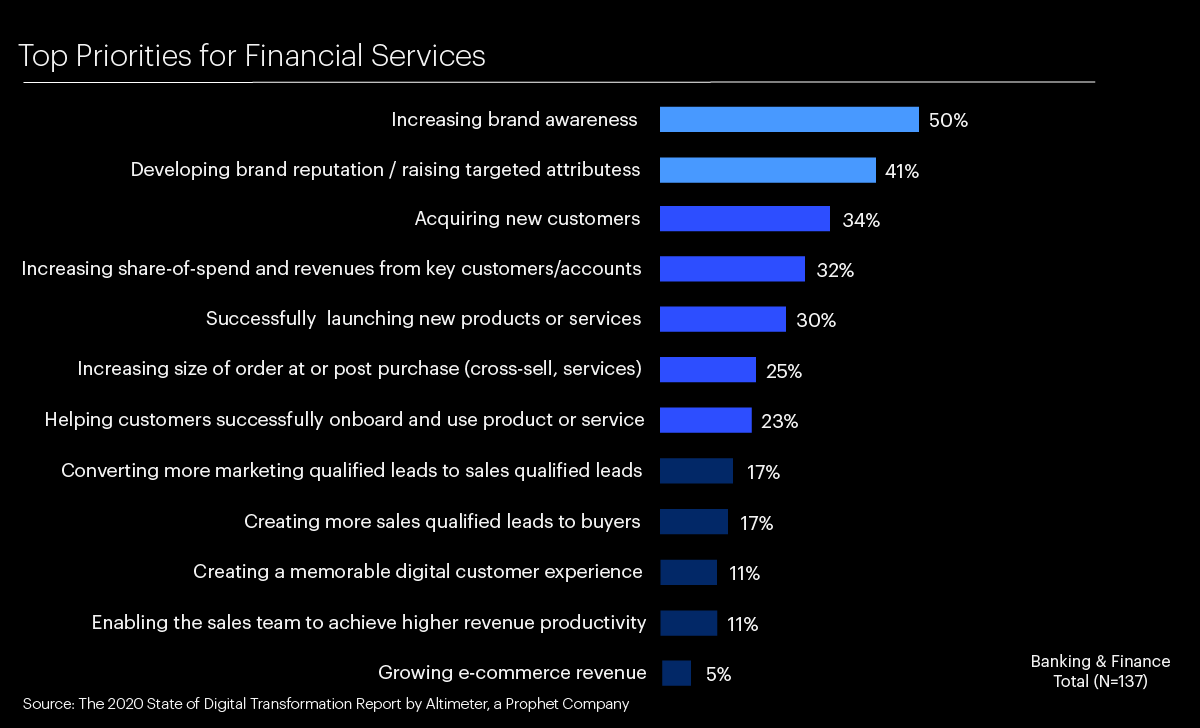

Financial services firms still focus on traditional marketing objectives, like increasing brand awareness or developing brand reputation. Those goals matter. But it often means that they pay less attention to higher-impact digital targets, such as adding customers (which ranks as the first priority across all industries) and increasing revenues from key customers and accounts (ranks as the second priority). And they lag even further behind financial disruptors, which use marketing to generate leads.

2. Gaps in Personalization

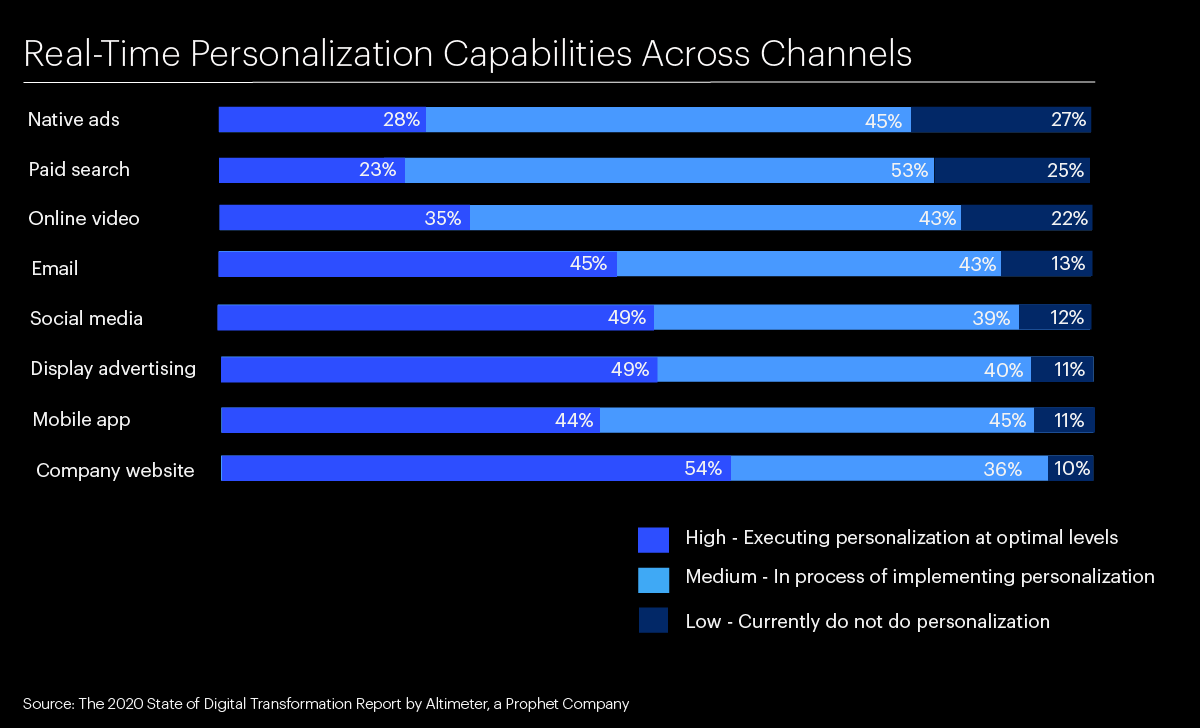

While almost half of the financial services respondents rank personalization as a top priority, the industry is lagging in delivering those experiences, something that is considered table stakes in other industries. While dynamic personalization is a key characteristic of digitally mature enterprises, less than half of financial services believe they can personalize at optimal levels. And 16 percent of firms don’t personalize at all across channels. There’s also a worrisome level of false confidence. Almost half do not use marketing technology (martech) platforms to scale personalization efforts, despite the general consensus that martech is needed to deliver optimal levels of personalization.

3. Lagging in Collaboration

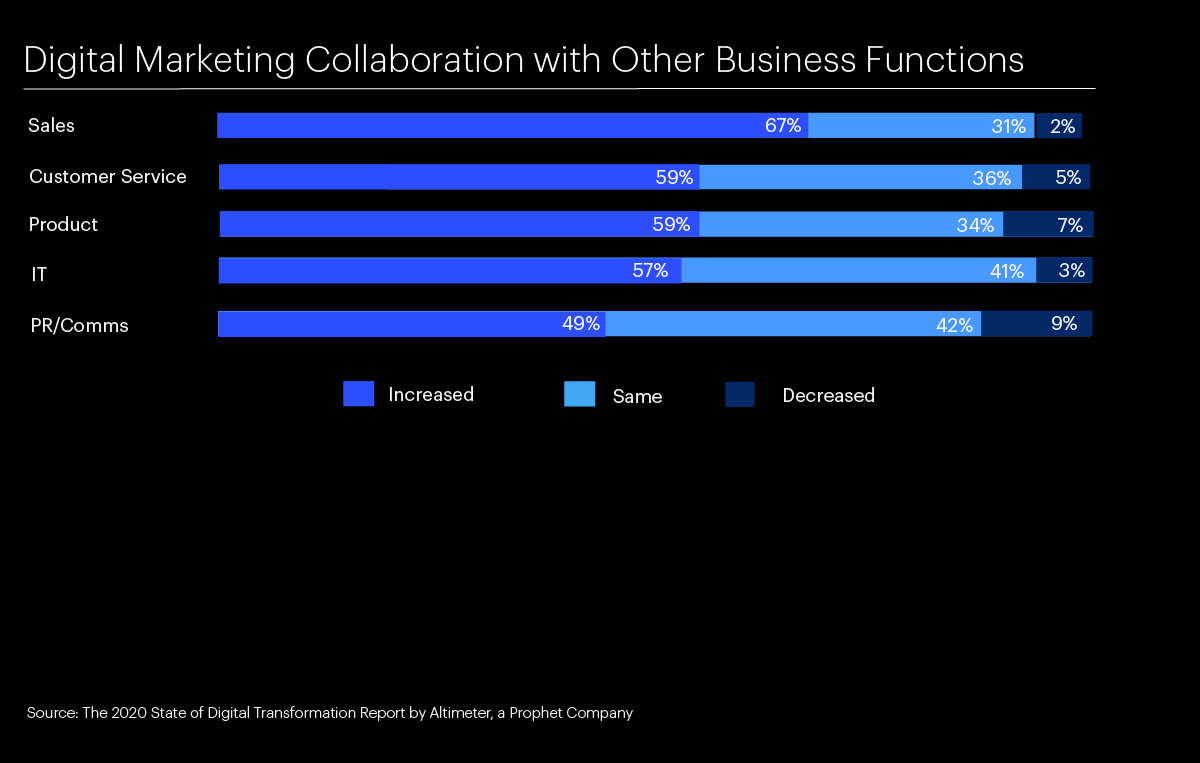

Certainly, marketing teams at financial services companies understand that it’s essential to work closely with other business functions, especially sales. They know they need to continue to prioritize this cross-functional collaboration. In the context of demand generation and B2B2C marketing, this increased collaboration is crucial to ensuring a lead doesn’t get dropped and is ultimately converted. About three-quarters of financial services respondents plan to invest in cross-functional efforts going forward, indicating that plans are taking this collaboration need into account. While the mindset and plans for the future are good news, it’s still worth noting these efforts lag in practice. About two-thirds of respondents increased collaboration with sales over the last two years, compared with 75 percent of respondents in all industries. Almost a third of respondents actually cut back on collaboration.

The Underlying Challenges: Integration Struggles and Skill Shortages

There are two underlying areas to address that are critical to solving the above problems. First, financial services still struggle to integrate the technology they already have. Almost half of all financial services firms say they lack the budget and integration mechanisms for their technology, specifically the martech stack.

And second, finding and hiring the right talent is still difficult. More technical skills are central to digital marketing talent needs, especially data analysis, marketing automation and software expertise.

As financial services firms look to improve and accelerate their transformation efforts, here are five ways to increase the pace of change:

Use digital marketing to drive growth through generating leads and acquiring more customers, rather than simply building brand awareness. Integrate a marketing technology stack that enables personalization. Prioritize cross-functional collaboration between marketing and other departments, especially sales, for the greatest business impact. Focus on integrating martech into the existing technology stack by ensuring adequate budget and resourcing is in place. Develop recruiting strategies and revamped employee value propositions to fill talent gaps, especially in the ability to make existing martech solutions work better.

Is your business equipped to compete? Our expert Financial Services practice can help to devise a clear strategy to move your business forward in 2021 and beyond, get in touch today.

Head of Digital at MB Bank Discusses Fueling Growth Through Digital Transformation

Becoming a truly digital-first organization requires a fundamental change in how companies do business.

In today’s corporate world, is there a more highly sought-after term than “digital transformation”? Probably not. COVID-19 is acting as a catalyst in accelerating many organizations’ digital transformation agendas. New technologies and business models are putting many existing players at risk with disruptive forces. Becoming a truly digital-first organization requires a fundamental change in how business is done. Corporate leaders understand the criticality of digital transformation, however, many are struggling with how to advance it.

We had the pleasure to interview Mr. Vu Thanh Trung, Head of Digital Banking at MB Bank. MB Bank (Military Commercial Joint Stock Bank) is one of the largest financial services groups in Vietnam. Over the past few years, MB Bank initiated a multi-year transformation program to become a digital-first bank. As part of the transformation, Prophet worked with MB Bank on customer expansion strategies and helped to pave the way to a more modern, digital and customer-centric bank. In this interview, Mr. Trung provides valuable insights on how to transform and what it takes to be a digital organization today.

What drove MB Bank to embark on a digital transformation agenda?

The banking industry in Vietnam is a nascent market with considerable room for growth. With a wide penetration of the Internet and smartphones and a growing digital-savvy population, Vietnamese consumers are rapidly shifting towards digital and mobile banking. They desire more seamless digital banking services with a more personalized customer experience. To meet the increasingly demanding expectations of customers in the region, MB Bank needed to fully embrace digital transformation to capitalize on the boom of digital adoption.

What has MB Bank done so far to digitally transform?

We started the digital transformation from scratch almost four years ago. A new digital bank was set up as an independent business unit at the end of 2017 with our own balance sheet, separate from the legacy bank. Our digital transformation efforts focus on two fronts: externally, we want to better understand the marketplace and the customer needs; internally, we want to introduce collaborative and nimble ways of working across divisions.

Prophet has been our indispensable partner on this multi-year strategic growth and digital transformation journey to become more customer-centric and more innovative. We started with an in-depth segmentation of our customer needs, behaviors and attitudes. Then we mapped out a roadmap with clear growth moves focused on innovating and transforming our digital offers. An important part of our digital transformation is to instill more agility and cross-organization collaboration. Prophet showed us how to innovate faster, pilot and launch quicker. We were able to revamp the digital banking app within three months, which normally would take 12-18 months.

Lastly, I want to talk about the achievement we have made on the people front so far. We started with a team 100 percent from the legacy bank and then recruited external technical expertise to fill the functional gaps. We now have a well-balanced commercial and technical team (some 400 in-house engineers) and work more cohesively in a start-up-like environment to drive towards our digital transformation ambitions.

What are the priorities for your digital transformation?

Among all things, we focus on our PEOPLE first. Digital transformation is not about technologies, but rather about changing the mindset of our people – our organizational culture and processes. Hence, we think people should be the ones to drive the technology and not the other way around.

As I mentioned, we started off with a team 100 percent from the legacy bank. We want to create a more entrepreneurial environment where people are empowered to make a difference to MB Bank in a more cohesive and dynamic way. This is rather different from the culture of our legacy bank. So, we need to train our people with new skills and more importantly, shift their mindset towards a digital culture while building up our technological capabilities.

“Digital transformation is not about technologies, but rather about changing the mindset of our people – our organizational culture and processes”

Prophet helped us to implement a nimbler way of working to get closer to the customers and shorten the time to market. We set a shared purpose and vision to help our people to be more personally and emotionally invested. We broke down the silo way of working and replaced it with a collaborative approach. With this new way of working, we managed to revamp the digital banking app at least four times faster.

The results so far have exceeded our expectations. In the midst of the pandemic last year, we launched our new digital banking app, which became the No. 1 app in Vietnam surpassing even Facebook and TikTok. Within nine months of the launch of the new app, we had 1.8 million new customers. A feat we are very proud of given the harsh pandemic landscape and lockdowns.

What advice would you give to leaders looking to drive transformation and ensure the organization has what it needs to succeed?

Leadership is an absolute requirement for any successful digital transformation. It’s not only about setting the vision, defining the strategies and building C-suite commitment. Leaders must “walk the talk” to establish a digital culture so that everyone is on board.

The success of digital transformation must be paired with a comprehensive talent strategy that sets your people up for success. In order to do so, we aligned incentives with staff performance to drive target reaching, providing tools and opportunities for upskilling and collaboration to help employees reach their goals.

Why do you think cultivating an innovative culture is important in a digital transformation program?

To me, digital transformation marks a reimagination of how an organization uses its technology, people and process to fundamentally change how we run the business. Digital transformation doesn’t come in a box. It provides the guidelines to steer people’s behaviors that advance our company’s goals.

A lot of organizations fail in digital transformation by ignoring the importance of culture. For MB Bank, we instilled an innovative culture through new ways of working. The agile way of working spurs our innovation process through cross-functional collaboration—allowing our people to take risks, fail fast and learn.

What are the challenges you have faced in your digital transformation journey?

We are still at the early stage of our journey. We need to continuously work on integrating technology seamlessly into every aspect of our organization to unlock the full potential of digital transformation. We need to reboot the parts of our operating model that pose hurdles for more cross-functional collaboration and operational efficiency. Then there is the holy grail of data — we are reorganizing our customer data as it is currently scattered across different legacy systems. We are in the process of integrating and synthesizing this data more effectively so that they can provide more meaningful, actionable insights for business units.

So, what are your next steps?

We are rebooting our operating model into a more unified structure and working to enhance collaboration across all business units. We need to further instill the innovative culture to fully tap into every individual’s potential and reap the benefits of agile methodology. And finally cracking the data issue across different systems so we can design more products and services to better serve our customers. We are really glad to have Prophet be our partner on this journey, helping us transform and steering us to become the leading digital bank of the future.

While insurance companies have made much progress in reinventing themselves for today’s customers, the results are clear: there’s still some way to go. As many turn their attention toward planning and formulating their strategies for the year ahead, this playbook from our Financial Services practice outlines the different levers to pull in order to speed up digital transformation efforts and customer experience initiatives.

In this playbook you will learn:

How insurers can transform their organizations from the inside out by effecting culture change and equipping the business with the right talent and capabilities to succeed in 2021.

How a customer-centric approach can help your business, how to get started and how to measure you efforts.

What the state of transformation is in the industry today and the reasons to hit the gas now.

How to Effect Culture Change in Financial Services

By dialing up agility, empathy, inclusivity and curiosity, companies can inspire effective transformation.

Financial services companies have been pursuing transformation for years, but the events of 2020 have only underscored the need for these firms to rapidly evolve. In a few months, the world has achieved years of digital progress, shining an unflattering light on the many companies that lag. Many legacy financial services organizations, hierarchical and slow-moving, stand to lose as much as 35% of banking revenues to more tech-savvy rivals. That’s on top of an estimated $1 trillion in losses the sector may give up as a result of COVID-19.

Legacy companies are difficult to change by design. They were built for capital longevity and regulatory compliance, not agility and innovation. But they can’t afford to stand still. The ones that are making the most progress are moving forward at two speeds. First, they’re executing multiple plans at lightning pace to get teams and market positions back to “normal.”

Here we dive deeper into each of these pathways with some industry examples:

Defining the Transformation: Driving Clarity

This step establishes a unifying ambition that is powerful and actionable, and that appeals to all levels of leadership.

We recently ran research with hundreds of leaders to study the cultural levers of transformation, including 100+ from financial services companies, who were more likely than average to say that their initial transformational efforts are proving effective.

But there are still roadblocks. Financial services companies often stumble when developing a transformation mission that is clear and actionable throughout the organization. It’s essential for leaders to get key stakeholders throughout the enterprise on board with the transformation plan in order for it to succeed.

Capital One, for example, has achieved extraordinary success by committing to a clear technology mandate. With a rallying cry of ingenuity, simplicity and humanity, the mission makes as much sense to thousands of software engineers and cloud executives as it does to customer-service representatives. Not only does Capital One excel among its peers, but its recruiting clout is on par with the best tech firms.

Directing the Transformation: Adapting the Operating Model

Financial companies, with their complex hierarchies and sprawling brand portfolios, often find that changing their operating model to support these ambitions is daunting. It involves overhauling governance, processes, roles, systems and tools. But these changes are essential: All parts of the organization need to line up with this leaner, faster thinking.

“Many legacy financial services organizations, hierarchical and slow-moving, stand to lose as much as 35% of banking revenues to more tech-savvy rivals.”

American Express offers an example of successfully directing the transformation. When it decided to shift its operating model away from relying on merchant fees to increasing card use, it re-engineered itself so that all functions could support the company’s new goals. That means decisions can be made quickly and laterally, without hierarchical delays.

But others struggle, in part because once a plan is prepared, executives are reluctant to share those roadmaps throughout the business. Our research finds that financial services companies tend to restrict these blueprints to the C-Suite – only 34% make it visible to the broader organization. That guarded attitude impedes financial-services companies from successfully adapting their operating models. Everyone needs to know where the company is headed in order to direct the transformation

Financial-services companies do have some advantages, though. Compared to other industries, they are more likely to update their roadmaps often, with 42% evaluating progress on a weekly basis compared to 31% in other industries. They’re also better at developing key performance indicators – 78% believe KPIs were well executed and measured transformation progress well.

Enabling the Transformation: Building a New Talent Model

None of these changes can take hold if the right people with the right skills aren’t in place. That requires shaking up methods of finding new talent and developing skills and competencies among current employees.

This includes hiring a diverse workforce and learning to listen to what they say. Leaders “who are inherently inclusive and collaborative and encourage good ideas to surface from wherever” are critical, says Mary Ann Villanueva, head of brand culture and engagement at Citi.

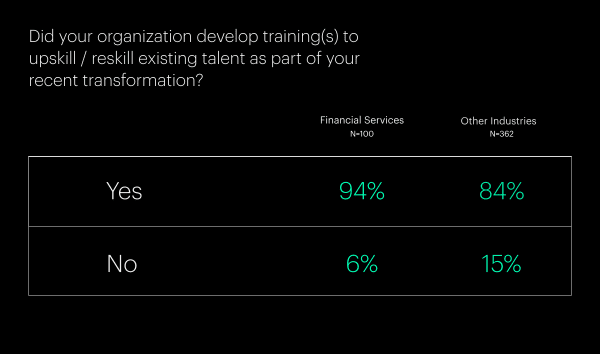

Our research finds that financial services companies are somewhat more willing to train and upskill employees than other sectors. One recent home run comes from JP Morgan’s $11 billion annual investment in tech, including an army of 50,000 technologists. That powered it to record results before the pandemic and continues to fuel the company’s exceptionally resilient performance so far this year.

Motivating the Transformation: Inspiring the Change

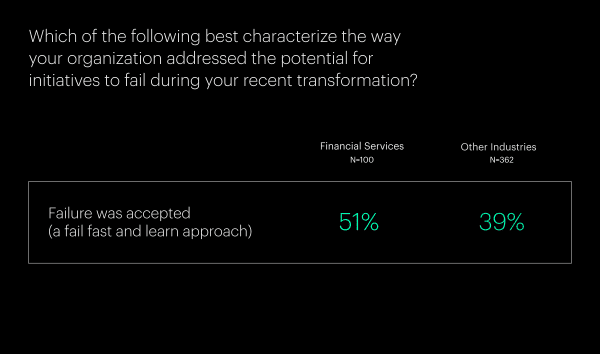

This aspect of change requires leaders throughout the organization to bring the transformation plan to life. In companies that are successfully transforming, executives don’t just talk about change – they exemplify it in ways that inspire employees to become evangelists for the new ways of working. Above all, they cultivate a tolerance for failure. Missteps are inevitable and failure is where an organization often finds opportunity. When teams fear failure, they seek broad consensus, which slows decision-making.

“We’re trying to enable employees to fail on small things, such as experiments in the innovation lab, to achieve success on the big targets,” Trung Vu Thanh, head of digital banking for MB Bank Vietnam, tells our research team. “We’re trying to push to the limit and use innovation, as more ideas will help.”

It’s hard to find a better example than USAA in this realm. USAA is best known for its intense focus on families and pride in military service. But its commitment to customer-centricity is so deeply ingrained into the test-and-learn culture that employees submit more than 10,000 customer-experience improvement ideas each year. Almost 900 are so good they’re patented. (And 25 of them came from a security guard, who – like all employees – is also a customer.) It’s an organization that draws its strength and energy from trying to find new ways to excel.

Taken together, these four pathways – harnessing curiosity, agility, inclusivity and empathy – can help financial services companies navigate their transformation. They build deep cross-functional engagement and collaboration. When combined with a shared sense of purpose, they can follow the transformative path to uncommon growth.

If you want to learn more about how our expert team can help your company accelerate change by transforming from the inside out then contact us today.

Digital Transformation for Financial Services: Three Reasons to Hit the Gas

Legacy companies are moving faster, keeping up with their fintech competitors.

While the financial services industry is undergoing almost constant transformation, fintech startups drive most of it. As these rising stars continuously find new ways to introduce customer-centric innovation, incumbent financial institutions are struggling to keep up. “The 2020 State of Digital Transformation,” a new report from Altimeter, a Prophet company, finds that even as these tech-savvy newcomers surge to record valuations, 68% of traditional financial services companies report that they are only in the early stages of digital transformation. And they say that COVID-19 has slowed their progress even further.

While validating the obstacles many legacy companies face as they navigate their way forward, this research makes clear that this is no time to slow down. The sooner companies lean in and accelerate digital efforts, the more revenue and market share they can reclaim from newcomers.

Fending off the fintech onslaught

There’s no doubt that capital markets are favoring these fintech startups. In 2019, KPMG reports that investment hit $135 billion. These companies are growing in scale and revenue, with 68 achieving “unicorns” status, a valuation of at least $1 billion, as of this past September, according to CB Insights. And while they span consumer banking, payment solutions, insurance technology and trading, they have plenty in common: They’re disruptive, customer-centric and digital to their core.

Chime, a neobank startup offering digital cash management services and debit cards, is one of our favorite examples. It has tripled its transaction volume and revenue this year, achieving a $14.5 billion valuation.

“The sooner companies lean in and accelerate digital efforts, the more revenue and market share they can reclaim from newcomers.”

And Robinhood, a commission-free brokerage platform, saw daily average trades skyrocket to 4.3 million in June, surpassing all traditional brokerage firms. Among the household names left in the dust: TD Ameritrade, with 3.84 million, Charles Schwab at 1.8 million and E-Trade at 1.1 million.

But some traditional banking institutions, such as Marcus, Goldman Sachs’ consumer banking platform, have also seen rapid growth during the pandemic. It’s grown to more than $27 billion in savings from 500,000 customers, indicating that even legacy companies can successfully transform into digitally-powered institutions.

How legacy companies can catch up on digital transformation for financial services

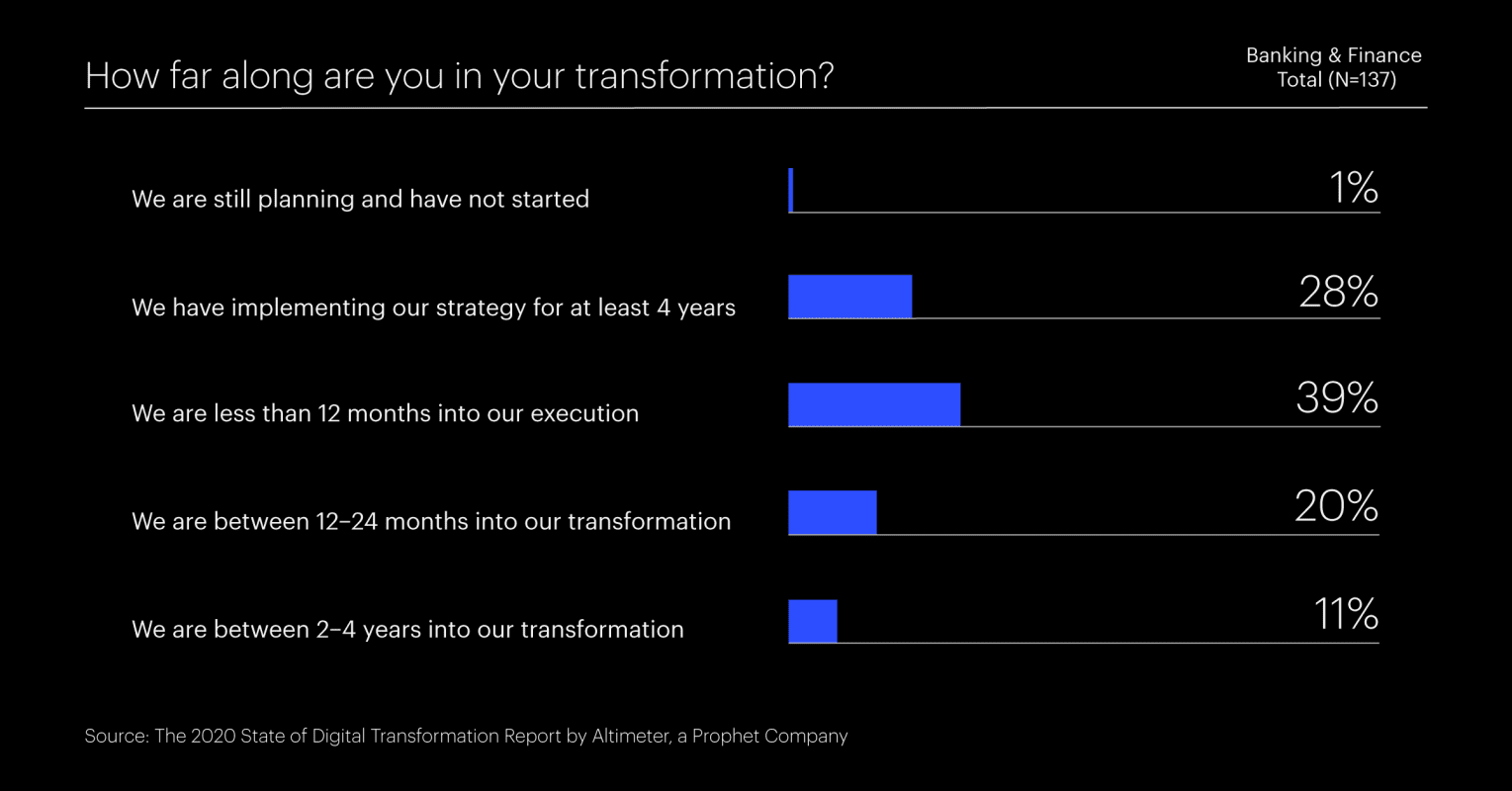

Altimeter’s report delves into how incumbents are trying to catch up. Based on an in-depth survey of 600 executives, including 137 in financial services, three clear imperatives emerge.

1) Move faster. The majority of financial services firms are still early in their digital transformation journey.

Altimeter’s research measures digital transformation through a five-stage model. First, companies make their case for investing in digital. Next, they develop foundations for more comprehensive investment, seeking to understand customer journeys and improve employees’ digital skills. From there, they build operations, digitizing them at scale. Fourth, they integrate these platforms to use data more strategically, and finally, optimize for growth, leveraging data and AI for great customer experiences.

Only 25% of the companies in our study have moved beyond this to the final two phases. Financial-services execs say they are moving even more slowly. Some 68% say their companies are still in the first two years of their transformation journey, and only 38% say they’ve reached the third phase (building operations). That compares to more than 50% of healthcare, tech and retail companies.

And that’s far too slow for consumers. The latest banking satisfaction research from J.D. Power, for example, shows that the more digital the customer, the more significant the satisfaction gap. And dissatisfaction is highest among Gen Z customers, a fast-growing demographic.

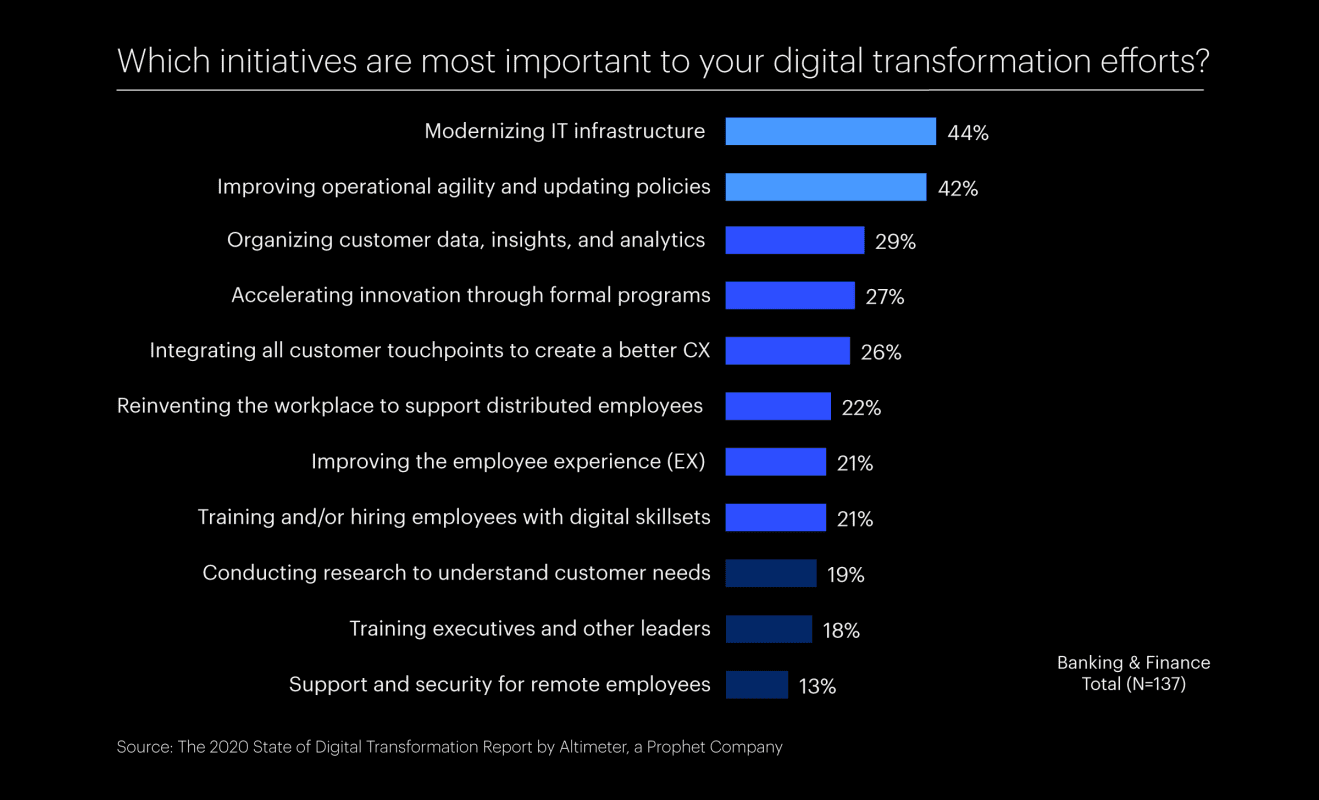

2) Make new ways to reach customers a higher priority

Optimizing internal processes is a compelling reason to pursue digital transformation, named by 40% of respondents and 33% name responding to COVID-19. And to create the resilience to navigate the current economic and health crisis, financial service executives recognize that their digital transformation should focus on improving operations and enable them to operate in a more agile and flexible way.

But our data suggest that these companies should give more weight to the many ways digital transformation could provide firms with opportunities to reach customers through new digital channels, particularly as more consumers look to engage primarily online.

As the market continues to change, and consumer preferences and tendencies evolve significantly due to COVID-19, financial services brands are picking up on the need to leverage advanced technology and data to become more flexible and agile.

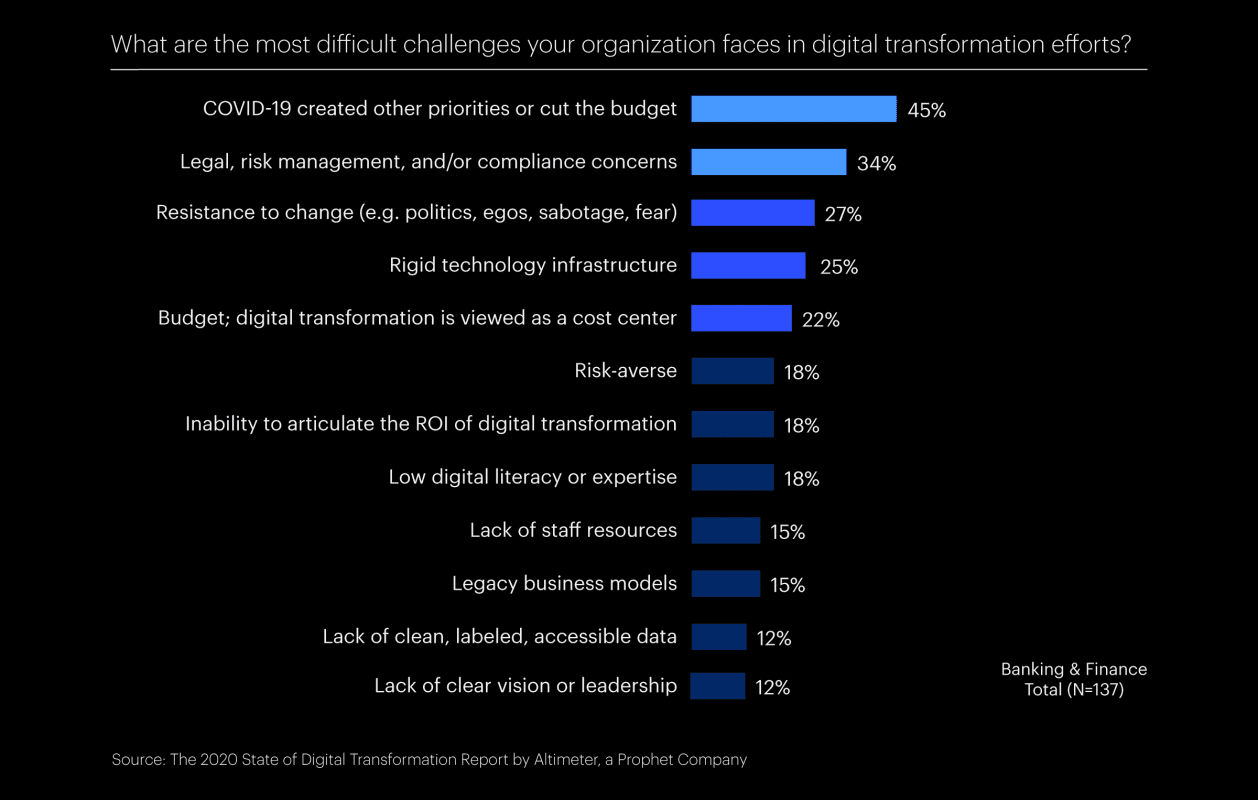

Transformation has not been easy, given legal hurdles and inherent resistance to change. And COVID-19 is creating new challenges. With urgent demands for supporting remote work and developing digital marketing and selling tools, the pandemic has hijacked many corporate priorities. In fact, 45% of our respondents say pandemic response and related budget considerations are the most significant challenge they face. And of course, traditional obstacles like risk management, resistance to change or rigid structures haven’t gone away.

The global economic and health crisis has impacted the way we think about digital transformation. This research underscores questions leaders within these companies should ask, to accelerate the transformation and achieve growth.

How has your organization accelerated or reprioritized its digital transformation initiatives in response to the current environment?

What obstacles are you encountering as part of that acceleration?

Is your agenda building greater operational resilience for your business?

Prophet’s financial services practice has been partnering with many clients in accelerating their digital transformation journey. Please contact us to learn more.

4 Ways Financial Services Companies are Supporting Customers Through COVID-19

Look for new and empathetic ways to offer guidance and provide relief.

COVID-19 is undeniably reshaping how we live and work.

Financial services companies may be better positioned than some other industries to weather this storm, but they – and the customers they serve – are nonetheless grappling with a variety of major shifts.

COVID-19 is not only impacting the way consumers and businesses interact with their financial services providers, but it is also impacting what they need from their financial services providers. For instance:

More businesses are seeking small business loans in response to the stimulus package.

More consumers need mobile banking solutions for items they previously would have visited for in-branch.

Increasingly, employers need to find the best way to keep their employees updated about potentially changing benefits.

As the effects of the COVID-19 crisis continue to unfold, we’re seeing four themes emerge.

Here’s how financial services and insurance companies are responding to the crisis today:

1. Providing an empathetic approach to addressing customers’ rapidly evolving needs, even “from a distance”

Banks, credit card companies, and insurance providers are working to provide easy access to information in a time of high uncertainty.

Banks that have previously been leaders in offering online banking – like Capital One and PNC – have been encouraging customers now more than ever to service their banking needs online with digital tools and services by reminding them how to check balances, pay bills, and transfer money online. They have also been expanding systems to ensure that they are able to handle an increase in inbound digital servicing. And, where possible, companies are deploying additional digital tools, including options to request payment deferrals and online chat services to enable customers to avoid longer than usual hold times at call centers.

“Companies are deploying additional digital tools, including options to request payment deferrals and online chat services to enable customers to avoid longer than usual hold times at call centers.”

Financial services and insurance companies are also empowering call service representatives to take action and address customers’ concerns directly without additional approvals. To deploy these new working norms, companies are launching additional training for customer service representatives who are bombarded by anxious customers. The trainings are focused on leading with empathy while being empowered to offer additional forms of financial relief.

2. Finding new ways to guide customers through a time of crisis

Some financial services companies are helping customers address their evolving financial situations through either an increase in available information or planning tools that enable customers to better navigate their financial picture given the uncertainty of the crisis. Examples of this response include Vanguard holding live webcasts and using a dedicated section of their website to educate customers on how to navigate market volatility, and HSBC is using its financial expertise to help customers manage their emergency finances with access to an Emergency Savings Fund Calculator tool.

3. Providing direct financial relief to customers or easing the pressure of monthly payments

Financial institutions including American Express, Chase, Discover, and many others have reported offering financial assistance or deferring payments in order to address the evolving financial situation caused by COVID-19. Furthermore, most companies are offering additional forms of relief that may be made available to customers who reach out and explain how COVID-19 has personally affected their personal financial situation or has caused hardship for their business. Depending on the provider, forms of relief include:

Waiving interest fees, late fees, or minimum payments for a period of time.

Not reporting payment deferrals such as late payments to credit bureaus.

Delaying due dates for some borrowers on cards, auto loans and mortgages.

Increasing spending limits for certain cardholders on a case-by-case basis.

In addition to providing payment deferral options, the top ten sellers of personal car insurance have pledged to give back more than $7 billion in reduced premiums through programs like Allstate’s ‘Shelter-in-Place Payback’ and Statefarm’s ‘Good Neighbor Relief Program.’

4. Giving philanthropic donations to support organizations that are providing direct aid to addressing the crisis

Many financial services and insurance companies have also already provided philanthropic donations focused on addressing issues of hunger and food insecurity, or to provide direct relief to community development organizations where the majority of their employees are located. Beyond giving donations to local communities and to support basic needs, some financial services companies have also provided additional donations to support broader communities including Bank of America’s pledge to support an initiative with Khan Academy to offer free online learning for Pre-K – Grade 12 students throughout this crisis. While USAA has committed that a portion of its donations will be designated to non-profits focused specifically on helping members of the military.

In the medium-term, we expect to see financial services and insurance companies begin to launch preliminary, near-term strategic responses. Given the continuously evolving nature of this ongoing situation, longer-term strategies will emerge as the pandemic slows and economies emerge with a clearer view of the new current state.

For many companies, the near-term and long-term strategies will require an accelerated digital transformation in order to meet changing customer needs and experience expectations. Companies will need to build smarter, faster and more flexible organizations to create new business models that operate at the pace of ever-changing markets in order to build and sustain crucial brand relevance.

If you need help figuring out what path to take now, in the next 6-8 months, or beyond, please don’t hesitate to reach out. We’re happy to have a conversation. Also, if you have any questions you’d like answered by our experts, drop them into the comments below or reach out directly here.

Asset-light thinking, “little” data and bundled services are all responding to changing customer needs.

Remember when “digital”, to most banks and financial institutions, simply meant getting online? Mobile apps, online banking, digitized systems for claims, servicing, etc. – this was the first wave of the digital agenda. But those days have quickly moved into the rear-view mirror, as new enablers and disruptors present opportunities, and challenges, for financial services firms to tackle.

“New enablers and disruptors present opportunities, and challenges, for financial services firms to tackle.”

Here, we’ve highlighted the four differentiators that financial services organizations should be considering over the next 5 years and beyond. We have identified the A, B, C and D of disruptive forces seen from the perspective of the customer, the key shifts affecting them, and consequently how financial services companies can adapt to these disruptive factors to drive their business forward.

A: Asset-Light: From Ownership to Access

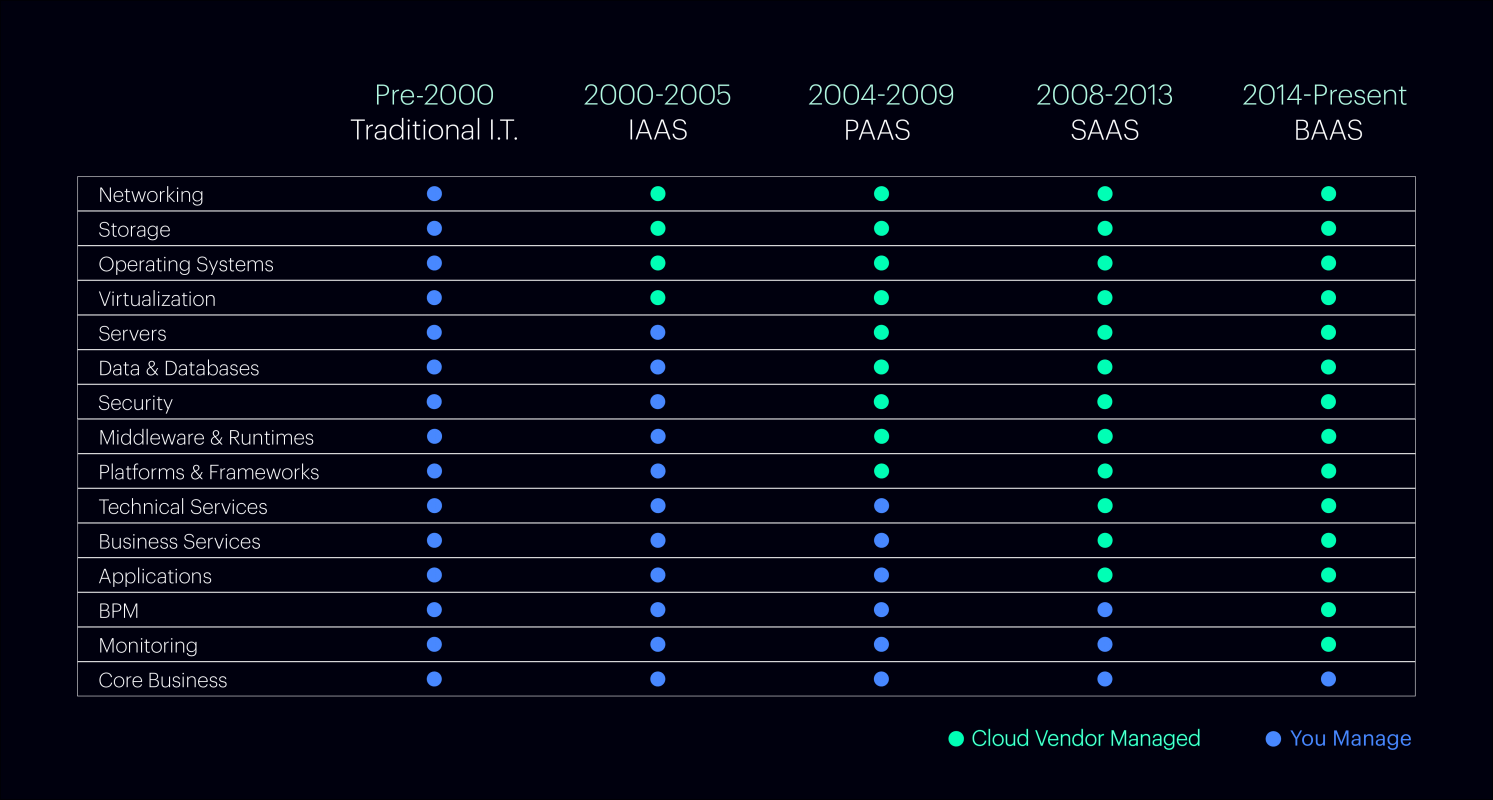

Banks that will succeed in the next 5 years will make the pivot towards being asset-light. First, this will require becoming asset-light as a company, e.g., smaller real estate footprint, fewer branches, less human staff in place of e-tellers, and so on. It used to be that you had to build it all yourself. Then, you could rent IT-as-a-service (IaaS), and over time you could rent products-as-a-service (PaaS), and eventually software-as-a-service (SaaS). Today, you can pretty much “rent” the entire business-as-a-service (BaaS), freeing you up entirely to focus on your core business. This is why asset-light companies have an advantage – they focus their full attention on their core business while building and scaling faster than ever.

Why Build the Foundation When You can Rent it?

But beyond the physical footprint, asset-light also means adapting to a customer who is more asset-light than ever – fewer houses, mortgages, cars, etc. Creating a more flexible and adapted product range to meet the needs of today’s asset-light customer will require a re-think of your firm’s product and service offerings.

B: Bundling: From More to Less

For years, big banks were a one-stop shop for all your financial needs – from your first savings account to credit card investments, mortgages, loans, and wealth management. These financial institutions had advantages in size (assets under management and customer count) and their global networks added a multiplier effect. They also had strong, globally-minded compliance systems in place to manage the difficult regulatory environment. So, they were hard to disrupt…if you tried to disrupt them in aggregate.

To overcome this competitive advantage, companies disrupted piece by piece, niche by niche, service by service. In the past 10 years, we’ve seen an emergence of niche players who entered the market and disrupted a very specific part of the value chain — Monzo (debit), Robinhood (investing), WeChat and Momo (payments), Revolut and Transferwise (FX), Stripe (B2B), etc. And they won share by being asset-light, freeing them up to deliver a better, more convenient (and sometimes affordable) experience.

But these niche players are no longer babies – they’ve grown up, raised billions, acquired millions of customers, and over time, have begun offering more comprehensive bundling of services.

For the first time since the fintech market took off 10-15 years ago, the big banks are no longer being disrupted in niche areas, they’re facing bigger threats as these formerly-niche-players bundle a more comprehensive set of services. It’s a global trend that customers are far more likely to refer a friend to a fintech than to a traditional bank.

So, today, who’s David and who’s Goliath?

C: Community: From Insular to Interoperable

For nearly a century, banks have thrived as closed systems, keeping data and assets in-house. But the rise of digital gave way to a new way: open source. It started in software, but over time open source became foundational to pretty much all businesses, none more so than financial services.

Meanwhile, openness isn’t just a customer nice-to-have, it’s becoming a regulatory norm. APIs that build and bridge communities and financial ecosystems will become a must. In this environment, financial services firms will need to strategically identify which data sources to share, based not only on what they can monetize, but what customers expect from a financial experience today.

But take note: openness is NOT about creating connections. It’s not simply enough to connect player A to player B.

Success comes down to creating community, which is about much more than connections. It’s about experiences. It’s sticky. Connections are a commodity – anyone can get access to APIs and connect things. But those who really create community do so in a way that creates stickiness, retention, loyalty. There’s a real value exchange, a real reason to come back time and time again.

D: Digital Identity: From Big Data to Little Data

For the past decade, the hype has been on big data. Collecting as much data as possible, storing it, and analyzing it. But the value actually lies in the “little” data — the data exhaust that you as a n=1 give off every day. Your daily schedule, shopping choices, patterns of travel, temperature preference in your home or car, physical health, emotions.

Google coined the term “ZMOT” a few years ago, with the idea that there was a single/zero moment of truth. That critical point when a decision is made. However, the reality is with little data, there are millions of moments of truth. When viewed in aggregate, they provide a much more compelling and interesting perspective of a person’s overall digital identity.

Millions of Moments of Truth

Companies that track, analyze and engage around “little data’ will be – and already are – the big winners, because they know you fully, not just in the realm of their industry or one-off interactions with you. They are becoming stewards of your digital identity.

As we undergo a shift from placing value on share of wallet to share of data, financial services companies are uniquely positioned to be those stewards of our digital identities. What we spend, where we travel, what we save, who we transact with, financial services companies are entrusted with millions of data points. And as trust in social media firms erodes, financial services firms are strongly positioned to be the owners of our digital identities for years to come.

If you would like to assess where your financial organization sits on the path to transformation, and where it can go next, connect here.

3 Ways to Build Brand Relevance for Financial Services in 2020

Consistency, trust and emotional engagement can help companies impress and inspire their audiences.

Financial services companies have a relevance problem. Consumers – who will often be heard enthusiastically talking about everything from kitchen appliances to Band-Aids – yawn when they think about banks and insurance companies. Our research shows that consumers are more interested in just about every other category compared to the companies that are working to safeguard their financial stability and helping them plan for the future.

It doesn’t have to be that way. At Prophet, we’ve spent years exploring the science of relevance, surveying 51,000 global consumers each year about thousands of brands. Our Brand Relevance Index quantifies how indispensable a given brand is to people in their daily lives. And we do it by ranking each brand against four key drivers of relevance:

Customer obsessed: brands that know you better than you know yourself

Distinctively inspired: brands that win your head and heart, often with a strong purpose

Ruthlessly pragmatic: brands that are right where you need them, making your life easier

We’ve found that relevance drives business impact – the most relevant brands outperformed the S&P 500 average revenue growth by 230% over the past ten years. We help clients use these insights to be more relevant in their customers’ lives by engaging with them in ways that build more excitement, trust and loyalty, whilst also building their bottom line.

Why Do Financial Brands Disappoint?

Companies like Apple, Amazon and Netflix consistently dominate our ranking, generating almost endless brand love. But financial services brands have consistently underperformed compared to other industries. Only one brand – Intuit TurboTax (No. 37) – breaks into the top 40 in our U.S. index. And just four more – PayPal (No. 43), Vanguard (No. 44), USAA (No. 46) and Zelle (No. 48) – manage to sneak into the top 50. While consumers do find financial-data companies moderately relevant to their daily lives, property and casualty insurance, life insurance and retail banking occupy the three lowest rungs of all 27 categories we measure.

Familiarity isn’t the problem. These are brands with high levels of awareness. And, in the case of retail banking, consumers constantly interact with these companies, from paying their mortgage to buying their morning latte. But, there are three primary reasons people feel so detached from these brands:

They’re Inconsistent

Except for financial data services, where 77% of consumers say companies deliver a consistent experience, people say financial services companies are all over the map in terms of their performance. For instance, only 29% say retail banking and investments are consistent, 23% for P&C insurers and just 15% for life insurance companies.

They’re Not Trustworthy

The days when people found financial service companies inherently honest and reliable are long gone. Amid daily headlines about privacy scandals, security hacks and breaches, consumers rank trust as the second-most important attribute for financial data services. Assessed simply on trust, some soar – PayPal, TurboTax, Vanguard and Fidelity are seen as the most trustworthy of all brands. But others fare terribly, with Wells Fargo, Liberty Mutual and PNC among the lowest-performing brands.

Indispensable? Yes. Inspirational? No

Consumers certainly understand that financial services are essential. When we rank brands by “Meets an important need in my life,” for example, TurboTax comes in third, and Visa, Vanguard and Fidelity are in the top 20. But, all stumble on measures of inspiration and emotional engagement, and our data shows that those misses can create a real risk of customer turnover.

3 Ways to Increase Brand Relevance

In our work with financial services companies, we’re helping clients focus on the levers most likely to boost relevance. Take a look at three ways we’re guiding brands to develop richer, deeper and more meaningful relationships with their customers:

1. Impact When It Counts

Brands like Zelle and PayPal have made consumers’ lives infinitely easier by being there for them at every single payment moment that matters. Both brands score more than 95% for “makes my life easier.” Many financial services companies are failing to address the pain points in the customer experience journey. Increasing focus should be given to simplifying processes and exchanges and identifying opportunities to create those all-important memorable and meaningful moments for customers that are tailored personally to their needs and to their lives.

2. Tap Into the Power of Purpose

We help cultures and organizations evolve to find a higher order purpose, that is unique to their company and genuinely resonates with customers and employees. As consumers, particularly younger ones, flock to brands that support their commitment to sustainability and fairness, financial services companies must stand for something more than profits.

Among insurers, for example, brands like USAA and Aflac have built strong relationships by making consumers feel that they can connect on more than just a functional level. USAA, for example, with its deep commitment to the military community, earns an enviable 99% on “has a set of beliefs and values that align with my own” – the third-highest of all companies we track in the U.S. And Aflac and Vanguard aren’t far behind. By comparison, only 1% say that is true of MasterCard.

3. Cultivate Emotional Engagement

With the right experiences and innovations, financial service brands can radically improve their emotional connections with consumers. We might even argue that they have an inherent advantage here, given how often customers interact with their brands.

“We help clients use these insights to be more relevant in their customers’ lives by engaging with them in ways that build more excitement, trust and loyalty, whilst also building their bottom line.”

We’re realists. Will paying a quarterly car-insurance bill ever make someone as happy as seeing a Pixar movie, shopping on Etsy or going to Disneyworld? No. But companies as varied as AARP, Lemonade and John Hancock have made sure that each touchpoint makes consumers “feel emotionally engaged”. By comparison, only 21% can say that of TurboTax, and just 13% about Visa.

There are many roads to relevance. Let us help you find the ones that will resonate most with your audience, and translate that into meaningful revenue growth, talk to our expert consultant team today.

Digital Marketing Priorities in Financial Services for 2019

Our research shows that lead generation and customer experience top the list. And hiring is a major headache.

It’s clear that emerging Fintech and Insuretech entrants are shaking up financial services. Across the board – from large to small-scale companies – we’re observing an accelerated need for more digitally fluent marketing organizations to tackle new challenges in an evolving market.

To understand the challenges and priorities impacting the insurance and banking industries today, we turned to Prophet’s digital analyst group Altimeter surveyed 68 global financial services executives as part of their industry-wide 2019 State of Digital Marketing report that spoke to over 500 executives in North America, Europe and China.

“Altimeter surveyed 68 global financial services executives as part of their industry-wide 2019 State of Digital Marketing report.”

The report surfaced three primary digital marketing insights specific to where financial services executives are betting their marketing investments to address business challenges:

Lead generation and customer experience are the top digital marketing priorities.

Scaling marketing innovation, the right talent and proving impact are the greatest challenges.

Data analysis, marketing automation and UX design are the most sought after skills.

Let’s dive into the results.

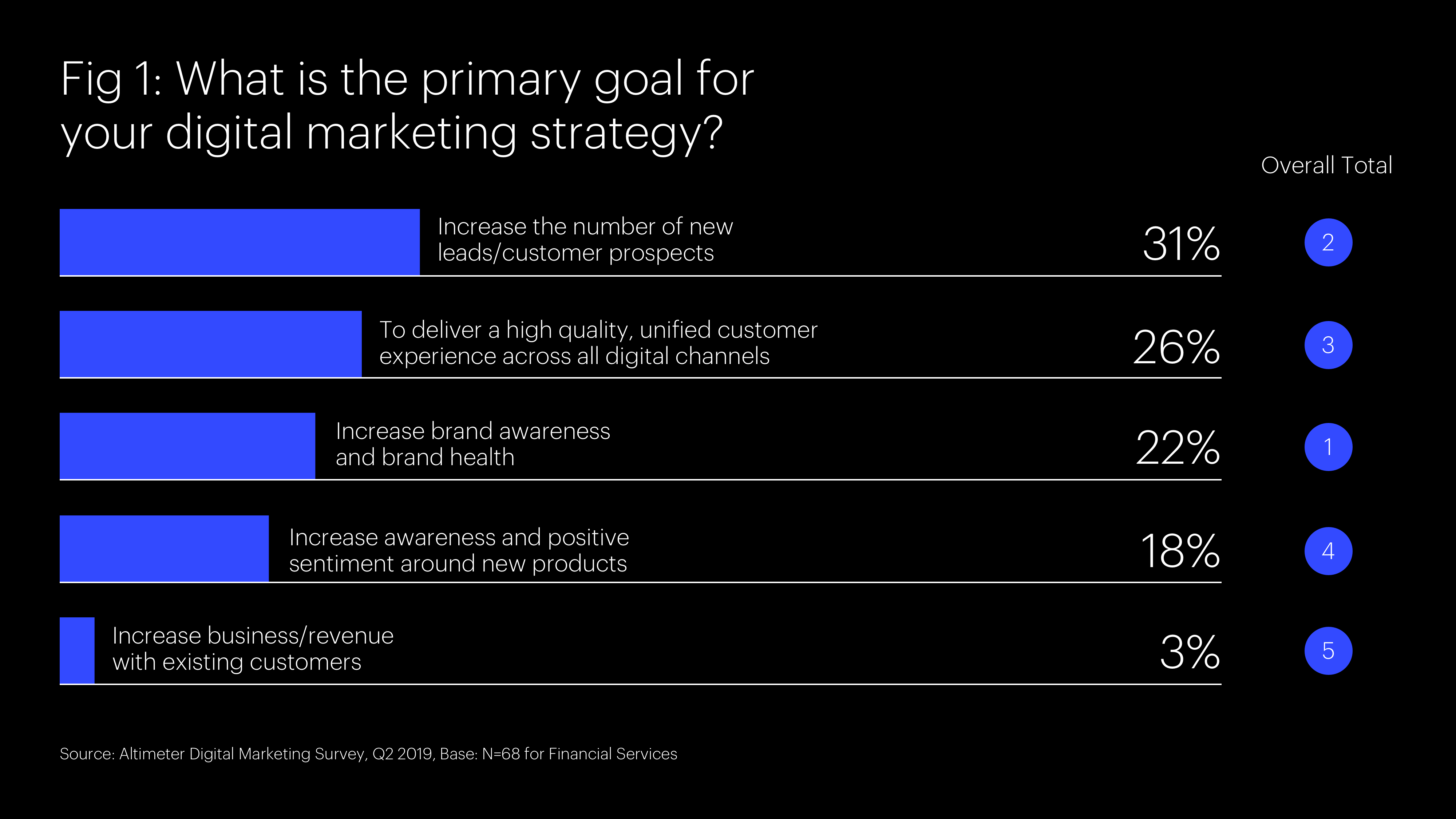

1. Lead generation and customer experience are the top digital marketing priorities.

Lead generation and customer experience came out on top (see Figure 1) – ranked higher than brand awareness and brand health – a top priority across other industries.

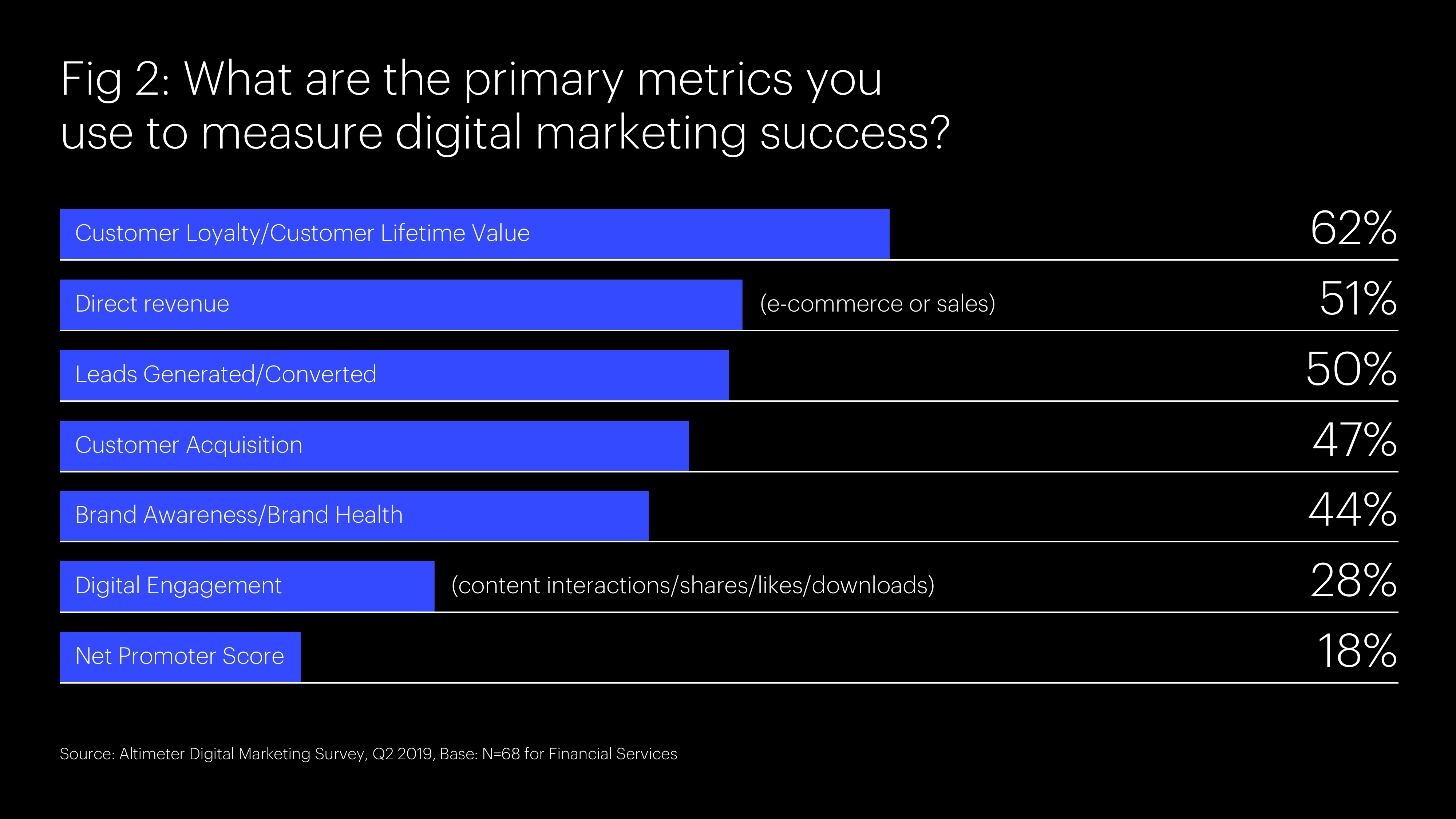

To measure digital marketing success, financial services companies are placing greater emphasis on customer loyalty/customer lifetime value (CLTV) – even before direct revenue (see Figure 2).

We see these forces working within financial services companies that are investing more to acquire customers through digital demand-building activities. Specifically, with the increases in the promotion of banking, investment and insurance products going more digitally direct-to-consumer. We also see loyalty as a rising metric to diagnose and resolve potential attrition challenges before being confronted.

2. Scaling marketing innovation, the right talent and proving impact are the greatest challenges.

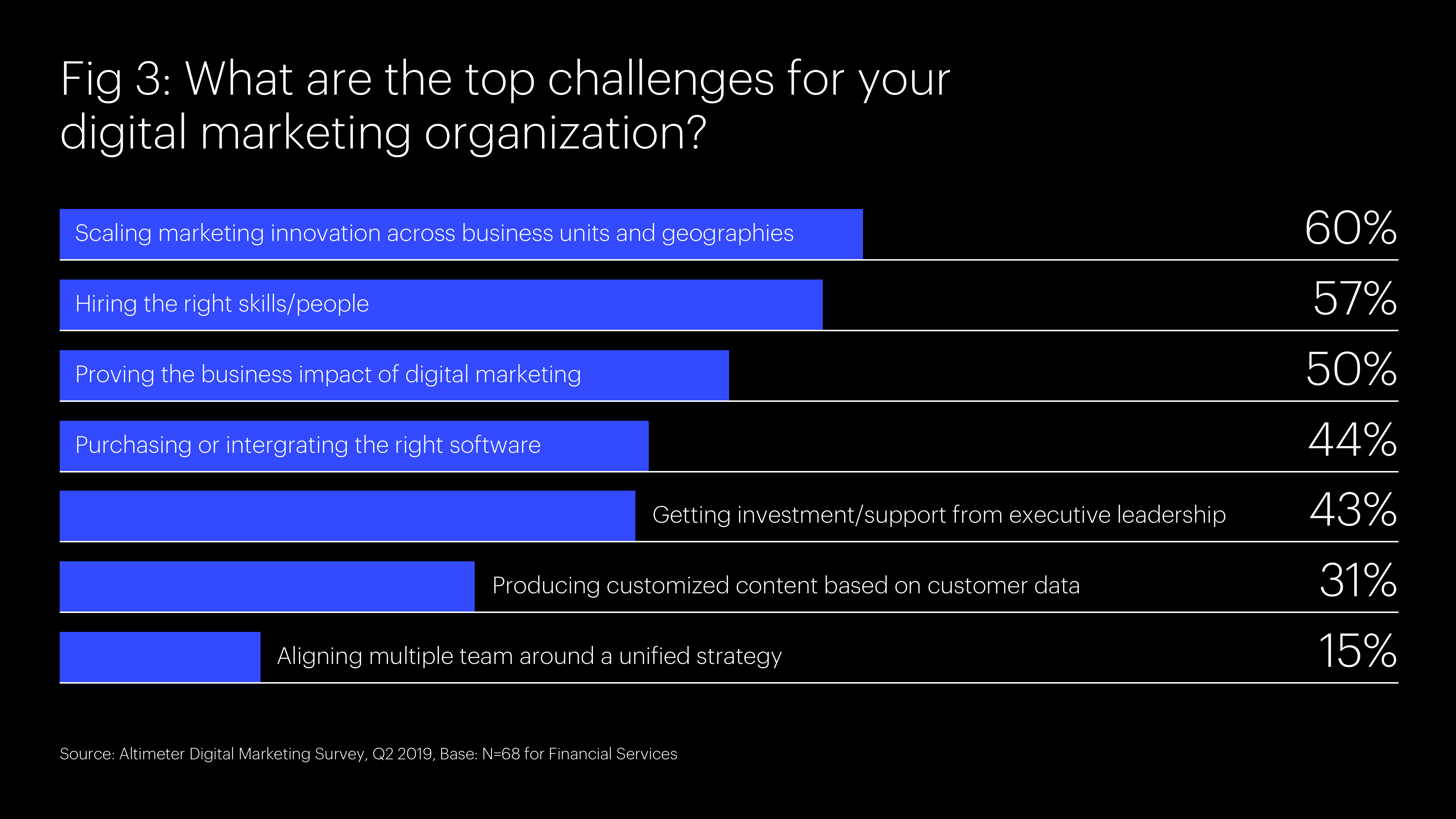

Financial services marketing organizations are navigating several challenges with their focus on lead generation and CX development, particularly around scaling, hiring and proving business impact (see Figure 3).

In addition, we learn that compared to other industries, financial services companies are experiencing a much greater challenge in seeing a return on investment for their marketing technology spend with 32 percent saying that it took a long time before they saw any return. Consequently, it is now considered to be their top Martech challenge.

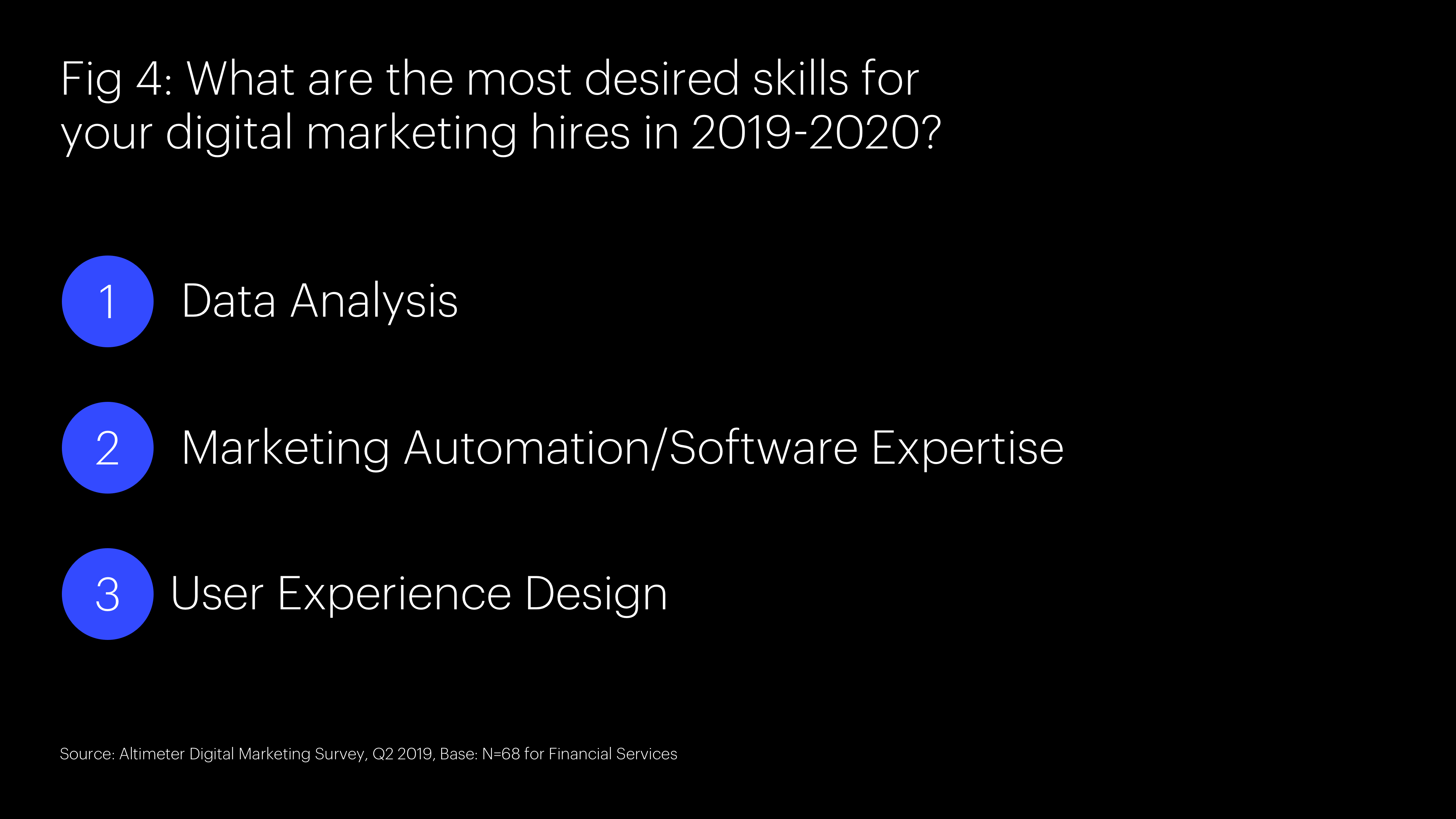

3. Data analysis, marketing automation and UX design are the most sought-after skills.

Financial services companies are now focused on building capabilities in data analysis, marketing automation, and user experience design (see Figure 4) to enable the scaling of marketing innovation across the full enterprise and ultimately to prove business impact.

Financial services companies as a consequence are finding the need for capabilities to apply digital marketing in new ways previously not considered.

These evolving digital marketing priorities are making way for the future

What’s clear from the findings of Altimeter’s 2019 State of Digital Marketing report is that as financial services companies place greater emphasis on driving customer acquisition and shaping customer experiences, marketing must bring in new capabilities formally nascent within the organization, invest in the right marketing technology, and prove business impact on a small – yet scalable – way.

At Prophet, we help our clients drive uncommon growth through transformation. We work with leaders across the insurance and banking categories to understand where to play and how to win to unlock the full potential of the brand and customer relationships. Learn more with our guide to digital marketing excellence here or get in touch today.

6 Actions to Build an Insurance Service Strategy that Drives Growth

Our research finds that consumers expect more, and want products combined with services.

Over the past several years insurance companies have faced increased product commoditization due to ubiquitous online presence, more sophisticated aggregators and the increased availability of insurance products. They are faced with the challenge of driving growth while managing their risk profiles to be less capital-intensive. In a market with heightened expectations for digital experiences – which the COVID-19 pandemic raised even more – the likes of Oscar, Lemonade and other new DTC market entrants are raising consumer expectations, spurring companies to develop more experience-led strategies to drive engagement and value. Then there’s other players like American Express and Chase making their play.

Where should insurers look to drive growth?

Against this backdrop, Life, Health and P&C insurers are turning to new services to drive growth and engagement. Services create more compelling and differentiated solutions that focus on customer needs, going above and beyond basic insurance coverages. This enables insurers to identify new streams of less capital-intensive revenue and increase demand for existing products – especially in a category that has historically struggled to drive engagement at moments outside of the core product moments (e.g., purchase, premium payment and claim).

Based on our extensive experience and research within the industry, integrating a services strategy also translates into impactful business outcomes for insurers globally – from initial purchase intent to long-term customer retention. The results speak for themselves:

Customers were twice as interested in an insurance product when sold with relevant services (Source: Prophet Insurer Research)

The presence of services impacts broker interest with three-quarters of brokers stating that services are critical to their choice of provider when recommending to clients (Source: Prophet Insurer Research)

Insurers who offer three or more services on top of the core product see NPS increases between 20-40 points.

When it comes to services, who is doing it well?

Insurers are already recognizing the value services can bring both to their customers and their business. However, as many insurers do not have exclusive relationships with services providers, avoiding services replication across the industry is key. Insurers are therefore partnering and acquiring across the services ecosystem to uniquely deliver new customer value.

P&C providers are already seeing strong integration of services into their offers given their ability to utilize customer tracking and connected devices, not only providing product discounts but also additional services on-top. For example, Progressive Insurance has partnered with TrueMotion to launch Snapshot, a service that monitors and measures driver data through either their smartphones or a plug-in device. This enables customers to understand their driving habits and generate personal discounts. Progressive is continuing to explore expansions to the program and invest in partnerships to combat distracted driving.

“Integrating a services strategy also translates into impactful business outcomes for insurers globally – from initial purchase intent to long-term customer retention.”

Health and Life are also now capitalizing upon the opportunity to integrate services into their portfolios by exploring the way they can utilize health tracking to adjust premiums through improved health. From a global standpoint, Vitality is one example of a brand that has developed a personalized customer health and wellness tracking and support platform. In the U.S. specifically, John Hancock has partnered with Vitality to provide discounts and tailored recommendations to their customers based on their health tracking. While in Asia, AIA has made a focused push to expand the solutions they offer to customer across the region.

Health insurers also are exploring the role of partnerships with preventative health start-ups to help customers manage chronic illnesses. For example, Cigna has partnered with Omada Health to offer customers a personalized preventative health solution to mitigate risk against diabetes, heart disease and stroke.

Six actions for insurers to create impact and drive growth through services

We believe there are six actions insurers take to develop a winning services strategy:

Understand what customers want. What is the foundational understanding of customer wants and needs to guide services development?

Identify the business opportunity. What role could and should services play for your business and what business objectives should your services strategy inform (i.e., acquisition, incremental revenue, retention, efficiency)?

Prioritize unique and relevant services. What are the set of unique services most relevant to your customer base that you will prioritize developing?

Drive engagement. Where and when within the journey do customers become aware of services and how do we improve interest for them?

Improve the experience of access and use. What is the right experience behind driving easier services access and use to deliver greater customer value?

Identify the right internal owners. Who within the organization is responsible for funding, building and managing our services strategy?

Insurers are falling short on delivering value to customers. A well-defined services strategy can nurture customer relationships and earn loyalty to fuel growth.

If you’d like to learn more about the role of services and how we have helped leading insurance companies execute experience-led strategies that drive impact and engagement, get in touch.