Now in its fifth year, our annual “State of Digital Transformation” research continues to document the constantly evolving enterprise. As disruptive technologies and their impact on organizations and markets continue to progress, our research aims to capture the shifts and trends that are shaping modern digital transformation.

In 2019, strategic digital transformation is only becoming more pervasive moving beyond IT to impact competitiveness throughout the organization. Budgets are soaring. The list of disruptive technologies on the radar of stakeholders is expanding. Ownership is moving to the C-Suite and managed by cross-functional, collaborative groups. Customer experience (CX) continues to lead digital transformation investments, but as we observed in 2017, employee experience and organizational culture are also rising in importance to empower and accelerate change, growth, and innovation.

Digital Transformation as an Enterprise-Wide Movement

This year, it’s clear that digital transformation is maturing into an enterprise-wide movement. Digital transformation is modernizing how companies work and compete and helping them effectively adapt and grow in an evolving digital economy.

What’s also evident is that there is still much work to do as companies are, by and large, prioritizing technology over grasping the disruptive trends that are influencing markets and, more specifically, customer and employee behaviors and expectations.

The State of Digital Transformation: 5 Key Takeaways

A successful digital transformation is an enterprise-wide effort that is best served by a leader with broad organizational purview. For the second year in a row, CIOs are reported as most often owning or sponsoring digital transformation initiatives (28%), with CEOs increasingly playing a leadership role (23%).

Market pressures are the leading drivers of digital transformation as most efforts are spurred by growth opportunities (51%) and increased competitive pressure (41%). With high-profile data breach scandals making daily headlines, new regulatory standards like GDPR are also providing impetus for organizations to transform (38%).

While there is a growing acknowledgment of the importance of human factors in digital transformation – like employee experience and organizational culture – most transformation efforts continue to focus on modernizing customer touchpoints (54%) and enabling infrastructure (45%). But many organizations are not doing their due diligence when it comes to understanding their customers, with 41% of companies making investments in digital transformation without the guidance of thorough customer research.

Organizational buy-in remains a top challenge for those leading digital transformation. The companies we studied report digital transformation is still often perceived as a cost center (28%), and data to prove ROI is hard to come by (29%). Cultural issues also pose notable difficulty, with entrenched viewpoints, resistance to change (26%), and legal and compliance concerns (26%) stymieing progress.

Innovation is staking its claim within the organization. Nearly half of respondents report that they are building a culture of innovation, with in-house innovation teams becoming the norm

Digital Marketing Priorities in Financial Services for 2019

Our research shows that lead generation and customer experience top the list. And hiring is a major headache.

It’s clear that emerging Fintech and Insuretech entrants are shaking up financial services. Across the board – from large to small-scale companies – we’re observing an accelerated need for more digitally fluent marketing organizations to tackle new challenges in an evolving market.

To understand the challenges and priorities impacting the insurance and banking industries today, we turned to Prophet’s digital analyst group Altimeter surveyed 68 global financial services executives as part of their industry-wide 2019 State of Digital Marketing report that spoke to over 500 executives in North America, Europe and China.

“Altimeter surveyed 68 global financial services executives as part of their industry-wide 2019 State of Digital Marketing report.”

The report surfaced three primary digital marketing insights specific to where financial services executives are betting their marketing investments to address business challenges:

Lead generation and customer experience are the top digital marketing priorities.

Scaling marketing innovation, the right talent and proving impact are the greatest challenges.

Data analysis, marketing automation and UX design are the most sought after skills.

Let’s dive into the results.

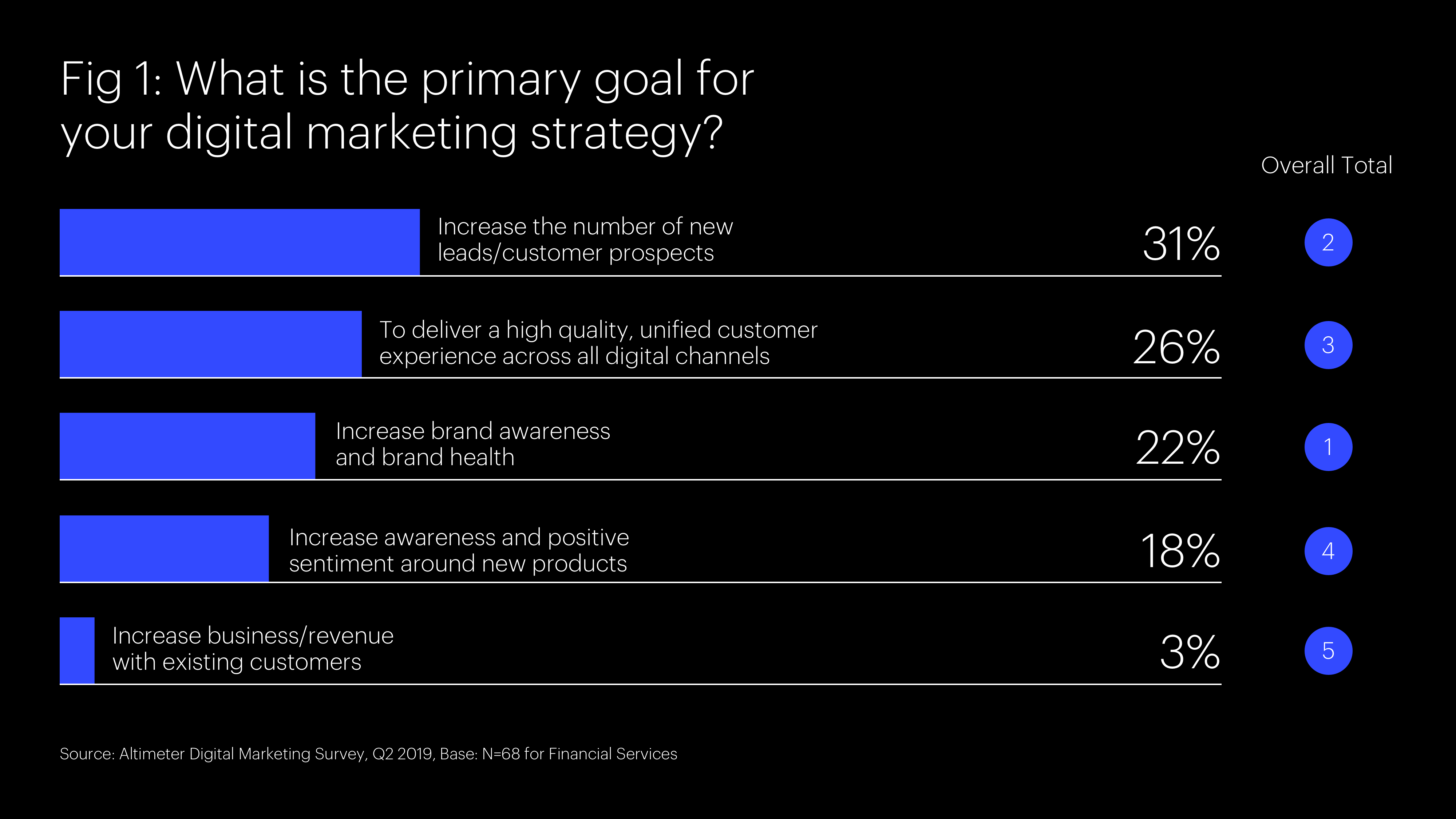

1. Lead generation and customer experience are the top digital marketing priorities.

Lead generation and customer experience came out on top (see Figure 1) – ranked higher than brand awareness and brand health – a top priority across other industries.

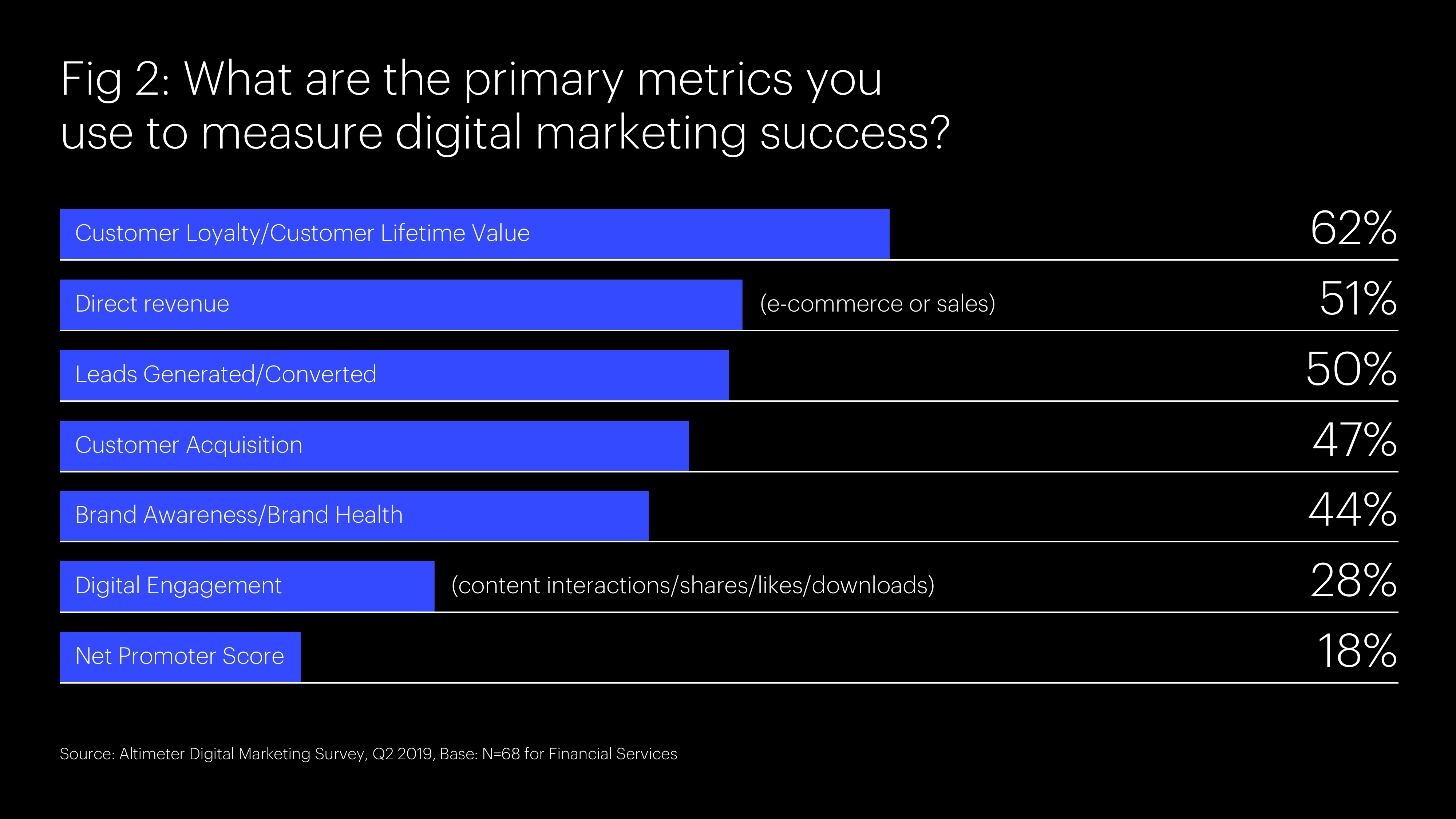

To measure digital marketing success, financial services companies are placing greater emphasis on customer loyalty/customer lifetime value (CLTV) – even before direct revenue (see Figure 2).

We see these forces working within financial services companies that are investing more to acquire customers through digital demand-building activities. Specifically, with the increases in the promotion of banking, investment and insurance products going more digitally direct-to-consumer. We also see loyalty as a rising metric to diagnose and resolve potential attrition challenges before being confronted.

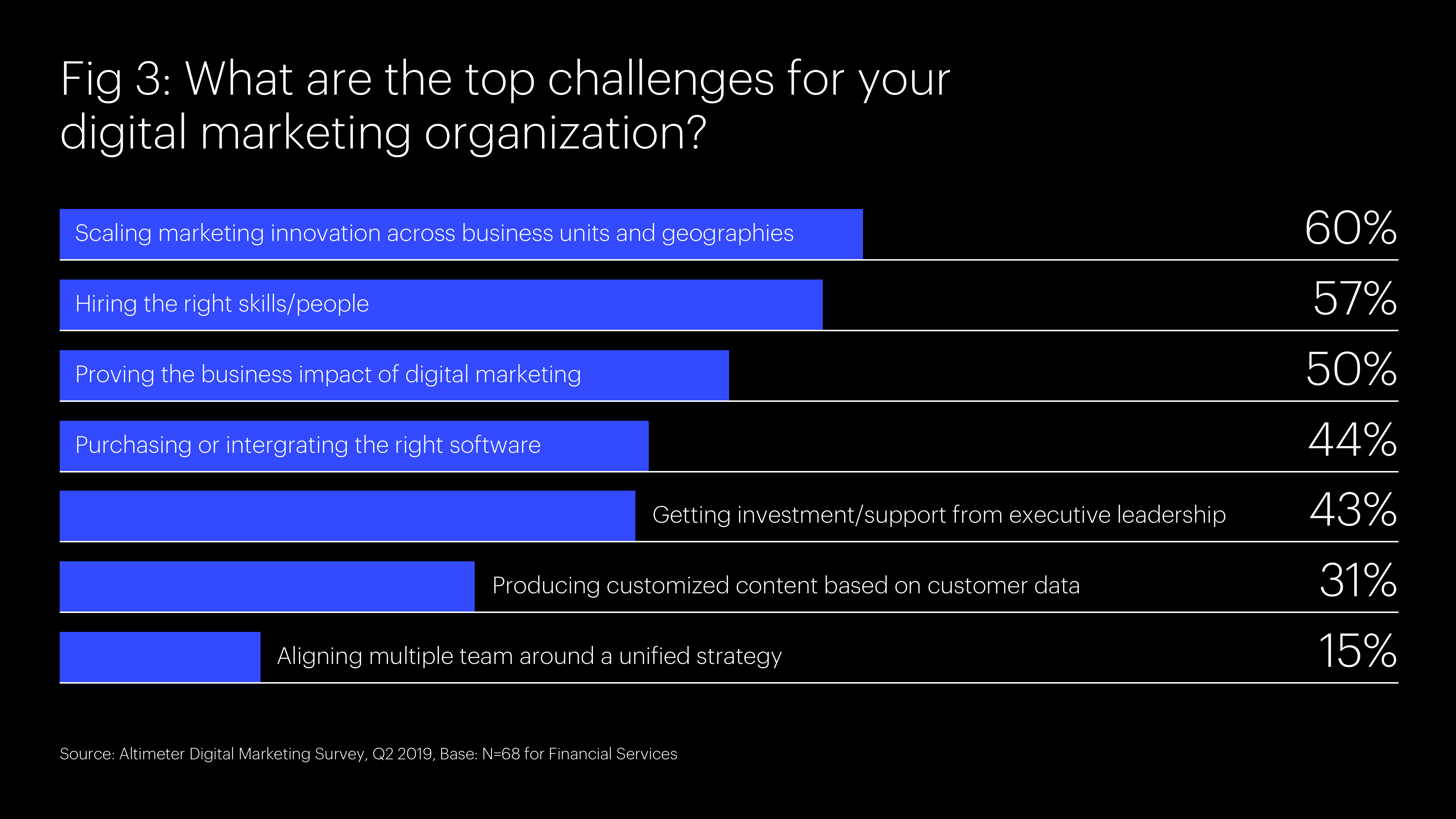

2. Scaling marketing innovation, the right talent and proving impact are the greatest challenges.

Financial services marketing organizations are navigating several challenges with their focus on lead generation and CX development, particularly around scaling, hiring and proving business impact (see Figure 3).

In addition, we learn that compared to other industries, financial services companies are experiencing a much greater challenge in seeing a return on investment for their marketing technology spend with 32 percent saying that it took a long time before they saw any return. Consequently, it is now considered to be their top Martech challenge.

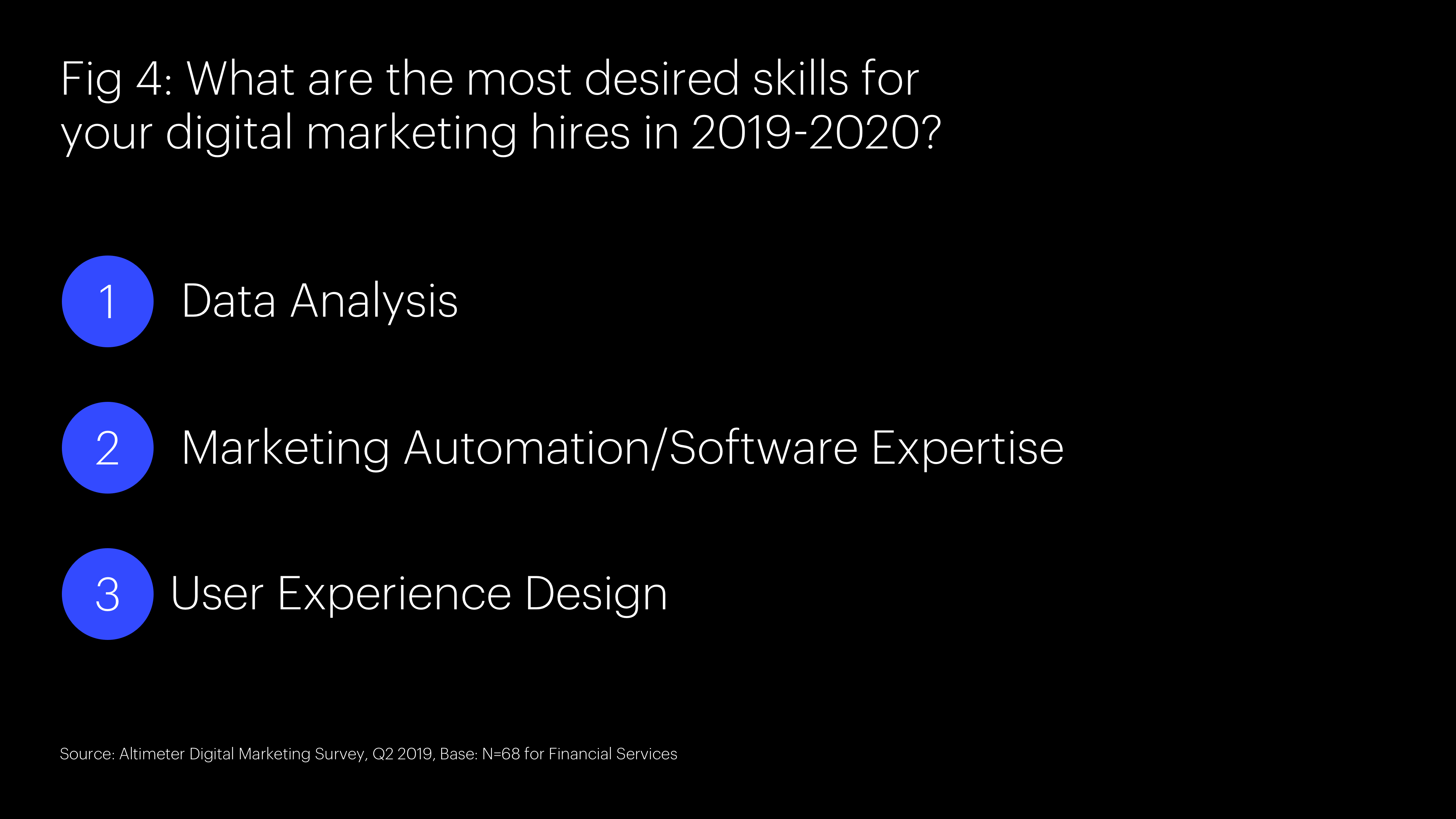

3. Data analysis, marketing automation and UX design are the most sought-after skills.

Financial services companies are now focused on building capabilities in data analysis, marketing automation, and user experience design (see Figure 4) to enable the scaling of marketing innovation across the full enterprise and ultimately to prove business impact.

Financial services companies as a consequence are finding the need for capabilities to apply digital marketing in new ways previously not considered.

These evolving digital marketing priorities are making way for the future

What’s clear from the findings of Altimeter’s 2019 State of Digital Marketing report is that as financial services companies place greater emphasis on driving customer acquisition and shaping customer experiences, marketing must bring in new capabilities formally nascent within the organization, invest in the right marketing technology, and prove business impact on a small – yet scalable – way.

At Prophet, we help our clients drive uncommon growth through transformation. We work with leaders across the insurance and banking categories to understand where to play and how to win to unlock the full potential of the brand and customer relationships. Learn more with our guide to digital marketing excellence here or get in touch today.

The growing adoption of Internet of Things (IoT) consumer electronics — such as smart thermostats and digital assistants — has paved the way for brands to use connected devices in their physical spaces too. The same sophisticated technology that powers “smart home” devices is slowly finding its way into stores, hospitals, and other public spaces, creating “smart places.”

For this report, we outline how location-based brands can take the battle offline by investing in technology-rich locations that raise the bar for Customer Experience (CX).

We also examine the barriers brands will face, balancing the value of enhanced consumer insights, customer experience, and operational efficiencies against heightened risks around consumer privacy.

Key Findings:

Detailed use cases distilled from research into hundreds of different ‘smart place’ devices

Interviews with early adopters, device makers, industry groups, and vendors who focus on CX management in physical locations

Recommendations for incorporating these technologies into your business strategy, and the challenges therein

In the new report, “The 2017 State of Digital Transformation,” we surveyed more than 500 executives and digital strategists to understand the current challenges and opportunities they are facing as they undergo a digital transformation.

This is the third annual report on the topic from Altimeter principal analyst Brian Solis. This year builds on his 2016 research and reveals how, why, and to what extent businesses are investing in digital strategies, initiatives and operational models. The good news is a growing number of businesses are investing in innovation strategies to uncover new growth opportunities. The bad news is most companies surveyed are ignoring the pervasive changes happening to connected consumers’ buying behaviors.

Key Findings

While businesses cite “evolving customer behaviors and preferences” as the top driver of digital transformation, fewer than half invest in understanding digital customers.

Some executives are beginning to own digital transformation efforts, and the Chief Information Officer (CIO) is most often at the helm (28%). As all companies increasingly become “technology companies,” the roles of the CIO and IT department are more important than ever — but true success in digital transformation is an enterprise-wide, cross-functional endeavor.

Companies and their change agents still face big challenges in the pursuit of digital transformation, including a lack of digital talent and expertise (31.4%), the perception that digital transformation is a cost center and not an investment (31%), and general culture issues (31%).

While companies are making attempts to modernize employees’ skillsets for a digital economy with new training programs (62%), only about half are investing in new digital talent. The employee experience is a crucial, yet often overlooked element of a successful digital transformation.

Undergoing a Digital Transformation? Get a Digital Maturity Assessment

To help companies navigate the digital transformation journey, Altimeter and Prophet have developed a diagnostic that assesses a company’s digital maturity. The tool provides an objective look at the current digital state vs. ideal future state while identifying major perceived gaps and opportunities that can be pursued as part of the digital transformation journey. Contact us today to learn more.

What’s Driving Digital Transformation Across Organizations?

Building on his 2014 research of digital transformation, principal analyst Brian Solis studied how companies are changing, and the challenges and opportunities they face while undergoing a digital transformation. Based on insights and data from more than 500 digital strategists and executives, the report found that companies are still facing significant challenges to operating in a digital economy.

The report, “The 2016 State of Digital Transformation,” shares the latest facts and figures on the top drivers, challenges and best practices of companies that are undergoing a digital transformation.

Key Findings

In our research, we identified key insights and trends impacting companies going through a digital transformation.

Customer Experience (CX) remains the top driver of digital transformation but IT and marketing still influence technology investments

55% of those responsible for digital transformation cite “evolving customer behaviors and preferences” as the primary catalyst for change. Yet, the number one challenge facing executives (71%) is understanding behavior or impact of the new customer

Only half (54%) of survey respondents have completely mapped out the customer journey. This means that many companies are changing without true customer-centricity 41% of leaders surveyed said they’ve witnessed an increase in market share due to digital transformation efforts, and 37% cite a positive impact on employee morale

The CMO vs. CIO: Digital transformation is largely led by the CMO (34%) not the CIO/CTO (19%)

Innovation tops digital transformation initiatives at companies today. 81% said it was at the top of their agenda, 46% stated their company has launched a formal “innovation center.” Right behind innovation was modernizing IT infrastructure (80%) and improving operational agility (79%)

Undergoing a digital transformation? Contact us for a digital maturity assessment.

To help companies navigate the digital transformation journey, Altimeter and Prophet have developed a diagnostic that assesses a company’s digital maturity. The tool provides an objective look at the current digital state vs. ideal future state while identifying major perceived gaps and opportunities that can be pursued as part of the digital transformation journey. Contact us today to learn more.

How Companies Are Investing in the Digital Customer Experience

Digital transformation isn’t a trend owned by a particular role, nor a discipline that belongs to one department alone. It is, however, a significant movement where daring business leaders venture into tomorrow’s markets, today.

In 2013, Altimeter researched how businesses explore digital transformation. One finding revealed that while the word “digital” is part of “digital transformation,” the essence of digital transformation comes down to people and how their digital behaviors differ from that of the traditional customers before them. It’s also more than that.

In our initial report on the topic, Digital Transformation: Why and How Companies Are Investing in New Business Models to Lead Digital Customer Experiences, we set out to determine how digital transformation unified disparate digital efforts under a common vision. In the process, we uncovered a more human story. We followed up our initial research with a 2014 survey, aimed at digital strategists, to further understand the state of digital transformation.

This report shares its results and is designed to complement Altimeter’s annual State of Social Business report. Combined, this research helps strategists drive social business evolution and digital transformation based on insight from peers and market leaders.

In our research, we learned that digital transformation is a movement progressing without a universal map to guide businesses through proven and productive passages. This leaves organizations pursuing change from a known, safe approach that correlates with “business as usual” practices. Operating within the confines of traditional paradigms without purpose or vision eventually challenges the direction, capacity, and agility for thriving in a digital economy.

After several years of interviewing those helping to drive digital transformation, we have identified a series of patterns, components and processes that form a strong foundation for change. We have organized these elements into six distinct stages:

Business as Usual

Present and Active

Formalized

Strategic

Converged

Innovative and Adaptive

Collectively, these phases serve as a digital maturity blueprint to guide purposeful and advantageous digital transformation. Our research of digital transformation is centered on the digital customer experience (DCX) and thus reflects one of many paths toward change. We found that DCX was an important catalyst in driving the evolution of business, in addition to technology and other market factors.

M&A Portfolios: Are You Thinking Like a Digital Native?

Companies need radical flexibility, not “house of brands” hang-ups.

After several quarters of near-frenzy pace, global deal-making is starting to slow. But for those in charge of managing portfolio and architecture strategy, the recent mergers and acquisition binge is creating something of a mess.

Many of the decisions about customers, brands and marketing have been addressed too quickly as deals were coming together. And once the integration process starts, those initial plans unravel. As the financial and operations teams that finalized deals hand them off to those responsible for taking new assets to market, tangles of false assumptions and the sub-optimal use of brand assets emerge; the value creation logic of the deal never gets out of the spreadsheet. And with $1.24 trillion in deals already on the books this year, that confusion presents material risk for shareholders.

Increasingly, clients are coming to us for help figuring out the best ways to organize and manage new, post-deal asset bases. Often, they start by asking: “Should we be a house of brands? Or a branded house?”

“Should we be a house of brands? Or a branded house?”

We’re not afraid to say that’s simply the wrong question. Digitally-focused companies can’t afford to think that way. The modern approach to architecture and portfolio strategy, and the one inherently chosen by digital natives, is radical flexibility.

Older companies are coming to understand this, too, focusing on customers earlier in the M&A process, aware that integration management offices are often working with incomplete data.

In order to get this right and maximize the value of today’s deals, we believe the best post-merger decisions come down to answering three essential questions.

Three Essential Questions For the Best M&A Portfolio Strategy

1. Are we customer-obsessed?

Our research on brand relevance offers compelling evidence that companies that are obsessed with customers significantly outperform others. It’s no surprise that the names that dominate the top of the Prophet Brand Relevance Index® are digital-first, including Apple, Amazon and Netflix. And those at the top of the list consistently outperformed the S&P 500 by 3x in revenue and 205x in profit in the last decade. These companies constantly ask themselves: Are we putting customer-use cases and environments first? All decisions are filtered through the perspective of customers and prospects.

When considering customers first—the buyers, the deciders–it’s easy to see how easily a company like Procter & Gamble and Schick might be outflanked. Direct-to-consumer brands like Dollar Shave Club and Harry’s have devoted themselves to changing and improving the razor shopping experience, rather than focusing on promotions and product features.

In post-M&A environments, brand portfolios should be built around key customer use cases, balancing the desire for efficiency with a customer-centric model that leverages the strongest brand for each use case. When J.P. Morgan & Co. and The Chase Manhattan Bank merged, they prioritized efficiency over customers and created a brand mash-up that weakened both brands. After a couple of years of brand value degradation, a new strategy that led with customer needs was founded with a powerful institutional brand, J.P. Morgan, and a powerful retail brand, Chase. This approach allows for effective targeting of clearly defined customer segments with separate brands and tailored offerings, and is paying off for JPMorgan Chase, with a five-year gain in brand value of 53%.

2. Can we find max value?

When M&A deals fail to generate revenue synergies, there is usually a lack of early focus on customer, marketing and branding issues. Playbooks often don’t include these steps and when they do, the discussions are qualitative and overly reliant on opinion and emotion.

The solution is in this key question: Are we deploying our assets to maximize customer use cases?

Companies can find significant incremental deal value when they integrate customer and marketing analytics in pre-close analysis and the integration management office. We studied one deal that doubled the final price of a $5 billion global asset by modeling the financial impact of future (post close) brand use cases. Another estimated market-share gains between 2 and 3% on a $60 billion deal through brand portfolio economic analysis. And on the cost side, we are helping companies lower post-merger migration costs between 15 and 40% by using cost-optimization analysis.

3. Are we serving up the right offer?

The best way to achieve this optimization is to constantly elevate the right offer for each person, on the right device and at the perfect time. Companies like Google, Amazon, Facebook and SAP are experts at this kind of hyper-responsiveness, with nearly-infinite capabilities for personalization, depending on the needs of each customer. They continually ask: Do we have an adaptive brand architecture? To win with today’s digitally demanding customers, companies need to maximize all the flexibility available through digital tools, making sure offers are as adaptive and individualized as possible.

Amazon remains a perfect example. Rather than being a monolithic Amazon or a fragmented collection of sub-brands, the brand adapts to its audience, use case or environment. Do you listen to a book at 9 p.m. each night? If so, it’s likely Amazon will push an Audible brand message just before. Recently ordered paper towels? Alexa will check-in to see if you need a refill. Context is king in our world, and successful companies will deliver an adaptive architecture that ensures maximum relevance.

Older companies don’t have to cede their future to those that came of age as digital natives. Moving forward, all companies–and all brands–can benefit from a modern portfolio and architecture strategy. And while all companies acknowledge that the future is digital, we’re convinced that those that win are those that also understand that the digital’s primary power is in better serving customers.

For more information on capturing greater value in the M&A, please contact us today.

Healthcare Transformers Series: Featuring David Edelman, CMO at Aetna

Aetna’s CMO explains why he wants patients to be more engaged, and how consumer-centricity can help.

3 min

Meet the Healthcare Transformers Leading Change in Their Organizations.

Prophet spoke with leading healthcare transformer and contributor to the book “Making the Healthcare Shift: The Transformation to Consumer-Centricity“, David Edelman, chief marketing officer at Aetna to understand how he is leading change at his organization to drive deeper engagement with consumers while delivering better business outcomes.

Get the Book: “Making the Healthcare Shift: The Transformation to Consumer Centricity”

As the industry sits on the edge of disruption, healthcare organizations need to transform to stay relevant. A new book by Prophet’s Scott Davis and Jeff Gourdji, “Making the Healthcare Shift: The Transformation to Consumer Centricity” shares real examples of how healthcare leaders are driving this transformation in their organizations.

Healthcare organizations now have both the motive and means to empower, engage, equip and enable consumers. While healthcare organizations have recognized the need to change, they have struggled to get started and sustain the effort. Based on conversations with leading healthcare organizations such as Mayo Clinic, Intermountain Healthcare, Geisinger, Anthem, Aetna, Pfizer, Novartis and more, the book identifies five required shifts organizations can make to better compete in this evolving landscape.

Through case studies and practical examples, Making the Healthcare Shift provides healthcare leaders across the healthcare ecosystem with a playbook to make their organizations more consumer-centric.

Interested in Hearing From Other Leading Healthcare Transfomers?

Watch Andrew Dreyfus, President and CEO of Blue Cross BlueShield of Massachusetts discuss how the healthcare industry is becoming more consumer-centric and how organizations need to be thinking about transformation.

From driving demand to enabling sales, new tech solutions make buying easier for business customers.

We’re now several decades into the digital age and yet transformation is still profoundly changing how we work. Until recently, the most disruptive elements have been those that empower consumers, giving rise to entirely new brands and industries like Airbnb, Uber and Spotify. B2B sales organizations–and most B2B sellers–have been several steps removed from the biggest changes. Certainly, B2B companies have deployed digital technologies to enhance business performance. But, in B2B industries such as medical devices, insurance, agriculture and business software, disruption has been less evident.

That’s changing fast, as smart B2B companies race to rethink their selling strategies. Access to data, information and channel alternatives has arrived in B2B and it’s changing the selling landscape. Intermediaries– hospitals, farm cooperatives and brokers, for example–no longer have a monopoly on data. The ability to collect customer data, store it centrally via the cloud and migrate it with orchestration across platforms is quickly breaking down legacy system silos. Data aggregators are emerging, providing a more complete view of the customer. For the first time, end-to-end customer data is a reality in B2B.

The impact of these relatively new changes is transformational. The most evolved B2B companies are reinventing the way they sell and finding ways to increase growth dramatically. But many B2B companies are still struggling to find the best path to modernize selling to accelerate growth.

The Five Digital Shifts Impacting B2B Selling

At Prophet, we see the impact of digital in B2B selling in five selling shifts:

Digital sales enablement

Digital outsourcing

Digital relationship development

Data-driven solutions

Digital demand generation

We’re working with clients to tap into each of these shifts more effectively, leveraging these future-proofing strategies to achieve uncommon growth:

Digital Sales Enablement:

This is the shift where many B2B companies have already made substantial progress by using digital tools and data to enable sellers to become more effective. Sales enablement tools, including Salesforce, Oracle and SAP are so well embedded that they are expected to be a $5 billion market within three years[1]. These platforms, networks and apps help individual salespeople achieve more and help sales teams work more effectively.

In the past few years, these platforms have shifted from customer relationship management to helping customer teams more fully engage the entire customer decision-making team. The advantages are immediate: Better equipped and coordinated salespeople accomplish more. They increase revenues, strengthen customer relationships and stay with companies longer.

Digital Outsourcing:

Companies are shifting more of selling’s routine chores to digital functions because studies of sales time utilization indicate two-thirds of a typical sales person’s day is spent on non-selling tasks[2]. Outsourcing frees-up sellers to focus on what they do best: building and expanding human relationships.

Many early efforts included more precise targeting, better sales resource planning and automating routine order-taking functions. More advanced B2B companies are also successfully making it easy to order spare parts or accessories online and handling problem resolution with advanced AI bots and call centers. These new tools make freeing up the sales persons’ time to develop relationships while increasing team efficiency and effectiveness through improved resource deployment.

Deepening Relationships:

The combination of new, more targeted vehicles such as LinkedIn advertising to reach B2B decision-makers with compelling content like video and virtual reality has opened up a shift called account-based marketing (ABM).

ABM is more personalized and tailored to the needs and criteria of individual decision-makers than traditional push email and digital advertising campaigns. It is also an integrated effort that coordinates the use of salesperson interaction and digital engagement for maximum impact and efficiency. The digital components also extend engagement into an anytime, anywhere experience through the 24/7 advantages of online and mobile vehicles.

“While the full impact of digital transformation on the sales process is still evolving, it’s clear that the classical model–where marketing and communications generated interest while the sales team closed the deal and expanded relationships–is dead.”

Data-Driven Solutions:

Oceans of data flooding the B2B value chain are shifting what sellers sell as well as how they sell. As suppliers gain greater access to data about their customers–and their customers’ customers–they have expanded the playing field for moving from selling products and services to providing data-driven solutions.

Infused with analytics and insights, solution-sellers can more readily mix the elements of the customer value proposition including pricing, value realization, value-added services, experiences and core offer innovation to suit the customers’ particular needs. In a data-driven world, they are better able to extend solutions into partnerships with other providers and make them interoperable with the customers’ systems and the ecosystem of the industry. These strategic decisions are also blurring the lines between sales, R&D, marketing and operations and demanding better leadership and teaming behaviors from sales team members and other functions.

Demand generation:

This may be one of the most exciting and rapidly evolving areas of B2B selling, particularly in intermediated businesses. The explosion of data and a rapidly expanding set of vehicles to reach B2B decision-makers among the customers’ customer is making it possible to create direct relationships with them. These channel and content alternatives are enabling established sellers to generate demand in three principal ways:

Bypassing the intermediary to sell directly

Generating sales pull through the intermediary

Hybrids of 1 and 2 where smaller size customers or certain offerings go direct, and larger size customers or parts of the portfolio are sold via intermediaries.

The Organization Imperative

All five of these B2B selling shifts spark the need to rethink the organization, redefine the roles of sales, marketing, e-commerce, data analysis and customer research and build new, often agile ways, for these teams to work together. It also requires rethinking the digital stack of how platforms and data work together in a way that can support the shifts and adapt to future changes.

Generally, we see a blurring of the roles of sales and marketing as digital investments that were previously the domain of communication-oriented marketers are redeployed to accelerate selling momentum. While the full impact of digital transformation on the sales process is still evolving, it’s clear that the classical model–where marketing and communications generated interest while the sales team closed the deal and expanded relationships–is dead.

And while we realize that B2B selling in many companies may never be fully automated, it’s essential to acknowledge how much digital can do to make it more efficient, not just more effective. Research consistently shows that the top 20 percent of a sales team is truly productive, while the bottom half often has a neutral or even negative impact on revenue growth. Hiring and training humans gets more expensive all the time, while the cost of using digital tools to find, target, serve and support customers in routine areas is plummeting.

—

[1] Jim Lundy, Lead Analyst, Aragon Research, 2017 “Aragon expects the worldwide sales engagement platform market to grow from U.S. $1.57 billion in 2017 to $5.59 billion by 2023.”

[2] Salesforce.com, Top Productivity Trends, Salesforce Blog, 2019

We don’t expect many B2B companies to be able to modernize selling without bumps and hiccups. The key to tackling these bumps is to think through the shifts and build momentum while in parallel developing and enhancing the organization’s capabilities to handle these shifts.

Our marketing and sales consulting practice helps B2B companies around the world overcome disruption and identify paths to achieving uncommon growth. Contact us to learn how we can help you.

Now in its fifth year, Altimeter‘s annual “State of Digital Transformation” research continues to document the constantly evolving enterprise. As disruptive technologies and their impact on organizations and markets continue to progress, our research aims to capture the shifts and trends that are shaping modern digital transformation.

Our global study revealed insightful differences between businesses operating in China, and those in the rest of the world, on how they think of and approach digital transformations.

In China’s distinct and fast evolving landscape, digital transformation is even more important.

In the past few years, the tech giants BAT (Baidu, Alibaba, Tencent), JD and some of our most recent tech unicorns including Didi Chuxing, ByteDance (TikTok and Toutiao), RED and Meituan Dianping among others, have led the first wave of digital transformation. Now, we are entering the ‘second half’ of the digital revolution, where more traditional businesses are transforming themselves to become more digitally-led to compete and thrive.

Over the past decade, China’s growth and technology transformation has been led and fueled by BAT (Baidu, Alibaba, Tencent). We are now entering the next chapter of digital transformation where businesses and brands must adapt and lead their own digital transformation to compete and thrive.

In China’s unique digital ecosystem, almost all companies are undergoing digital transformations. Compared to other countries in the world, Chinese enterprises embrace digital transformation in a more proactive way—with CEOs playing a bigger role in leading the effort. Additionally, companies in China prioritize consumer-facing touchpoints, such as customer experience and e-commerce, to a significantly higher degree in their digital transformation.

It is worth noting that having a strong organizational culture is instrumental to sustainable growth. However, companies in China are overwhelmingly more concerned with ROI than internal initiatives like organizational structure and employee engagement. While driving a customer-centric growth is a competitive advantage for companies operating in China, internal organization, way of working and company culture are also essential enablers for tapping into the Body, the Mind, and the Soul of the organization.

As these once-disruptive brands hit speed bumps, sharper omnichannel thinking can recapture growth.

As successful early-stage founders and investors would agree, building with a product-market fit focus is one of the top priorities in launching a company (perhaps second only to raising capital to enable the prior). Once a company has reached organic growth and reach with a product-market mindset, the priorities need to quickly shift towards strategic growth and scale.

As the digital marketplace continues to become further saturated and competition has become too numerous to name, we are helping digital-native brands focus on a few strategic objectives to help them reach uncommon growth.

6 Strategic Objectives to Help Digital Native Brands Reach Uncommon Growth

1. Build an irreplaceable, valuable brand

The digital marketplace is now an unbelievably crowded space packed with digital natives as well as droves of large consumer product brands investing in direct-to-consumer initiatives. (According to a recent Salesforce study, “despite all the criticism CPG companies receive in regard to their retail and commerce strategies, at least 99% say they’re investing in direct-to-consumer strategies.”) With such a competitive marketplace all vying for much of the same customers, the value of a meaningful brand is higher than ever.

For many digital natives, growth curves flatten quickly before they can truly build an enduringly valuable brand position. But for those that have a relevant story to tell with their brands (Dollar Shave Club, Everlane, Airbnb), strategic growth comes in the form of growth-stage capital, acquisition exits and IPOs. For traditional CPG companies and the financial market, effectiveness and success in brand building and amplification have become a clear differentiating growth indicator for targeting digital-native brands for inorganic growth.

2. Create a strategic customer targeting strategy to posture for growth

Customer acquisition is VERY difficult at the growth stage for most organizations. It takes additional capital and sophisticated growth techniques for digital-native start-ups to achieve scale without burning through profits. The question we most often hear from our growth-stage, digital-native clients is, “Now that we have figured out our initial entry market, how do we grow with new, unidentified targets and geographies?”

The first step is in taking a comprehensive look at the market landscape and executing market and customer segmentation mapped to the company’s value proposition. The strategy will be followed with a cohesive roadmap with savvy demand gen and acquisition techniques. However, this poses a chicken/egg dilemma. Many will say that they need strategic capital in order to reach these new customers. But it is very difficult to raise that capital unless you have a strategic plan in place. We’ve found that completing an expeditious, yet effective, customer targeting strategy provides investors a plan they can buy off on, which forms the basis for an immediate plan of action once the capital comes through.

3. Take customer data to the next level

Digital native brands are rich in data. However, we often find the abundance of data untapped and under-utilized in driving strategies and operational execution. Sophistication comes from not solely basing strategies on historical data, but driving current data into actionable insights that drive the execution of the product and user experience (most often through machine learning).

“Despite all the criticism CPG companies receive in regard to their retail and commerce strategies, at least 99% say they’re investing in direct-to-consumer strategies.”

Customer expectations are driving companies to think about next-gen data strategies. It’s not just about the tools and technology used to access and manage data; It’s the deeply human insights to understand and implement behavioral data-driven retention and acquisition strategies. Journeying through the landmines of data value exchange, ethics in AI and overall customer data privacy become even higher stakes with global expansion.

4. URL to IRL. Getting physical with the brand experience

With the rising cost of digital customer acquisition, many successful growth-stage digital-native brands are finding growth in brand awareness and customer acquisition with offerings in a physical retail experience (Warby Parker, Casper). However, going physical without considering the customer journey with a brand will often come up short.

It is critical to have a customer-centric approach in understanding and meeting the customer’s journey with the brand toggling in the metaverse of both digital and physical.

5. Expanding with a brand portfolio

Perhaps the market assessment tells you that an unserved market will require a different brand identity or positioning. Too many razor options for facial-hair growing men? Grooming products and supplies? Razors for women? Will the master brand be sufficient or stretched too thin? Should there be a sub-brand to capture additional opportunities among adjacent consumer segments?

Prophet vice-chairman and master brand guru, David Aaker, writes about innovating with new brand subcategories in his book coming in 2020 titled, “Achieving Uncommon Growth in the Digital Age: Own Game-Changing Market Niches.” In it, he’ll discuss how game-changing market niches create growth, how digital drives and enables new market niches to win, and how to find, evaluate, manage and build barriers around these game-changing market niches.

6. Growing together with your employees and brand advocates

In reaching out to new targets and markets, it’s easy to lose sight of the early-stage magic that created traction with customers and employees in the first place. Accelerating the speed and scale of growth without alienating the core consumer group takes extra care and caution in brand management disciplines.

The often unforeseen challenge in strategic growth is in paving the way for organizational growth – keeping the best talent, training existing talent for skills required for the next generation of growth, and luring new talent to fill resource gaps and needs. With a competitive market, it’s more than free food perks at this stage. Start-up culture is part of the secret sauce – so how do you grow without losing sight of the most important ingredient of success – employee culture?

Due to the nature of the start-up hustle, most digital-native companies have not prioritized professional development support and are not the best positioned at cultivating talent. Where speed to market is a constant drumbeat, work-life balance and communication are often weak. And as the fight for talent increases, companies need to rethink team growth. Another clear differentiating growth indicator is how companies are leveraging employee/team optimization to help with growth.

In the post-digital-revolution age where businesses are pervasively disrupted – entry barriers to earning the “first pots of gold” are ever low, while driving toward the second, third pots of gold, and achieving enduring growth is extremely challenging. Moving from organic growth focused purely on a mind-blowingly-great product or service to making strategic choices based on an understanding of their unique brand, customer and employee culture is a necessary path to achieve 2.0 and 3.0.

If your digital native brand is ready to determine its path to uncommon growth, let’s set up a time to discuss. Our team of strategic consultants is ready to help you chart the course.