BLOG

Standing out in a Sea of Sameness: Five Ways Asset Managers Can Build a Winning Brand Strategy

Prolonged and emerging pressures are creating new challenges across the industry.

How do you gain market share and attract the best talent in a market that looks like a sea of sameness? Where clients, partners, and talent see you and your competitors as interchangeable? Asset managers have long operated with this mindset when it comes to brand positioning. Compounding this challenge in recent years is the need to navigate challenges that include fee compression, market volatility, shifting regulatory environments and talent friction.

Consequently, asset managers have rapidly expanded their areas of focus: taking on a new tension around focused expertise vs. expanding the set of offers to serve investors (e.g., new industries, specialties, alternative investments, ESG investing, real estate, digital assets, etc.). Many have used expanded offers to deepen their relationships with clients and successfully compete but at the price of sometimes murky associations around specialization. Such go-to-market strategies have made it confusing for new investors to confidently invest and, at times, for asset managers to confidently sell a broader set of investments and capabilities.

Facing New Opposition

Rising interest rates, inflation, inverted yield curves, disruptive technologies (AI, digital assets), and rising global tension have shrunken available Assets Under Management (AUM), which has only increased investor trepidation as they conserve cash at a time when access to capital is more costly.

Automation and AI are also shifting the paradigm for acquiring AUM, and there could be a semi-industry rotation. The sales and client engagement processes are also evolving as a consequence of technology. It’s less about being “close” to investors for AUM and more about being “ubiquitous” and/or “famous” for something.

The theme of 2021 was a world of too much money chasing too few assets. The theme of 2023 is too little AUM for too many asset managers and their expansive sets of offers.

Consolidation is the next imminent frontier we are seeing. Franklin Templeton’s $1bn+ purchase of rival Putnam Investments and Lansdowne Partners’ plan to acquire UK equity investment manager Crux Asset Management are only the beginning.

The Asset Management Brand-Demand Challenge

While consolidation will make newly combined entities more competitive and allow them to capture efficiencies, it will not solve the two underlying challenges present in the asset management space:

- A need to establish or regain slipping relevance: Every asset management brand covered in Prophet’s Brand Relevance Index (BRI) saw a decline in relevance from 2021 to 2022, and all but one declined in relevance versus other brands from 2022 to 2023. Relevance, which directly relates to the bottom line, is noteworthy to all stakeholders. It creates importance to investors but also attracts and retains premier talent in a tighter AUM environment and bigger asset management ecosystem—building both brand and demand for the business.

- A need to create coherence: As entities combine and grow, it is critical to ensure that not just the company but also its offers and capabilities are well-articulated, organized and understood—making it easier for investors to buy and asset managers to sell.

5 Actions for Building a Winning Asset Management Strategy

1. Acknowledge and understand your unique audience motivations.

Asset managers need to manage a range of stakeholders and monitor the emerging patterns in behaviors. For example:

- Investors: Institutional and individuals are typically seeking risk-adjusted returns that outpace the other options available in the capital structure.

- Portfolio Companies: Seeking sustainable growth through capital and expertise, but also looking for purpose and values alignment.

- Capital Allocators: Seeking value creation, preservation of capital, and risk management for both the firm and its clients. They also need the best talent to convey expertise, broaden access to capital, and drive outsized performance.

- Talent: Looking to build unique career knowledge, gain experience, and get rewarded by working with the smartest people at asset management firms with the strongest cultures.

2. Establish a clear brand purpose.

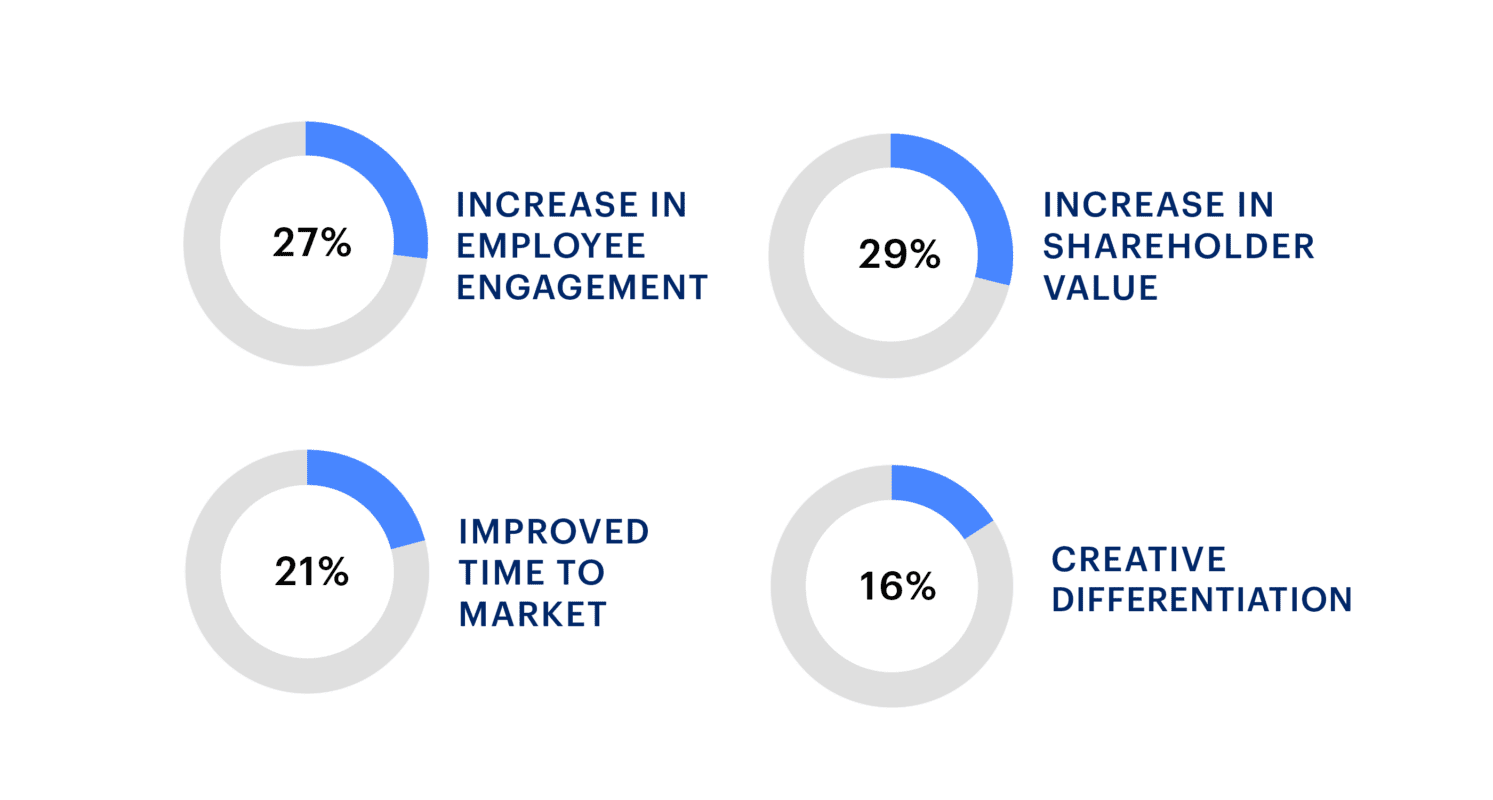

Asset management brands tend to place too great of an emphasis on what they do (alternatives, quant, fixed income) vs. answering bigger questions on how they do it (resources, ecosystem, talent) or, even further, why they align their purpose, promise, and principles to a particular vision. Brands that can’t get past what are likely to simply float along in a sea of sameness. Many asset management positionings have migrated to being ‘safe’ through a few primary lenses: looking towards tomorrow, spotlighting integrity and/or trust, and a focus on driving long-term value.

We believe many of the declines in brand relevance for asset managers can be attributed, in part, to a decline in various key client sentiment heart factors as outlined by Prophet’s BRI. Heart factors encapsulate the emotional connections that the audiences will forge with brands, e.g., ‘connects with me emotionally’, ‘makes me feel inspired’ and ‘engages with me in new and creative ways’. The erosion of these heart factors vs. more rational head factors which have remained stable, e.g., ‘know I can depend on’, ‘delivers on a consistent experience’, and ‘makes my life easier’ reinforces the idea that asset managers have reached a perceived parity across products, services, and the overall brand. Such underscores the likely importance of conveying a clear ‘how’ paired with a well-defined ‘why’ in the brand purpose with clients.

A clear how may include things like:

- Your investment philosophy and approach

- Your organization’s talent, values, and principles

- Signature stories of lasting impact on employees, investors, companies, communities, and ecosystems

A well-thought-out purpose is:

- Authentic – ties back to what you do

- Inspiring – connects with employees and customers emotionally

- Shared – creates connection and builds community

- Actionable – lived every day

In Vice Chairman at Prophet David Aaker’s recent book The Future of Purpose-Driven Branding, he outlines the use of inspiring, and mission-driven signature social programs that deploy resources to address the most pressing societal challenges. One shining example of this is State Street Global Advisors who commissioned the bronze sculpture Fearless Girl overlooking the New York Stock Exchange in anticipation of National Women’s Day. This serves as a symbol of a part of the organization’s purpose to position on the gender equality gap and reinforces its position on taking an aggressive stance on its expectation that all portfolio companies hold at least one woman on its board. The organization mentions it is prepared to cast proxy votes against board leaders when companies do not meet their diversity expectations.

3. Power brand from within using a visible human-centered approach.

It’s hard enough to articulate a clear purpose in the crowded asset management space but even harder to ensure that brand purpose connects meaningfully to people and clients. The brands’ purpose needs to align with prospective talent and customers. Shaping a visible culture plays a critical role in attracting and retaining the best people which in turn garners the attention of clients. Bridgewater Associates famously pioneered a workplace culture relying on truthful and transparent communication dubbed “radical truth and radical transparency” as part of Ray Dalio’s principle-based approach. A human-centered approach involves bridging your brand purpose into a visible culture supported by a strong employee value proposition that:

- Articulates what makes your company a strong place to work

- Improves winning in the broad talent marketplace

- Develops an enhanced foundation to support future and evolving talent needs

Doing these three things requires building from the organization’s purpose but also driving careful consideration around the Employee Value Proposition and employee experience. In some recent Prophet qualitative research in the asset management space, we found building a winning EVP requires deliberate care to the employee experience levers talent is looking for beyond compensation, such as:

- Autonomy – giving employees the freedom to make decisions that matter to them

- Mentorship – surrounding talent with leaders that inspire them

- Clarity – on how the organization will value their performance and the capital available to them

- Resources – being equipped with the right support to guide decisions and accomplish goals

- Innovation – seeing their work and the work of the company evolving toward the future

4. Revisit architecture, nomenclature, and value propositions.

Increasingly adding incremental investment products and services will raise organizational capabilities with impending M&A in the asset management space compounding that effect. But these new products, services, and areas of focus often get added to the existing array of capabilities that slowly stifle brand and portfolio coherence. Asset managers need to revisit the growing complexity of their investment focuses and develop an architecture and naming strategy that still complies with regulatory requirements but removes friction for both buying and selling offers designed to increase their AUM. Coupling this with strong value propositions that don’t just indicate what investments to provide but also how to pursue those investments in a way that serves to improve investor consideration and demand in addition to improving the ability for advisors to promote their services. The necessity for these services becomes evident when we consider a key finding from BRI, which reveals asset management brands fall short of advantageous relevance drivers that connect to aspects of having a strong brand architecture, use of nomenclature, and/or value propositions resonate with people in meaningful ways:

- Emotional resonance (connects with me)

- Value alignment (has a set of beliefs and values that align with my own)

- Essentiality (I can’t imagine living without).

5. Experiment to win with experience both internally and externally.

In an industry where both brand and culture follow predictable patterns and a substantial amount of investment follows critical business-as-usual actions around quality reporting, transparency, educational resources, technology, etc., it can be easy for marketing, business development/advisor activities, experience investments, and cultural investments to follow these patterns. Applying a portfolio construction theory to marketing, hiring, and culture investments to experiment with actions that set a brand’s purpose and culture apart can yield huge returns. Asset management company, Vanguard, is famous for owning the retirement space not just for investors but also employees whom they affectionately name their “crew”. The Vanguard Retirement Savings plan for this group offers 4% in matched contributions and an unheard-of 10% company contribution without limit.

Acknowledgment: The authors would like to thank Prophet Partner Adam Tremblay for his input in creating this article.

Don’t Miss a Beat

Sign up to receive our latest insights.

FINAL THOUGHTS

As the asset management industry continues to encounter pressure and consolidation, the asset managers able to revisit the actions that surround their brand(s) to regain relevance and establish coherence will have outsized chances of being considered. Our Prophet team has supported some of the most respected global brands in asset management to better position for growth. If you are looking to grow your brand, connect with our global team of experts today.

{kind=link}