BLOG

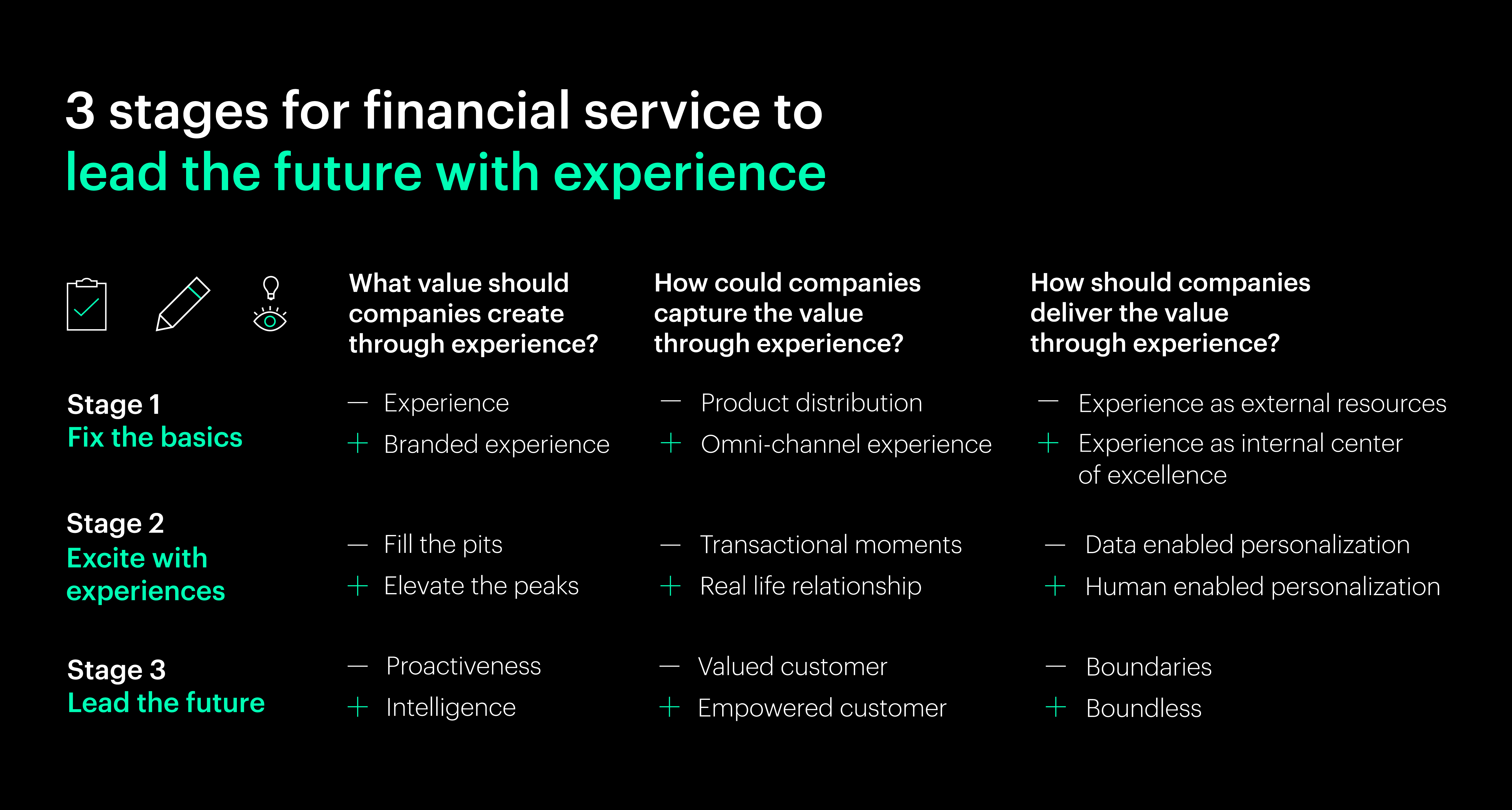

Transform Your Financial Services Retail Experiences with These 9 Levers

9 key levers across 3 development stages, each enabling financial institutions to transform their retail experience towards the future.

In many Asian markets, financial services companies used to grow alongside the macro economy and compete heavily on products. But things are changing. Product innovation within established incumbents is becoming more difficult under a slowing economy and tighter regulations. Fintech companies are disrupting legacy brands – with offers across saving, credit, insurance and more. The new generation of consumers is increasingly looking for more than short-term returns. These macro shifts indicate that in the future of financial services, reimagining the customer experience and offering benefits beyond transactions will be critical in driving sustainable, ownable growth.

Study1 shows that nearly 70% of Asian financial services companies understand the importance of “customer-centricity,” and are investing heavily to improve digitally enabled customer experiences (CX). Yet surprisingly, only 20% of customers consider FS companies providers of truly “customer-centric” experiences2. This gap is not a favorable truth but indicates a great opportunity for a company to take action and lead the future. We have identified nine key levers across three development stages that will enable financial institutions to transform their retail experiences for the future.

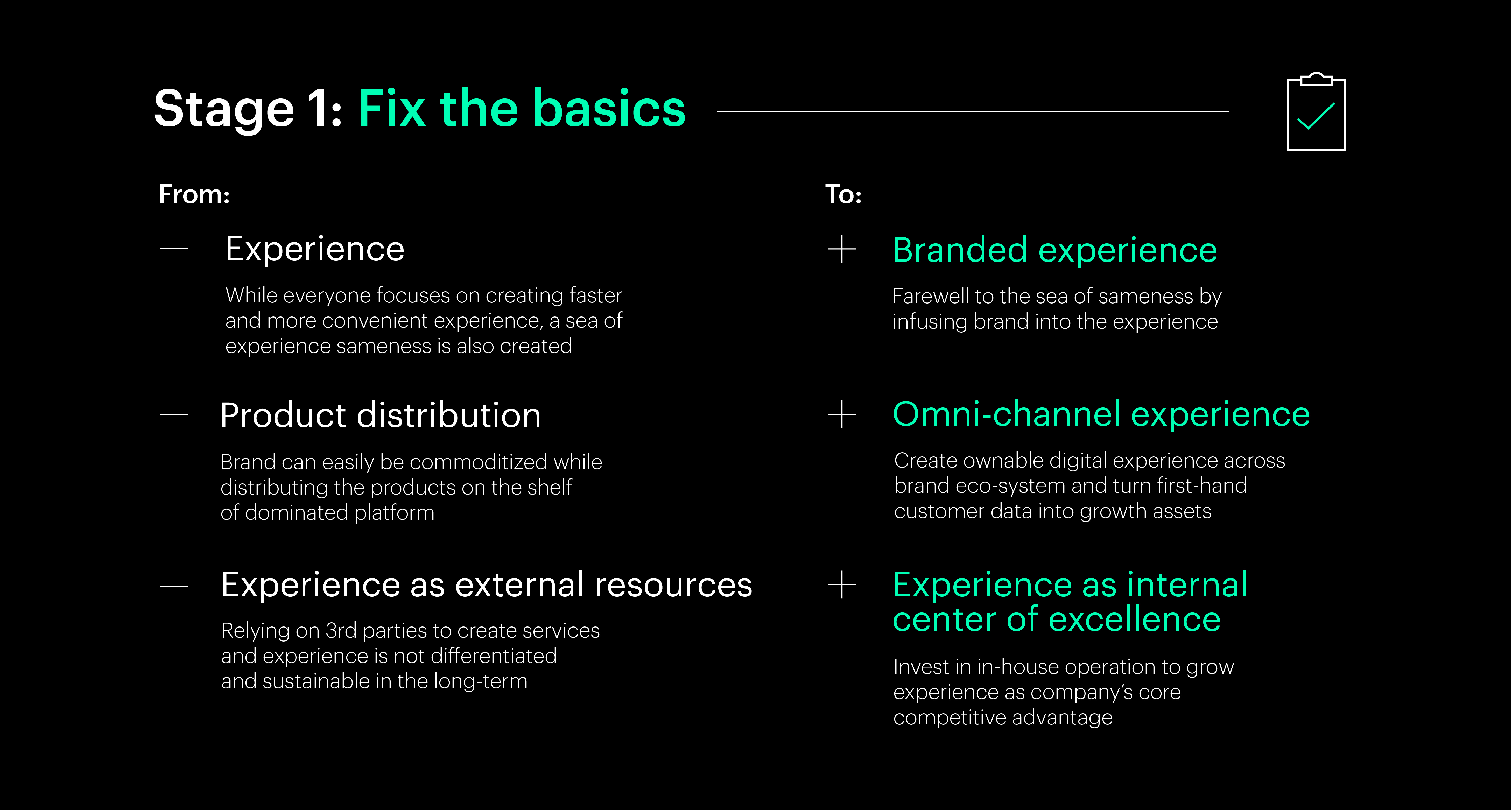

Fix the Basics: Become a Financial Services Company that Meets Customer Needs

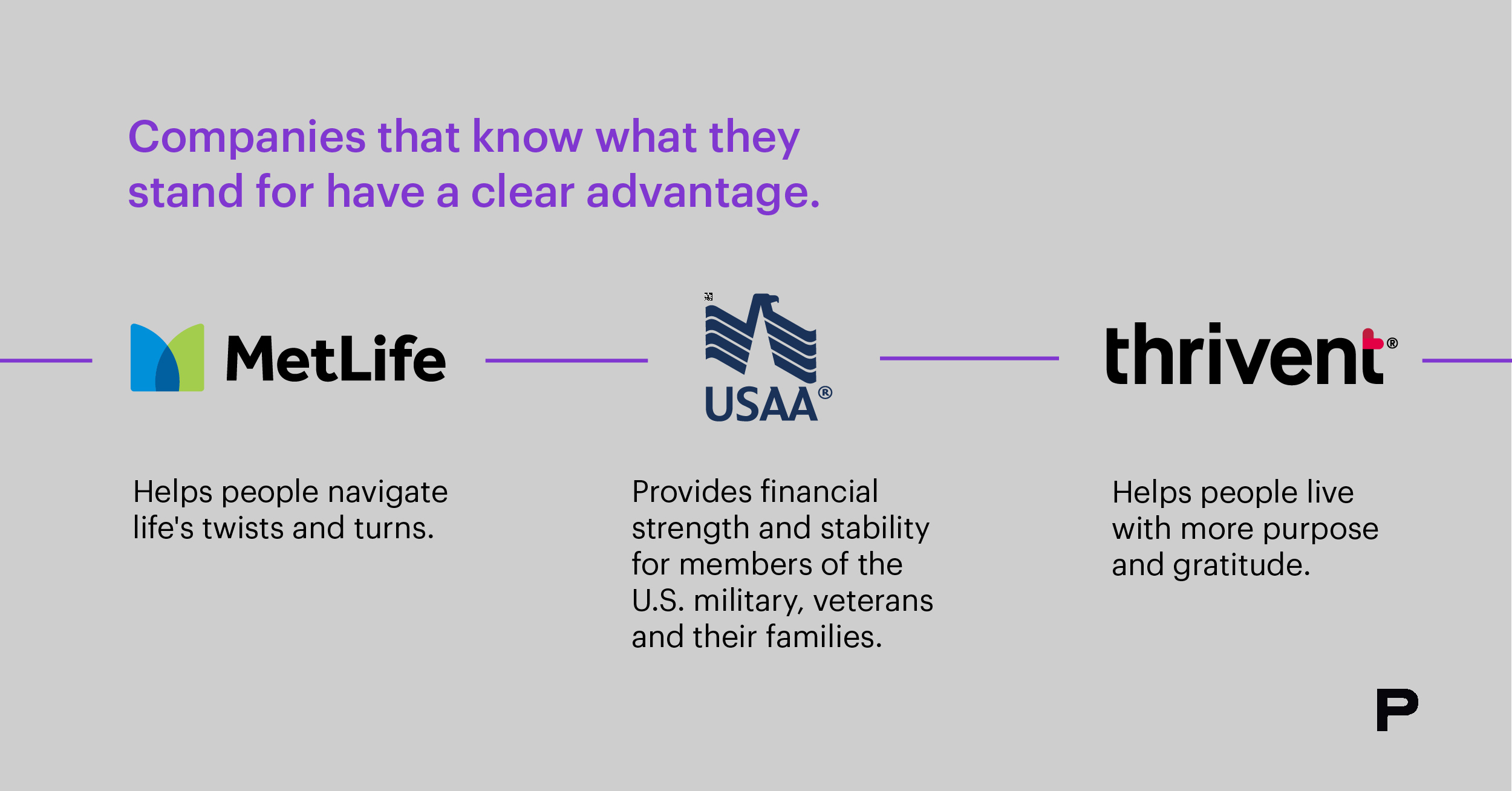

1. From “Experience” to “Branded Experience”

Speed and convenience have become critical for customers in the modern digital world. But focusing efforts solely on “ease” also tends to create very similar sets of experiences and/or functions. So how can a company cut through the clutter?

The answer is simple: brand. A solid brand strategy clearly defines what promise a company makes to its customers and how it uniquely delivers on the promise. Next, this will be translated into a brand identity system that closely aligns with the strategy and guides the development of truly ownable experiences.

For many financial services companies, brand has not been considered and managed as a strategic asset. Therefore, before aspiring to create any signature experiences, companies need to build a solid foundation first by carefully looking into their brand strategy and identity to define their own experience principles.

2. From “Product Distribution” to “Omni-Channel Experience”

Internet companies and FinTech pioneers have disrupted and transformed the retail side of financial services (e.g. Ant Finance and Ascend Money). Many companies now rely heavily on these platforms to broaden their reach to retail customers. But platforms can be restricting, and the company could face constraints in building distinct experiences and owning customer relationships.

As a solution, some leading companies have started to invest in their own digital ecosystem. For example, Fidelity created SmartRetire, a one-stop retirement solution platform. By building their own digital experience, companies can not only design and own the customer experience, but also collect data to enable targeted, more relevant engagements, that in turn can improve the customer journey in the long term.

If creating owned ecosystem is not feasible in the short term, companies should at least build a holistic plan across touchpoints and identify opportunities to maximize owned experience and relationships.

3. From “Experience as External Resources” to ‘Experience as Internal Center of Excellence”

Many financial service providers leverage third-party vendors to deliver service and experience at lower costs. However, service quality could be at risk under this outsourcing model and differentiation could be harder to sustain if the vendor relationship is not exclusive.

Companies should prioritize experiences that are most desirable to customers, viable to businesses and feasible to execute, building an internal “center” that breaks the silos, connect the dots and assures quality. A strong center of excellence enables great experience from within, bringing higher efficiency and sustainable competitive advantage in the long term.

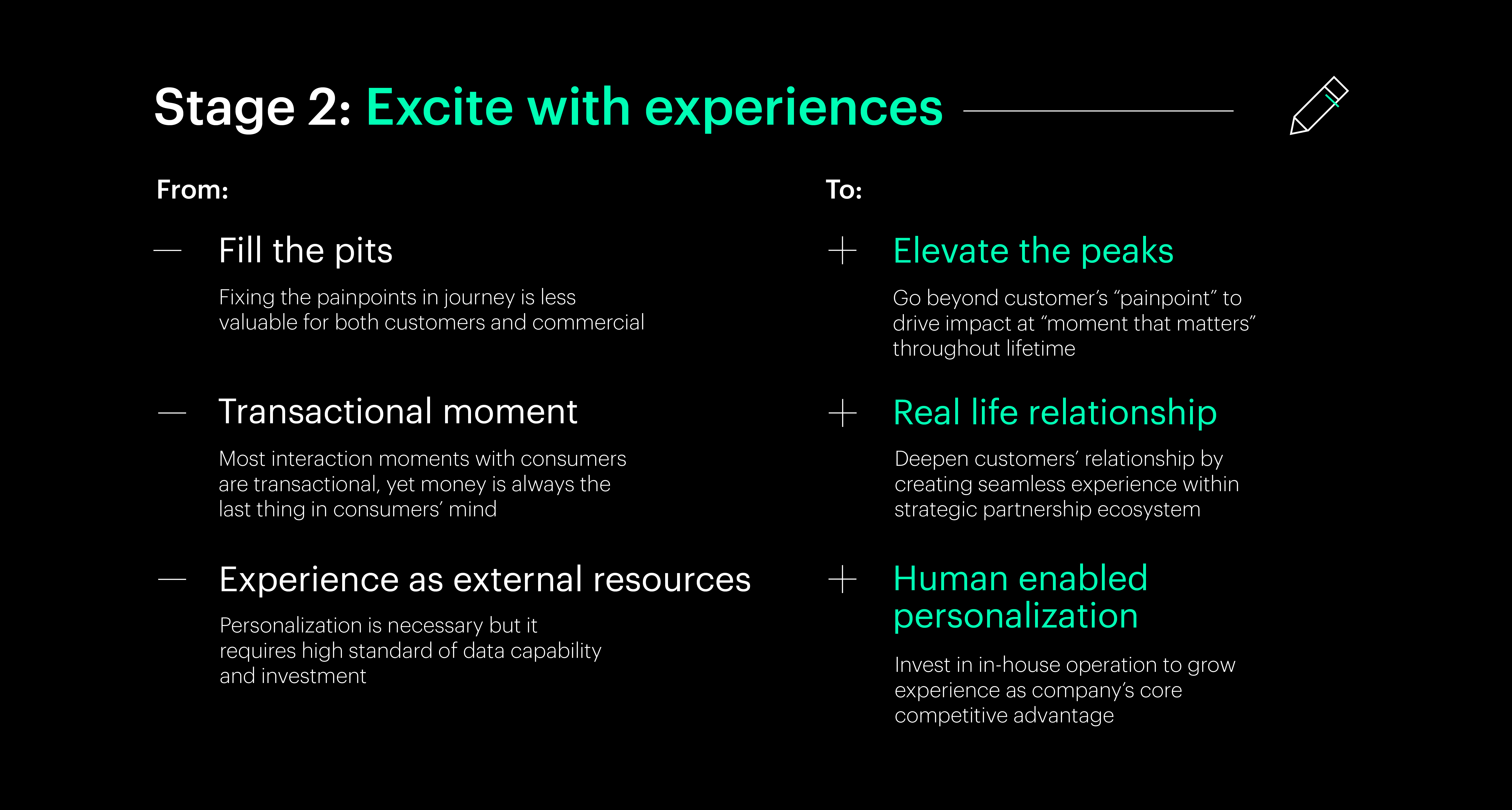

Excite with Experiences: Become a Financial Services Company that is Loved by Customers

4. From ”Fill the Pits” to ”Elevate the Peaks”

There could be a huge perception gap on “excellent customer experience.” Research3 shows that 80% of financial services companies believe they deliver excellent customer experiences, while only 8% of customers agree. One of the reasons behind this is that most companies focus only on fixing the pits upon functional pain points, but not on creating any peaks that delight and excite customers in memorable moments.

Customer lifetime could be quite long in financial services. To become a company that customers choose, trust and love, companies must build a holistic view of the customer lifetime journey, by identifying and prioritizing moments that matter and creating signature experiences that customers truly desire.

5. From ”Transactional Moment” to “Real Life Relationship”

Many financial services companies are facing infrequent interactions and transactional relationships with customers. Research4 shows that 60% of Asian customers have had zero engagement with their financial service provider in the past 18 months.

To go beyond the transactional moments, companies should look to expand their role and presence in other areas of customers’ everyday lives through partnerships and co-branded experiences. For example, Neo Bank MOX in Hong Kong partners with merchants favored by its customers and provides exclusive cash back. Another example is insurance company Beam, which partnered with a smart toothbrush brand and launched an oral health solution, offering premium incentives based on customers’ usage and behavioral data.

Companies should take a broader view of the customer journey, identify opportunities to meet people where they are in life and enable their lifestyle beyond financial needs. With expanded partnership and engagement, companies could also build an enriched understanding of customers on top of transactional data and enable future products and service innovations.

6. From “Data Enabled Personalization” to “Human Enabled Personalization”

Research5 shows that 80% of financial service customers desire more personalized experiences. In Asia, customers are 1.5 times more willing than customers in Europe to share personal data in exchange for personalized experiences. Yet it takes time to build data and analytics capabilities that enable meaningful personalization at digital touchpoints. Customers in Asia also still desire a certain level of in-person engagement – even in younger customers, research6 shows more than half believe financial services are not human enough.

So, while building data capabilities, companies should invest in empowering their front employees (e.g. RMs, agents) to deliver better, more relevant experiences with smarter tools and insights (e.g., need analysis, claim tracking). These tools should be designed not only to enable higher quality engagement but also to capture customer insights/data into the centralized database – to maintain customer understanding and relationships at risk of potential people turnover.

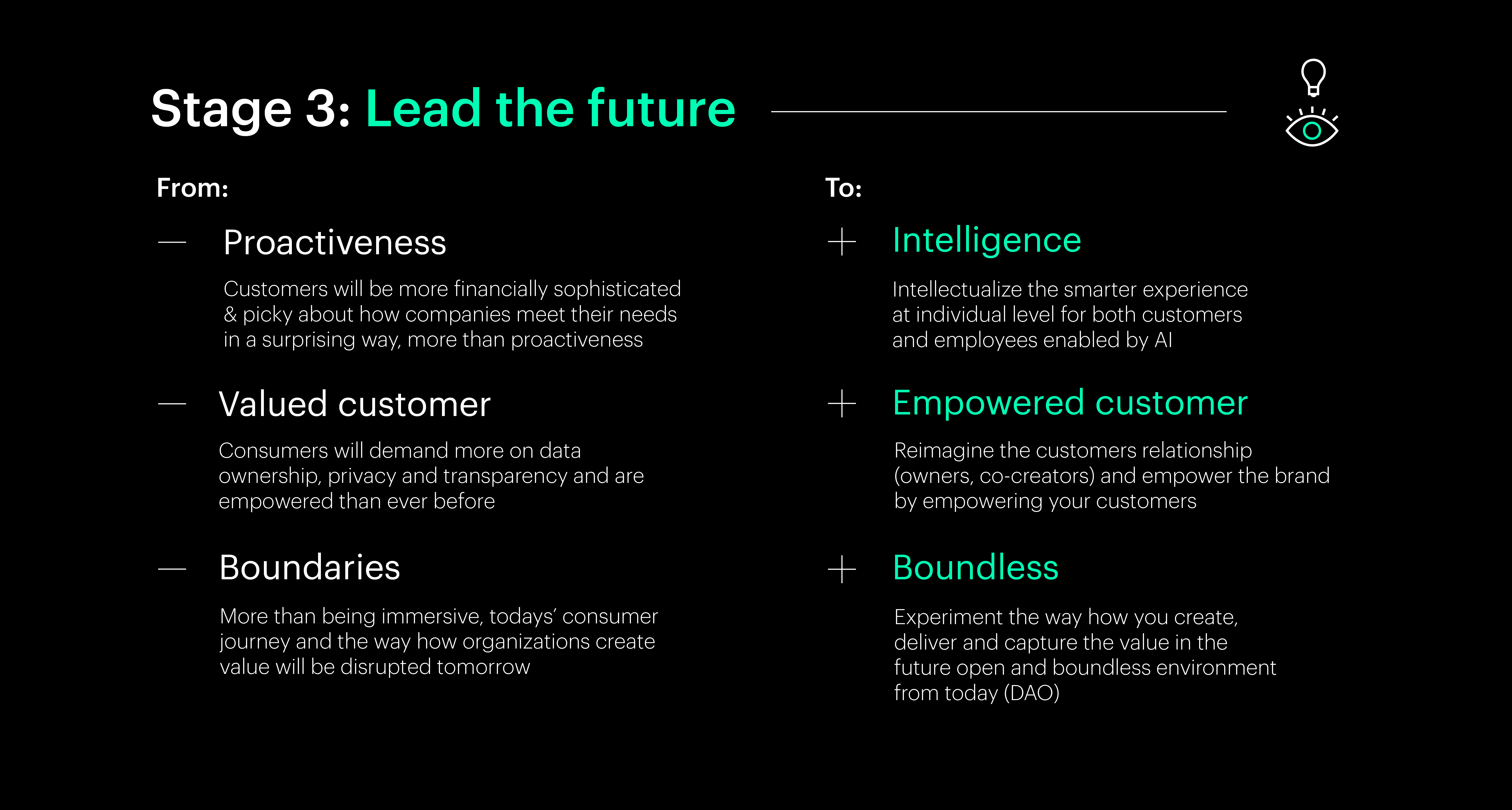

Lead the Future: Go Beyond the Frame of Reference as a Traditional Player

7. From “Proactiveness” to “Intelligence”

Customers are increasingly sophisticated and their expectations will rapidly evolve. Being “proactive” will become a table-stake part of the experience and companies could aim to lead by creating “intelligent” experiences that are three steps ahead with AI technology. In 2021, HSBC HK saw 10 times higher engagement between relationship managers and customers when it leveraged AI to offer 22 thousand different sets of wealth management solution advice to individual retail customers7.

Deep learning and hyper-personalization are among the top strategic priorities for CX leaders in 20228. Leading financial service companies should not only identify close-in use cases, such as product innovations or credit risk assessment but also stretch-out use cases that help the company go further into customers’ lives.

8. From ”Valued Customers” to “Empowered Customers”

Being “customer-centric” has been the center of gravity when creating experiences, but it still treats customers as “buyers,” in the position of receiving. As we move into the future, this relationship will be disrupted, and we will see customers as active stakeholders in deciding what type of experiences are created for them.

Creating better experiences requires data, but customers are increasingly conscious of their privacy and the power of data ownership. Research9 shows that although Asian customers are more willing to share data in exchange for better service, 90% of them are concerned about data privacy and 84% of them desire more control over how their information is used.

Leading companies should see this more as an opportunity than a challenge. Financial service brands should look at customers as empowered individuals, transform data collection into a “value exchange”, enhance data transparency with a sense of “co-ownership” and develop solutions and experiences through customer “co-creation.”

9. From ”Boundaries” to ”Boundless”

In the future world of Web 3.0, traditional boundaries will be blurred – online versus offline, virtual versus physical, consumers versus owners, etc. This boundless space will change how financial service companies organize and deliver value to customers throughout the lifecycle.

The entire model of “financial services” might change in the context of this – the role of a company could transform from a “service provider” or a “transaction middleman”, to an ecosystem or a community that enables peer-to-peer connections and better decisions among employees, partners, and customers.

The fast disruptions of fintech will never stop. Financial service companies should be open and embrace the changes to experiment with new ways of delivering value in the future, starting from small use cases.

Data source:

- Harvard business review, Taking the Financial Services Customer Experience to the Next Level

- Salesforce, Trends in the financial service industry

- Bain, How to achieve true customer-led growth and close the delivery gap

- Genesys, The era of 4.0 experience in Asia financial service industry

- Mckinsey, Future of Asia financial services

- Capgemini, The customer engagement imperative for financial services

- South China news portal, HSBC leverages smart analytics to develop new tools that enhance the personalized customer experience

- Genesys, the state of customer experience in financial services

- Warc, APAC consumers increasingly concerned about data privacy

Don’t Miss a Beat

Sign up to receive our latest insights.

FINAL THOUGHTS

With advancement in customers, technology and society, experience will become a critical driver of sustainable and transformational growth in the future. Financial services companies should take actions early and carefully assess which stage they are currently at, what levers they could invest in building towards the next stage and start with smaller test and learn today to lead the future.